Bank Note$ - TS Lim's quarterly bank review

The sector turned in another positive performance in the December period (in line with expectations) with strong contributions again from the domestic retail and business banks. NIM may have been lower in the period due to asset price competition but we are seeing an easing in retail and wholesale funding costs. Positive repricing across most mortgage fronts, improving free fund effect/easing liquidity drag as long rates begin to rise and steady business volumes (in line with managing for profitable growth) should also provide tailwinds in the second half and beyond especially for the majors.

With the exception of volatile life insurance earnings, other income was generally better in the half with higher commissions and lending fees, markets income (favourable sales and trading conditions) and general insurance contributions. On an underlying basis, revenue growth on a pcp basis was generally positive. Combined with strict cost management, this resulted in positive “Jaws” in the December period.

Asset quality remained relatively steady (GIA and 90 days past due loans manageable despite ongoing mining town stresses in WA and QLD) in a low unemployment and low interest rate environment while higher IP charges were offset by CP releases due to portfolio improvements. Regardless, the sector BDD charge remains low (4-17bp vs. 20-30bp through-the-cycle for the majors, 1-13bp vs. ~20bp through the cycle for the regionals) and higher levels have thus been factored into our forecasts.

Interim dividends were not reduced. CBA had a ~1% increase to 199cps, BEN’s was unchanged at 34cps and SUN had a 10% increase to 33cps while reaffirming its commitment to returning surplus capital in the medium term. These outcomes reflected strong organic capital generation despite the majors absorbing higher mortgage risk weights on 1 July. APRA will likely push for higher capital requirements but we believe the banks (and especially the majors) will be given sufficient time to achieve these (and to be adequately funded by their respective DRP).

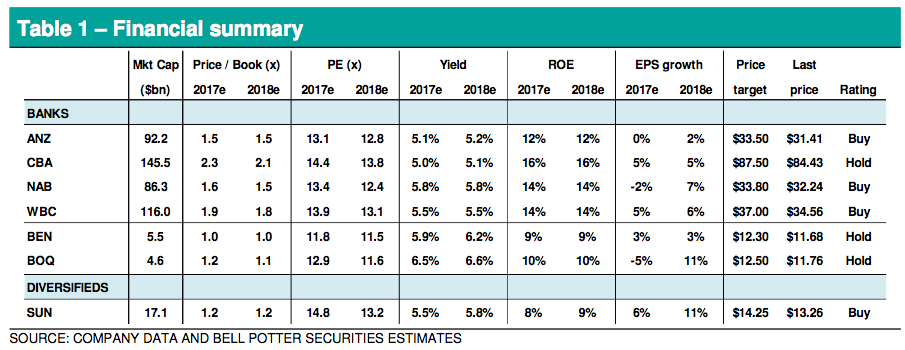

Major bank picks: WBC, ANZ and NAB

Forecast changes from mortgage rate rises: NAB cash NPAT +3%; and WBC cash NPAT +2%. Price target changes: ANZ slightly up to $33.50; NAB +4% to $33.80; and WBC +2% to $37.00. All ratings are unchanged and we remain positive on the majors relative to the regionals. Majors’ pecking order: WBC; ANZ; NAB; and CBA.

Full report available here:

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bell Potter Securities is a leading Australian stockbroking, investment and financial advisory firm that provides a comprehensive offering of financial services to a diversified client base that includes individuals, institutions and corporations.

7 stocks mentioned

Stockbroker

Bell Potter Securities is a leading Australian stockbroking, investment and financial advisory firm that provides a comprehensive offering of financial services to a diversified client base that includes individuals, institutions and corporations.

Expertise

Stockbroker

Bell Potter Securities is a leading Australian stockbroking, investment and financial advisory firm that provides a comprehensive offering of financial services to a diversified client base that includes individuals, institutions and corporations.

Expertise

Comments

Comments

Sign In or Join Free to comment