TOL - 1st Dec, 2021

Alternative investing: it’s essential, not optional

Two years since the onset of the COVID-19 pandemic, investors are still looking further afield to generate asset returns, both geographically and beyond public markets. Driven by a shortage of expected alpha, income and diversification within public markets, we believe alternative assets have become essential, not optional, for meeting portfolio objectives. With investors convinced of why alternatives are necessary, they are now grappling with how to add alternatives to their portfolios. A crucial first step is to determine the investor’s investment objectives and risk appetite. Another is to decide how alternatives could complement or supplement other assets in an overall portfolio.

Two years since the onset of the COVID-19 pandemic, investors are still looking further afield to generate asset returns, both geographically and beyond public markets.

Driven by a shortage of expected alpha, income and diversification within public markets, we believe alternative assets have become essential, not optional, for meeting portfolio objectives1.

With investors convinced of why alternatives are necessary, they are now grappling with how to add alternatives to their portfolios.

A crucial first step is to determine the investor’s investment objectives and risk appetite. Another is to decide how alternatives could complement or supplement other assets in an overall portfolio2.

What to keep in mind

The diverse nature of alternatives and variation of this asset class provide a robust investor toolkit. The breadth of what can be called an alternative is one of its advantages, but it requires added levels of scrutiny to uncover the underlying attributes of each alternatives category, as well as any overlapping risks.

Alternatives generally refer to non-traditional investment opportunities in any asset class except traditional stocks, bonds and cash. Some examples include liquid alternatives (which generally are mutual funds with exposure to strategies such as long and short positions), hedge funds, private credit, private equity and real assets such as infrastructure, real estate and transport.

While some alternatives have a distinct and easily defined primary function in a portfolio (e.g., private equity as a source of appreciation-driven returns), other categories can be more opaque and play multiple roles.

We group alternatives according to three main portfolio functions - alpha, income and diversification – and we consider the extent to which each category can deliver on these goals1.

Alpha

Because alternatives can behave differently to traditional assets, they can act

as potential alpha generators in an overall portfolio2. A thoughtful mix between private and public assets can deliver different outcomes and may

help improve portfolio risk/return profile.

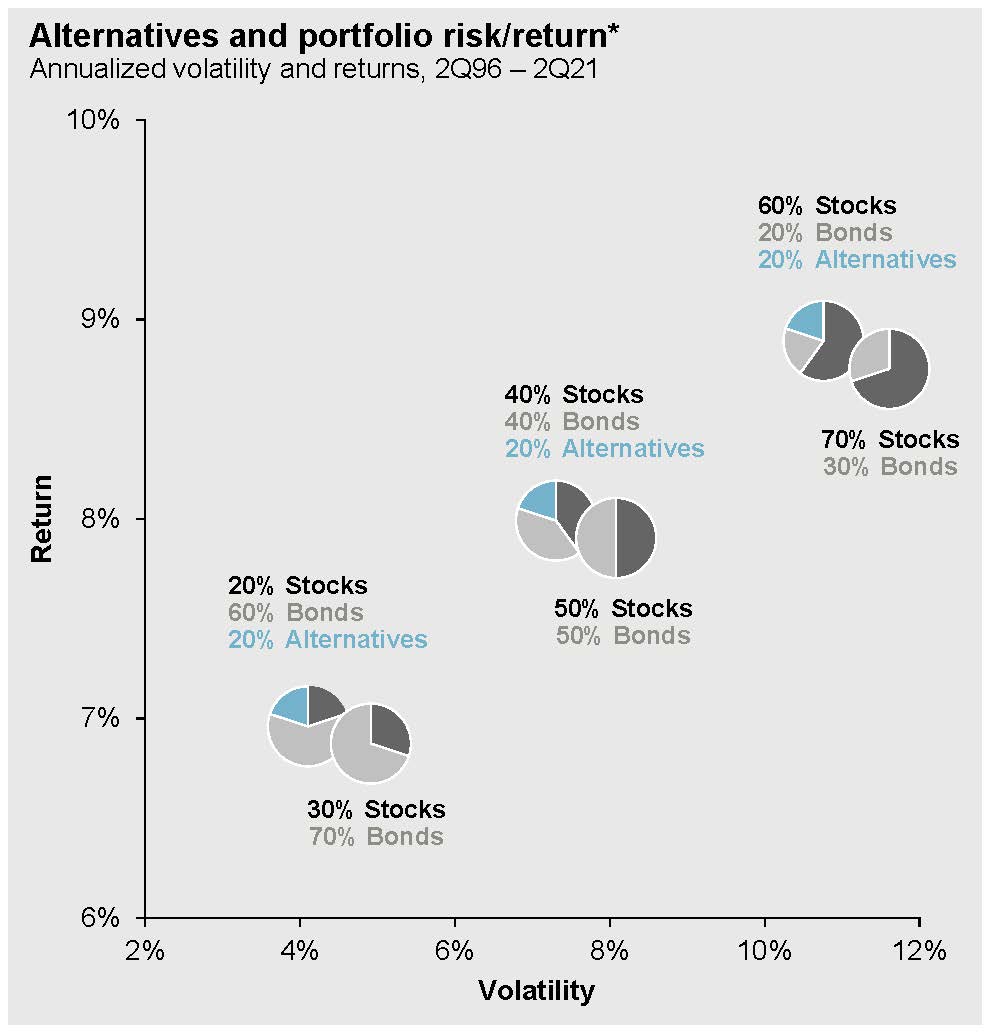

Alternatives and portfolio risk/return3

As illustrated in the chart3, adding alternative assets may provide opportunities to improve returns or lower volatility by allocating from bonds and stocks.

INCOME

Finding

income in some fixed income sectors has been challenging. Alternatives can help

generate relatively attractive yield opportunities amid low rates and even

negative real rates,

as

illustrated in the chart4.

Alternative sources of income4

While many investors seek more income in high-yield (HY) bonds, such bonds are also more correlated to equity markets with higher risk, when compared with government bonds. Sectors such as transport, direct lending, and global infrastructure can offer relatively attractive yields with similar diversification benefits to traditional fixed income.

DIVERSIFICATION

Because alternatives have a low correlation to traditional assets, they have the potential to offer diversification benefits to an overall portfolio. Even within alternatives, one asset can behave differently from another, providing additional diversification opportunities.

Through this lens, investors can sort the universe of alternatives according to their primary (and secondary) attributes and what is most applicable for their portfolios. Once identified, attention needs to be directed to determining the best way to access them.

Access to alternative investments

Opportunities to invest in private markets are becoming increasingly accessible to non-institutional investors, as asset managers are building bridges to cross from public to private markets. A proliferation of new investment vehicles are allowing smaller investors to build more diversified portfolios incorporating unique potential alpha sources.

Among the relatively more accessible, and also more commonly known types of alternative assets are liquid alternatives and hedge funds.

Liquid alternatives are generally mutual funds that aim to help investors diversify and manage risks through exposure to alternative investment strategies such as long and short positions. They are deemed liquid as they can generally be traded on a daily basis, unlike some traditional alternatives.

Hedge funds can generally provide diversification opportunities through their non-correlated or negatively correlated returns. As illustrated in the chart5 below, hedge funds have managed downside risks during periods of market stress, circled in blue.

During most of the periods of acute market stress over the last 30 years, hedge fund correlation to a 60/40 stock-bond portfolio has fallen to zero or below. Correlations came down in 2020, although not as far as during other periods of volatility, likely because market volatility during the COVID-19 pandemic was brief relative to past downturns.

Hedge funds and traditional portfolios5

Still, investors need to be aware of the risks as alternative techniques such as short-selling and derivatives aren’t commonly used in traditional stocks and bonds. In general, an allocation to alternatives should be outcome oriented – identifying the challenge that the investor is trying to address, and then allocating to the asset that will provide the desired solution.

Conclusion

Stocks and bonds will likely continue to dominate most investors' portfolios. Still, investors need solutions that can improve returns while optimising risk1. Alternatives can potentially be higher returning substitutes for stocks and bonds. As market conditions evolve, alternatives are starting to bridge the gap. In our view, they have shifted from optional to essential in an overall portfolio.

Build robust portfolios with defensive qualities using alternatives

Please join Anton Pil, Global Head of Alternatives at J.P. Morgan Asset Management and David Wright, CEO of Zenith Investment Partners for an interactive webinar on 10 December at 9am AEDT as they discuss how to use alternatives to achieve your investment goals.

Register for the webinar here

Find out more about J.P. Morgan Asset Management's Alternatives capabilities.

Footnotes

- Provided for information only, not to be construed as investment recommendation. Investments involve risks, not all investment ideas are suitable for all investors.

- For illustrative purposes only based on current market conditions, subject to change from time to time. Not all investments are suitable for all investors. Exact allocation of portfolio depends on each individual’s circumstance and market conditions. The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

- Source: Barclays, Bloomberg, FactSet, HFRI, NCREIF, J.P. Morgan Asset Management; Standard & Poor’s. *Stocks: S&P 500. Bonds: Bloomberg Barclays U.S. Aggregate. Alternatives: equally weighted composite of hedge funds (HFR FW Comp.) and private real estate. The volatility and returns are based on data from the period 30.06.1996 – 30.06.2021. Indices do not include fees or operating expenses and are not available for actual investment. Past performance is not a reliable indicator of current and future results.

- Source: Alerian, Bank of America, Bloomberg Finance L.P., Clarkson, Drewry Maritime Consultants, FactSet, Federal Reserve, FTSE, MSCI, NCREIF, Standard & Poor’s, J.P. Morgan Asset Management. Global transport: Levered yields for transport assets are calculated as the difference between charter rates (rental income), operating expenses, debt amortisation and interest expenses, as a percentage of equity value. Asset classes are based on NCREIF ODCE (Private real estate), FTSE NAREIT Global/USA REITs (Global REITs), MSCI Global Infrastructure Asset Index (Infrastructure assets), MSCI Global Property Fund Index – North America (U.S. Real Estate), MSCI Global Property Fund Index – Asia-Pacific (APAC real estate), Global Bloomberg Barclays U.S Convertibles Composite (Convertibles), Bloomberg Barclays Global High Yield Index (Global HY bonds), J.P. Morgan Government Bond Index EM Global (GBI-EM) (Local currency EMD), J.P. Morgan Emerging Market Bond Index Global (EMBIG) (USD EMD), MSCI Emerging Markets (EM equity), MSCI Europe (European. equity), MSCI USA (U.S. equity), ASX 200 (Australian equity). Transport yield is as of 30.06.2021, Infrastructure and real estate 31/03/21. Past performance is not a reliable indicator of current and future results. Data as of 30.09.2021.

- Source: HFRI, Standard & Poor’s, Bloomberg, Barclays, FactSet, J.P. Morgan Asset Management. *60/40 portfolio is 60% S& P 500 and 40% Bloomberg Barclays US Aggregate. Hedge funds are represented by HFRI Macro. Correlation is calculated on a 12-month rolling basis. Data is based on availability as of 31.08.2021.

Disclaimer

Provided for information only based on market conditions as of date of publication, not to be construed as investment recommendation or advice.

Diversification does not guarantee investment return and does not eliminate the risk of loss. Yield is not guaranteed. Positive yield does not imply positive return.

© 2021 All Rights Reserved - JPMorgan Asset Management (Australia) Limited ABN 55 143 832 080, AFSL No. 376919

Diversification does not guarantee investment return and does not eliminate the risk of loss. Yield is not guaranteed. Positive yield does not imply positive return.

© 2021 All Rights Reserved - JPMorgan Asset Management (Australia) Limited ABN 55 143 832 080, AFSL No. 376919

The information provided in the article is general in nature only

and does not constitute personal financial advice. The information has been

prepared without taking into account your personal objectives, financial

situation or needs. Before acting on any information on this website you should

consider the appropriateness of the information having regard to your

objectives, financial situation and needs. Therefore, before you decide to buy

any product or keep or cancel a similar product that you already hold, it is

important that you read and consider the relevant JPMorgan fund Product

Disclosure Statement (PDS) and Target Market Determination (available from (VIEW LINK)), and make sure that the product is appropriate for you. Before making any

decision, it is important for you to consider these matters and to seek

appropriate legal, tax, and other professional advice

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Kerry Craig, Executive Director, is a Global Market Strategist. Based in Melbourne, Kerry is responsible for communicating the latest market and economic views from our Global Market Insights Strategy Team.

........

Provided for information only based on market conditions as of date of publication, not to be construed as investment recommendation or advice.

Diversification does not guarantee investment return and does not eliminate the risk of loss. Yield is not guaranteed. Positive yield does not imply positive return.

© 2021 All Rights Reserved - JPMorgan Asset Management (Australia) Limited ABN 55 143 832 080, AFSL No. 376919

The information provided on this website is general in nature only and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information on this website you should consider the appropriateness of the information having regard to your objectives, financial situation and needs. Therefore, before you decide to buy any product or keep or cancel a similar product that you already hold, it is important that you read and consider the relevant JPMorgan fund Product Disclosure Statement (PDS) and Target Market Determination,which are available to download on this website and make sure that the product is appropriate for you. Before making any decision, it is important for you to consider these matters and to seek appropriate legal, tax, and other professional advice.

1 topic

Kerry Craig, Executive Director, is a Global Market Strategist. Based in Melbourne, Kerry is responsible for communicating the latest market and economic views from our Global Market Insights Strategy Team.

Expertise

Kerry Craig, Executive Director, is a Global Market Strategist. Based in Melbourne, Kerry is responsible for communicating the latest market and economic views from our Global Market Insights Strategy Team.

Expertise

Comments

Comments

Sign In or Join Free to comment