Are we headed for a rate cut in Australia?

We witnessed an almost perfect “about face” last year from most of the market on interest rates with the start of 2018 all about rising interest rates / bond yields on the back of bullish economic & stock market predictions, while the second half focussed on a looming recession and hence falling bond yields – interestingly both scenario’s led to aggressive sell offs in stocks who appear to like things just as they are i.e. we’ve been in a sweet spot for assets for almost a decade and changing dynamics = more volatility.

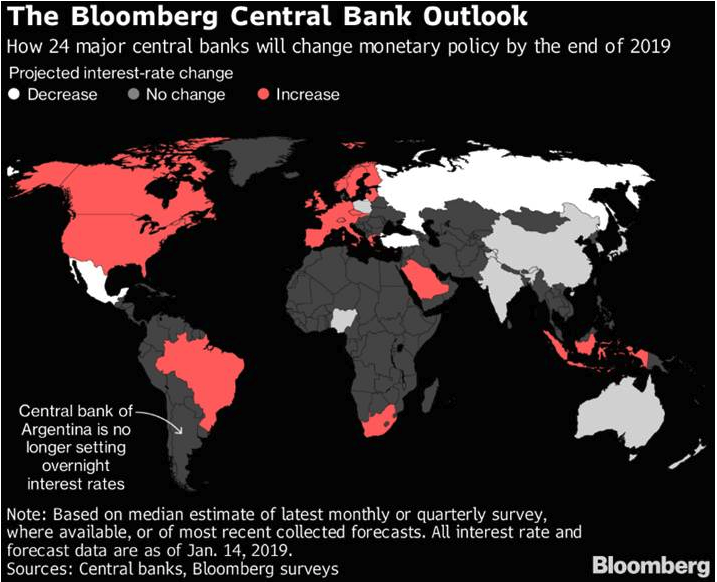

The below map shows how economists see major central banks altering interest rates in 2019 ; 3 quick takeout’s:

1 – The market is expecting Australia to cut rates with a falling housing market undoubtedly having a huge impact here.

2 – The US Fed is expected to continue its path of raising rates.

3 – Most of the Emerging Markets are expected to maintain their current levels.

Bloomberg Central Bank Outlook

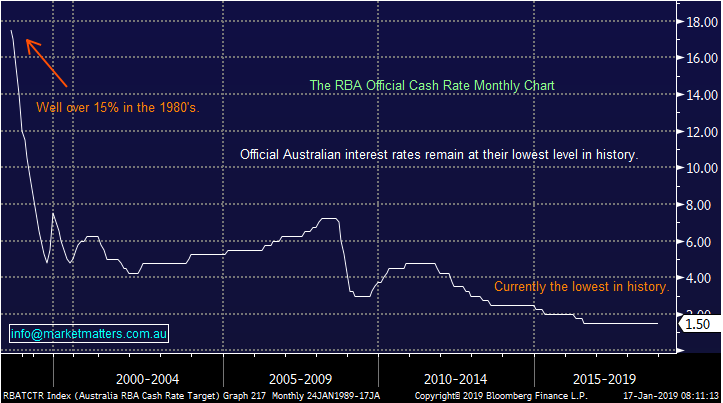

The futures market is targeting a cut in local rates next year but we question whether trimming things further from the already lowest in history 1.5% will have any impact. The housing market which is scarring many is not falling because of interest rates, it’s been an engineered policy decision by bureaucrats who are now scarred they’ve gone too hard too fast – wouldn’t be the first time!

While a downturn in the local property market is having a detrimental impact on consumer spending initially taking over 1% from growth, this is not yet pushing us into recession. For Australia to finally experience the “big R” China probably needs to keep slowing which would put pressure on commodity prices.

If China holds together, maintains stimulus and the US / China trade negotiations are settled, the RBA will not cut rates in our view

RBA Official Cash Rate Chart

However what matters the most to MM is what stocks will perform the best in 2019 due to the RBA’s actions, or perhaps their inaction. Over the last year the “yield play” stocks like Transurban (TCL) and Sydney Airports (SYD) have essentially trod water hence putting in a better performance than the underlying ASX200 which has been weak. That implies that lower rates have been factored into market / pricing of these sort of stocks.

If we’re wrong and current market pricing is right what stocks would benefit? Property is the obvious one, however the main beneficiaries we think would have commercial / office exposure rather than residential given residential has a higher degree of emotional bias connected to it plus retail landlords would still struggle. Transport and utilities generally do well while infrastructure would rally from here – stocks generating overseas earnings would also benefit from the decline in currency.

Sydney Airport (ASX: SYD) Chart

Conclusion

Overall, we remain in “sell mode” at current levels, looking to increase cash to buy future weakness.

We do not believe the RBA will cut rates in 2019 or 2020 unless the economy deteriorates markedly.

However we doubt rates will go up and will consider buying the “yield play” stocks if a suitable / risk reward opportunity presents itself.

Want to learn more?

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

2 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment