Are we "mid-cycle" or "late-cycle"?

In the AFR today I argue that we are not "late-cycle" as so many commonly claim, but rather mid-cycle, which has profound ramifications for how one should optimally allocate capital (AFR subs can click here). Brief excerpt:

I hear a lot of ostensibly smart people relentlessly recite the meme that we are “late cycle” with the implication that a recession is right around the corner. In this vein there are many overpaid equity investors spruiking the next financial crisis. That’s interesting given investment-grade credit default rates are at historically low levels and forecast by Standard & Poor’s to fall, not rise, in the short-term.

Sure, anyone can conceive of financial Armageddon if Trump suddenly decides to throw the US economic baby out with his rhetorical bathwater, or if he feels compelled to nuke North Korea. But the hard facts are that the global economy is coming out of the most destructive recession since the great depression and has untapped capacity, which is why core inflation and wages rates remain materially below historical trend levels.

This also explains why real cash rates are still negative in most developed economies. And that essential delivery device for the worst contagions, banking systems, have been radically cutting, not increasing, leverage for the best part of a decade.

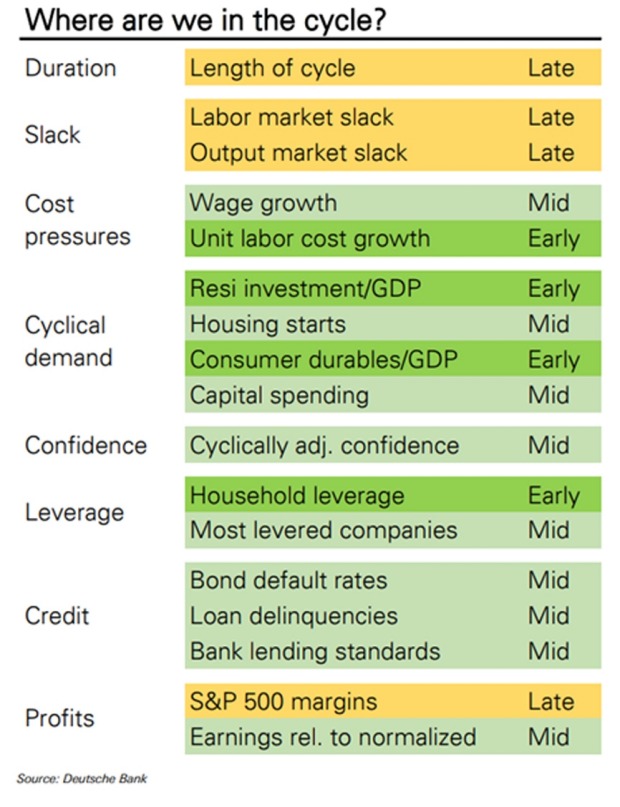

The question of where exactly we are in the economic cycle, which has profound ramifications for investment returns, is ultimately an empirical one. So I was delighted to see that Deutsche Bank’s chief international economist, Torsten Slok, has attempted to objectively address it.

He considers eight key measures of economic activity in a cyclical context: the length of the recovery; labour market and output slack; cost pressures; cyclical demand; leverage; credit default rates and lending standards; and profitability.

Across five variables (inflation, demand, confidence, leverage, and credit quality) Slok finds that we are actually in the early-to-mid stages of the US cycle. It is only on the basis of the duration of the cycle, and labour and output slack, that we appear late cycle. And there are question marks around these two late cycle indicators.

The duration is long because of the depth of the creative destruction wrought since 2008, the likes of which the global economy had not experienced for a century. It was always expected that a recovery burdened by deleveraging would be elongated. Duration is, as a result, somewhat misleading.

The labour slack measure is similarly nebulous. Labour force participation rates in many developed economies like Australia, the UK, and New Zealand are at record highs. Were it not for this jump in the number of people looking for work, Australia’s jobless rate would be below 4 per cent.

But this has not yet manifest in the US where participation rates are miles below 2001 levels. It is, however, possible that thoughtful policy measures could, if enacted, animate the inert labour supply displaced by the crisis (or, as many researchers believe, by pervasive dependencies on prescription drugs). To be clear, I remain a long-term inflation hawk because I am convinced politicised central banks and treasuries will over-stimulate economies.

Setting aside duration and slack, Dr Slok concludes that “almost all other indicators, ranging from cost pressures generated by that limited slack, the cyclical components of demand (housing, durables, and investment spending), confidence, corporate and household leverage, delinquencies and default rates, bank lending standards, margins and earnings, all suggest mid- or in some cases even early-cycle”.

And he warns that “limited slack by itself does not end the cycle”. “What does is either the cost pressures it generates, or stretched spending, leverage, overconfidence and other excesses that it has historically coincided with, [yet] none of these currently appear to be in place”.

In the last three US economic cycles, the “late” phase lasted between two to four years, which implies that a recession may not materialise until 2021. Crucially, any improvements in labour force participation or productivity would stretch this out further.

Exiting your portfolio too early in the cycle can be extremely costly given average market returns in the first half and second half are similar. “The timing of the move from late to end cycle is always unclear in real time and if the cycle goes on for longer it would imply significant foregone returns amounting to a median cumulative 42 per cent during the late cycle phase [of the last three episodes],” Slok says.

Across the asset-classes I concentrate on, the price action of late indicates investors may be starting to shrug-off late cycle blues. This column argued the listed hybrid market had become cheap in March, and we have seen a striking rally in prices since June in particular. The Solactive ASX Hybrids Index is up 2.2 per cent since June 1 before franking (and by 2.7 per cent since the end of March). Five year major bank hybrid spreads have crunched in from 406 basis points over the quarterly bank bill swap rate to 345 basis points over.

There has also been a nascent rally in global investment grade credit with spreads compressing, furnishing capital gains for those prepared to buy during the recent sell-off. Within this domain there has been a renewed bid for non-bail-in-able senior bonds, which are becoming increasingly scarce in a world dominated by banks issuing bonds that are indeed bail-in-able by regulators to meet Total Loss Absorbing Capacity (TLAC) rules. Read more here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

1 topic

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment