An Axing for Axsesstoday

Last month Axsesstoday (AXL) was on its way to becoming a market darling. Today it is suspended from trading. The CEO is gone. The stock was already down by a third and things won’t be pretty if it ever trades again. It’s a tale of growth turned disaster.

To say the equipment financier was growing quickly would be an understatement. Last year saw net profit up 94%; the year before 155%. The forecast for the current year was for net profit to grow another 82%. This was all driven by a very rapid increase in lending. Loans, mainly to hospitality and transport clients (think coffee machines and second hand trucks) finished last financial year at $336m. Four years earlier loans were just $4m.

Debts going bad

The company constantly reminded investors of their “disruptive digital financing” solution, with “scalable credit risk management” while giving “real time credit approvals”. Despite all that, the reckoning came in the latest set of financial results. Bad debts and arrears (also known as soon-to-be bad debts) rose dramatically. While revenue was up 130% on the previous year, bad debts almost tripled. And arrears, those borrowers who are behind in their payments, increased by more than six times. They are now about 4% of total loans.

This is partly because the company changed its accounting policies, leaving loans in the arrears bucket (and not expensing them) for longer. Had they not, the result would have been much worse. Bad debts would have been higher, reducing profits even further.

A growing loan book can hide plenty of problems, and the faster the growth the easier it is to hide bad loans. That’s because loans don’t falter right away. An optimistic new cafe owner will take time to run into trouble, so a poor loan made today might take a year or two to go bad.

That alone would have caused plenty of issues. But then things got worse.

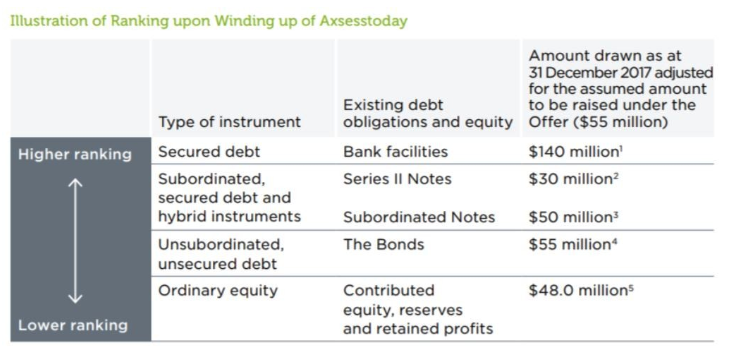

The change in those accounting assumptions “inadvertently” triggered the company’s financial covenants with senior bank lenders. This is not trivial for a highly leveraged business with $280m of debt and only $70m of equity. The company is madly scrambling to get a waiver to the covenants. If these don’t come it could be game over. Even if they do come, Axsesstoday could be stuck paying a lot more than the promised 7% on its borrowings.

And there was another breach, this one a little harder to explain. Business loans of $2m were made outside of the bank facility terms. The company will have to come clean on why that was lent and where the money ended up.

Equity holders might not be the only casualty here. Axsesstoday also raised $55m through a corporate bond in July. It is separately listed under the ticker AXLHA. Those bond holders rank just above equity holders and earn only about 7% for bearing plenty of risk. Trying to pick up an extra 2% or 3% in interest may cost bond holders plenty of capital.

A cautionary tale

It hasn’t been smooth trading for the other listed small business lenders either. Silverchef (SIV) had also been growing its hospitality and transport lending. It’s now in trouble, breaching its debt covenants in June and looking for more capital.

Thorn (TGA), a holding of the Australian Shares Fund, has been growing its equipment finance book quickly, too. Arrears haven’t risen yet, but bad loans could be lurking. At least for Thorn, trading at half of its book value, plenty of problems have been factored in to the market price.

Growth is seductive. But growing too fast can be dangerous. Lending money as quickly as possible may look good for a while, but the risk of lending to the wrong clients, and borrowing to do it, can quickly end a business.

Did you enjoy that?

If you are interested in receiving the Forager monthly and quarterly reports, please register here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Alex is a Portfolio Manager at Forager Funds Management, responsible for managing the Forager Australian Shares Fund alongside CIO Steve Johnson

.jpg)

.jpg)

Alex is a Portfolio Manager at Forager Funds Management, responsible for managing the Forager Australian Shares Fund alongside CIO Steve Johnson

Expertise

Alex is a Portfolio Manager at Forager Funds Management, responsible for managing the Forager Australian Shares Fund alongside CIO Steve Johnson

Expertise

Comments

Comments

Sign In or Join Free to comment