Another chapter in the volatility story

Vimal Gor

Pendal Group

While the situation in Europe is likely to continue capturing investors’ attention in the near-term, the real story is one that we have spoken of repeatedly this year, namely; the return of volatility.

It is a story driven chiefly by the withdrawal of an unprecedented swell of liquidity in the financial system. A tide that had lifted all asset classes, but more importantly a force that had lured investors to those offering higher yields, which are now those that are the most at risk of an unwind.

We won’t rehash all the implications here, but what is worth emphasising is that the aforementioned moves across Italian bonds and high yield credit are part of this much larger story, which arguably has many more chapters ahead.

Market headlines in the final week of May were dominated by developments in Italian politics. Uncertainty over which parties would lead the country’s government and what policies they would pursue drove some sizeable price swings that extended beyond Italian bonds.

We thought it would be timely to highlight some of the more noteworthy market movements and the relevance to broader risk-sentiment.

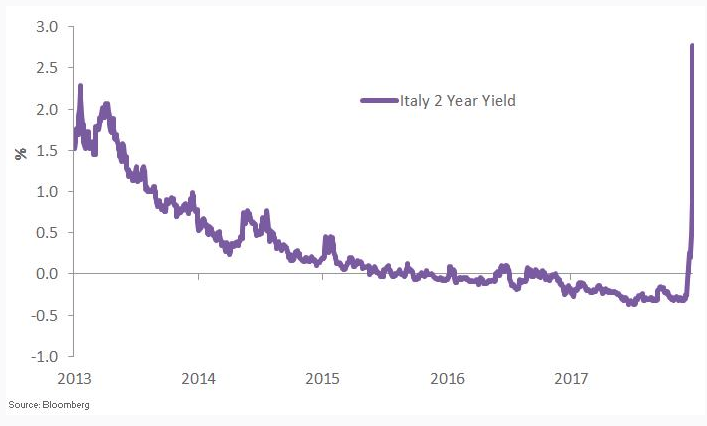

The most dramatic reaction to the Italian turmoil has arguably been witnessed in yields for Italian bonds, the fourth largest bond market in the world. As illustrated in Chart 1 below, the 2 year Italian yield spiked an alarming 304bps during the month.

Chart 1: Italian 2 year yield

This benefited our positioning for a widening in the spread between Italian and German yields. Given the arithmetic of the election results in March, there was never a possibility of a market friendly outcome. The best outcome for the establishment parties was a second election, but in reality this would have just bolstered support for the populist parties.

Moreover, while there were echoes of the French election worries that ultimately fizzled last year, as we explore later – the market environment has changed and risk sentiment is more vulnerable than 2017.

Beyond Italy, the sharp correction for risk appetite spread through the region with Spanish bonds suffering a smaller but still significant spike (2 year yields from -34bp to 7bp).

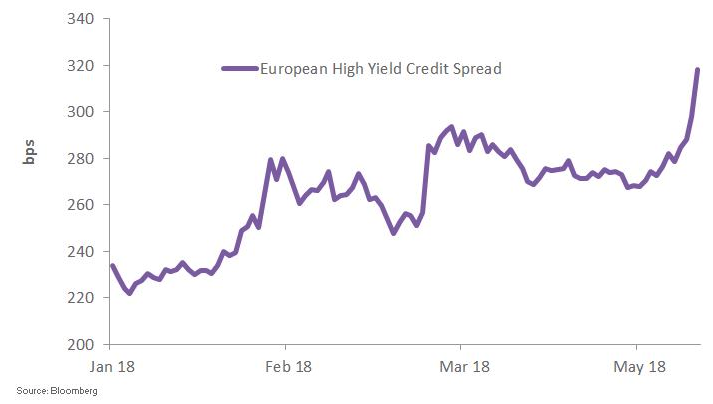

Similarly, the region’s common currency endured a 3.2% slide, the largest monthly decline since November 2016. The spill-over effects were also felt in the credit arena, where the cost of protection on European high yield jumped 51bps.

This accelerated the trend higher calendar-year-to-date as visible in Chart 2. These sizable moves served our short credit and short Euro exposure well.

Chart 2: European High Yield CDS Credit Spread

In terms of the economic landscape, we have previously pointed to reasons why we believe the European growth story has tired and has already turned a corner.

This includes the gusting tailwind of strong export growth fading to a breeze as the surge in Chinese imports drops, coupled with the looming effects of trade wars.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Comments

Comments

Sign In or Join Free to comment