Australian sharemarket wins gold

Each year Credit Suisse produces the Global Investment Returns Yearbook in collaboration with the London Business School. It is an analysis of the long-run performance of stocks, bonds, bills, inflation and currencies. This year’s book emphasises the importance of a multi-asset class portfolio to smooth returns and achieve investment goals. It proves that equities remain the best long-run financial investment globally ahead of bonds and bills, having enjoyed an inflation adjusted (real) rate of return of just over 5% since 1900. But it also shows equities experience periods of high volatility and certain decades have produced a negative real return.

The volatility of markets means that even over periods as long as 20 years, we can experience “unusual” returns. For example at the start of 2000, the real return on global equities for the previous 20 years had been 10.6% p.a. But over the next decade, the real return was -1.3% p.a. Thus, an investor must take into account their own investment horizon and the acceptable volatility when constructing a portfolio.

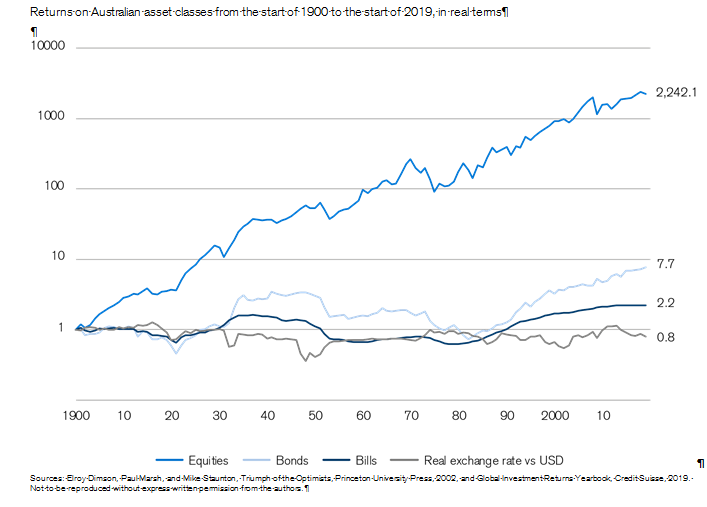

Australian Equities Best Real Return in USD

The Australian equity market has shown itself to be an attractive investment destination over the last 119 years. In USD terms, its return of 6.5% p.a sees it as the best performing market, slightly exceeding the US. The AUD return of 6.7% p.a since 1900 sees it as the second best performing market after South Africa. Not only was it the best performing market in USD it also had the second lowest standard deviation, or volatility, second only to Canada. US market volatility was sixth highest. The equivalent of 1 Aussie Dollar invested in 1900 has grown to AUD2,242.1. Australia also ranks well in terms of real dividend growth, having the fifth highest level of growth. Interestingly, the top six countries in terms of real dividend growth are also (but with a different ranking) the six best performing markets. These returns do not include the positive impact of franking on after tax returns. AUD bonds returned 1.7% p.a in real terms over the same period.

Emerging Markets to Become a Larger Part of Portfolios

The yearbook also highlights the potential in emerging markets (EM) and China in particular. Since 1950 EM have outperformed developed markets (DM), but this has not been the case in the last 10 years. EM are responsible for 40% of world GDP and are home to 59% of the world’s population. Yet, EM and frontier stock markets combined account for only 12% of world market capitalisation. The reason for this is not due to the size of the relevant economies or lack of growth. In fact, since 1980, EM countries have doubled their share of world GDP. The main reason appears to be the world indexes are based on the investable universe for a global investor. The indexes exclude or underweight markets that are difficult to access, have low free float weighting and screen illiquid stocks. Thus, until 2018 the large local Chinese A share market was excluded from the MSCI EM Index because of the difficulties of access. However, as China and other EM countries modernise their exchanges, improve access, company founding families sell down holdings and global investors gain confidence in governance, the share of EM in world indices, and portfolios, will inevitably increase.

Style Impact on Investing

Finally, the yearbook considers the success of different styles of equity investing. The “value” versus “growth” debate stirs plenty of passion. Value, the purchase of stocks with an emphasis on low valuation, has had a poor run as a style since 2007. No doubt the rise of large successful technology stocks has contributed to this. But giving value managers hope is that an analysis of US data since 1927 shows value stocks, defined as those having high book value versus market value, have generally done better than their growth counterparts.

Other factors are at play in stock picking such as size (small caps versus large), income and yield, momentum and risk. The conclusion is that it is hard to predict or time when a particular style or factor will dominate. The lesson is to diversify portfolios across multiple factors and remain humble as to one’s ability to pick the winning style in the short term.

Never miss an update

Stay up to date with the latest news from Credit Suisse Private Banking by hitting the 'follow' button below and you'll be notified every time I post a wire. Want to learn more about Credit Suisse Private Banking? Hit the 'contact' button to get in touch with us.

Credit Suisse Private Banking specialises in asset diversification, holistic wealth planning, next generation training, succession planning, trust and estate advisory, philanthropy. Find out more here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in Australia. He is also Head of Investment Solutions and Products.

Andrew has been investing on behalf of clients for over 24 years and was the founder of the Credit Suisse Discretionary Portfolio Management service in Australia. He has managed single and multi asset class portfolios for major superannuation funds, institutions, ultra-high net worth individuals, not for profits and private clients and is Chairman of the Australian Investment Committee.

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Andrew McAuley is a Managing Director of Credit Suisse Wealth Management Australia. As Chief Investment Officer, he is responsible for developing discretionary and advisory investment strategies across multi asset class portfolios for clients in...

Expertise

Comments

Comments

Sign In or Join Free to comment