ASX hybrid liquidity soars 160% as spreads improve

I am often asked what liquidity is like in the ASX hybrids market, and it is generally better than most people appreciate. And contrary to popular myth, liquidity improves during times of market stress, which is one of the benefits of investing in an transparent exchange-traded security that trades actively every day.

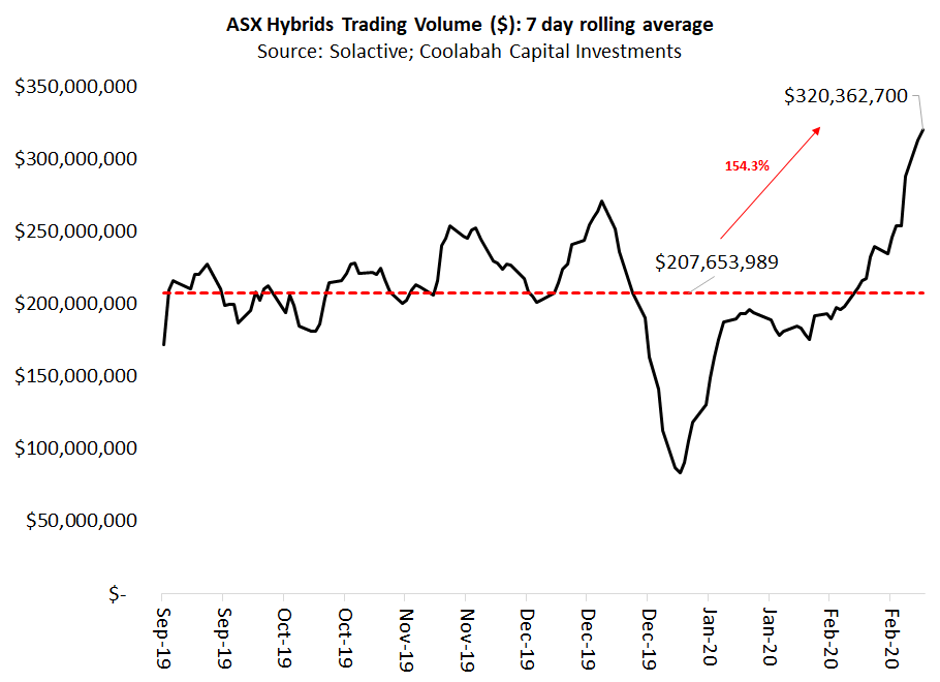

Since September last year, about $207m worth of ASX hybrids have traded every seven days. But as was the case when Labor announced their proposal to dump cash refunds on franking credits in 2018---which spooked many naive investors out of the hybrid market---we have seen a huge increase in hybrid liquidity during February 2020 as the equity market slumped. As my chart below shows, the rolling 7 day trading volume has jumped from around $200m in late January to over $320m in February. That's a 154% increase in hybrids trading volume over its average level since September 2019.

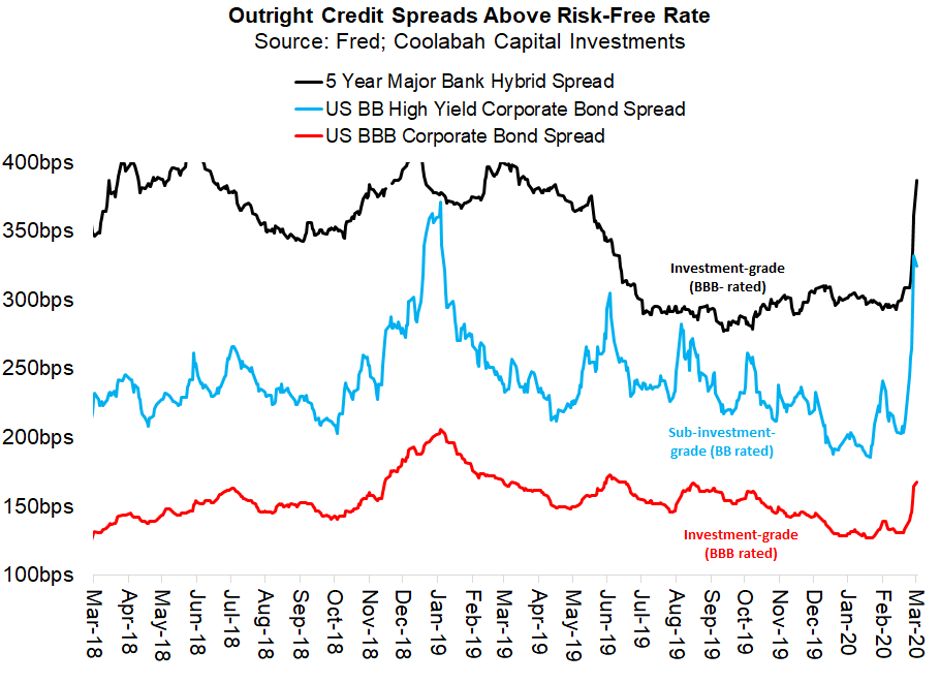

While the ASX hybrid market massively outperformed equities in February with just a 1.7% loss (cf. equity's 8.2% drawdown), there was a very sharp increase in the credit spreads hybrids pay above the quarterly bank bill swap rate (BBSW). In particular, the spread on 5 year, BBB- rated (ie, investment-grade) major bank hybrids jumped from about 277 basis points to as high as 367 basis points (bps) between January and the final days of February. Following a huge rally on Tuesday, when hybrid prices jumped more than 1%, spreads have normalised somewhat to around 340bps above BBSW. That translates into a total yield of about 4% annually.

What is interesting is that you get much better outright credit spreads on the major banks' ASX hybrids than you do on US high yield corporate bonds with inferior BB credit ratings, as you can see in the chart above (compare US high yield, which is the blue line, with ASX major bank hybrid spreads, which are the black line). Specifically, BBB- rated major bank hybrids currently pay about 62bps per annum in extra spread over BB rated US high yield and about 219bps per annum more than BBB rated US corporate bonds. And this is despite the fact that bank risk-weighted leverage has more than halved since 2007 while US corporate leverage is back above its pre-GFC peaks.

Of course, many mums and dads are also inherently more comfortable with the business model risks of the major banks as compared with offshore high yield borrowers or even investment-grade companies in the US that do not have the benefit of government guaranteed deposits and access to the RBA's liquidity facilities.

The 90bps increase in ASX hybrid spreads has now put them back to the levels that prevailed around the time of the election when investors were (incorrectly) worried about losing the cash refunds on their franking credits. (Readers might recall that I long argued that they would not lose these cash refunds, either because of a ScoMo victory or as a result of the Senate's staunch opposition to the proposal.)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Disclaimer: This information has been prepared by Smarter Money Investments Pty Ltd. It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Past performance is not an indicator of nor assures any future returns or risks. Smarter Money Investments Pty Limited (ACN 153 555 867) is authorised representative #000414337 of Coolabah Capital Institutional Investments Pty Ltd, which holds Australian Financial Services Licence No. 482238 and authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271.

1 topic

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment