ASX Breakout!

Last week was a down week for global equities in general, thanks in large part to US President Trump’s threats to impose even more tariffs on Chinese and European imports. So far at least, however, what’s apparent is that countries are not bowing to Trump’s threats. That said, markets are still assuming (with some reason in my view) that some form of negotiated settlement will eventually be reached, or that at least escalation won’t continue much longer.

Indeed, as we’ve seen with his overturning of the forced separation of children from their asylum seeking parents at the Mexican border (a ploy which failed to get Democrats to agree on a bill to fund the Mexican Wall), Trump has the capacity to back down if he senses it’s a losing fight. And it strikes me that few in US industry are clamouring for Trump’s trade “assistance” given the economy is already booming, and many will be hurt by either higher import costs and/or lost export sales if he keeps up the fight.

While it seems ludicrous to worry that imports of steel, aluminium and cars from friendly allies threaten US national security, Trump is on stronger ground complaining about China’s protectionist policies. But to the extent he really cared about the latter, he’s be much better advised pursuing specific grievances in earnest through established World Trade Organisation procedures. Indeed, he might actually enlist the support of Europe in this quest!

In other news last week, OPEC appeared to agree to a moderate increase in oil production, meaning the overall global supply-demand balance is likely to remain relatively tight. At issue is that OPEC is already producing less oil than its current agreement allows for, due to capacity limits and supply-side disruptions among several smaller members. OPEC appears to have tacitly agreed to let Saudi Arabia, which does have spare productive capacity, to fill this gap for the time being. All up, it’s likely to keep oil prices relatively firm, and there’s an increased chance Brent crude prices might re-test $US 80 again.

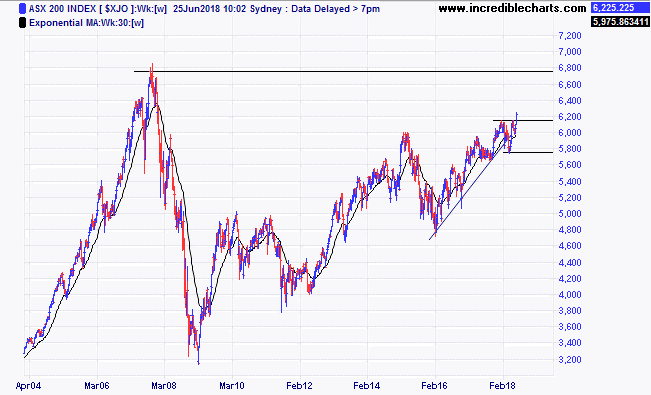

The other highlight last week was the impressive strength in the local equity market, with the S&P/ASX 200 rising 2.2% and breaking above recent weekly resistance levels around 6,150. It’s now seemingly blue sky ahead technically, with the next key resistance level 8.4% higher at the pre-GFC high of 6,748 – reached way back in October 2007!

What’s driving the local market?

Several factors seem at play. A weaker $A is boosting the offshore earnings outlook for many companies, while the associated strength in the $US has hurt some emerging markets and helped Australia look relatively less risky for globe-trotting investors.

Banks have also rebounded of late on the view that the worst of the Royal Commission negative headlines are potentially behind us.

More broadly, the recent decline in global bond yields due to simmering trade fears has sparked some renewed interest in yield plays – of which Australia has many!

To confirm the local market is now trending up, it should now be able to hold the 6,000 level, though I suspect it may still take a while – possibly even a year – to re-test previous peaks.

Week Ahead

There’s little on the data front globally this week, meaning attention is likely to remain focused, unfortunately, on the global “trade wars”. That said, the Fed’s preferred US inflation measure – the core private consumption expenditure deflator or “PCE” – is released on Friday and is expected to show annual inflation only edging up a little, from 1.8% to 1.9%. A stronger result would obviously grab market attention given lingering fears over the US inflation and interest rate outlook.

In Australia, home sales and private credit data on Thursday are likely to further confirm the softening outlook for local housing demand.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment