ANZ is Paying the Price for a Failed Asian Strategy

ANZ’s results this morning were disappointing on a number of fronts. The headline profit drop of 24% versus the same period last year looks substantially worse than it is, with the new CEO “kitchen sinking” $717 million of one-off items including capitalised software write downs, impairments on equity stakes in Asian banks and restructuring expenses.

The largest of those item is $441 million of capitalised software write downs, with the treatment of capitalised software always a grey issue. Maintaining software is arguably an operating expense so it shouldn’t be capitalised but banks often treat it as an investment and thus are able to increase their short term accounting profits, at the expense of their long term profits. APRA zeroes out this when it assesses bank capital, as software is unlikely to have any meaningful value if a bank is broken up and sold.

The more interesting story is the increase in provisions. The $918 million expense for the half year is $408 million higher than the same period last year and $223 million higher than the previous six months. The increase all comes from the commercial and institutional lending departments, split between Asian exposures and Australian exposures. ANZ pins the increased provisions in Australia on the resources sector.

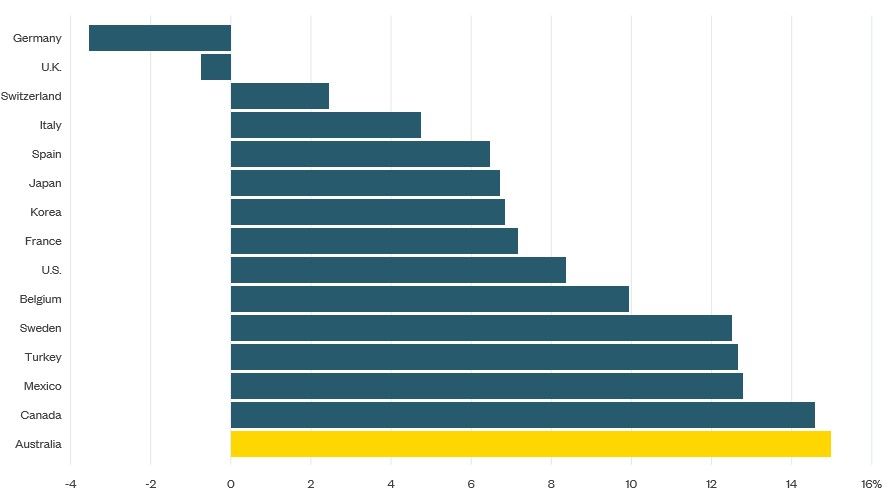

The increase in Asian lending provisions is disproportionately large relative to the size of its Asian lending book. For those who understand credit markets this would come as no surprise. Australia has long been amongst the most profitable lending markets in the world as shown in the Bloomberg table below, which compares the return on equity for large banks in each country.

Source: Bloomberg

ANZ is now paying the price to unwind its Asian lending operations, with provisions announced today linked to this. The strategy to establish a large Asian lending book for corporate and institutional clients was always misguided. Asian corporate lending is far less profitable than corporate lending in Australia, which itself is less profitable than home lending in Australia. As a new entrant, ANZ had little to win over clients unless it offered lower pricing or took on higher risk. Either of those strategies will destroy a bank’s return on equity. Lower pricing impacts immediately via lower net interest margins, which ANZ has long struggled with. Higher risk lending doesn’t show up in the short term, the impairments usually take years to appear as they are now.

ANZ should have learnt the lessons of Royal Bank of Scotland and Bank of Scotland, who took enormous losses in Australia in 2008 to 2012 as a result of pursuing aggressive growth in corporate and institutional lending. This is not hindsight analysis, the competitive landscape hasn’t changed. There has long been a surplus of banks in Asia, competing for a limited number of corporate clients.

Share markets have punished ANZ in the past for pursuing low profit growth. It is likely ANZ will feel more pain in coming years as the Asian lending book is unwound and capital is redeployed domestically. Much of it will need to go towards rebuilding ANZ’s capital levels, as Mike Smith’s strategy of jawboning the regulator for lower minimum capital levels has also failed.

For Australian investors the wider lesson is that credit providers in Australia are paid very well for taking limited risk. Banks here face limited competition and this shows through in higher margins on lending and lower risk through security position and covenants. More avenues are emerging for Australian retail and institutional investors to take advantage of this, correcting the common over-allocation to equities and underinvestment in credit.

A recent example of this was a AAA rated, residential mortgage backed security offered at bank bills +2.75%. It may not sound exciting but the ASX accumulation index has only delivered bank bills +2.69% since inception in 1980.

Written by Jonathan Rochford for Narrow Road Capital on May 3, 2016. Comments and criticisms are welcomed and can be sent to info@narrowroadcapital.com

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

3 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management