Bank Note$: Wayne's world

Whenever the APRA Chairman gives a speech, there is a strong likelihood that bank share prices will head south. This is especially true when topics include the need for more bank capital and unsustainable mortgage lending practices. However, the negativity is sometimes balanced by positive speeches about the strength of the Australian banking system, banks closing the capital gap and orderly capital changes. APRA’s speeches rather than ASIC’s appear more negative for the banks as a whole.

Be that as it may, APRA is likely to provide further capital clarity in the next few months (this is in addition to recently-introduced speed bumps for interest-only and investor home lending). As such, we revisit in this note the potential implications on the Australian banks. Based on last reported data, it comes as no surprise that ANZ and NAB should be most resilient of the major banks. Of the regional banks, BOQ and SUN Bank would top the chart. Our forecasts assume 10-12% DRP rates for ANZ, NAB and WBC and 20% for CBA, and it is our view that this capital lever will remain a key capital funding source for the major banks. We believe a 30% average mortgage risk weight will be the likely outcome as this would provide a more realistic level playing field for the regionals (i.e. 35% would not produce much benefit to them).

The above should also be considered with the additional lending speed bump introduced on 31 March (limiting the flow of new interest-only lending to 30% of total new residential mortgage lending and inclusive of the 10% benchmark growth for investor lending). Given NAB’s smaller interest only portfolio at ~32% of the total, the impact on cash NPAT would be minimal (all else being equal). This would be followed by ANZ, CBA and WBC (again no surprises for the mainly-retail oriented banks). The overall impact remains small and we believe further mortgage repricing should go some way towards alleviating the above opportunity cost.

Prefer NAB, ANZ and SUN

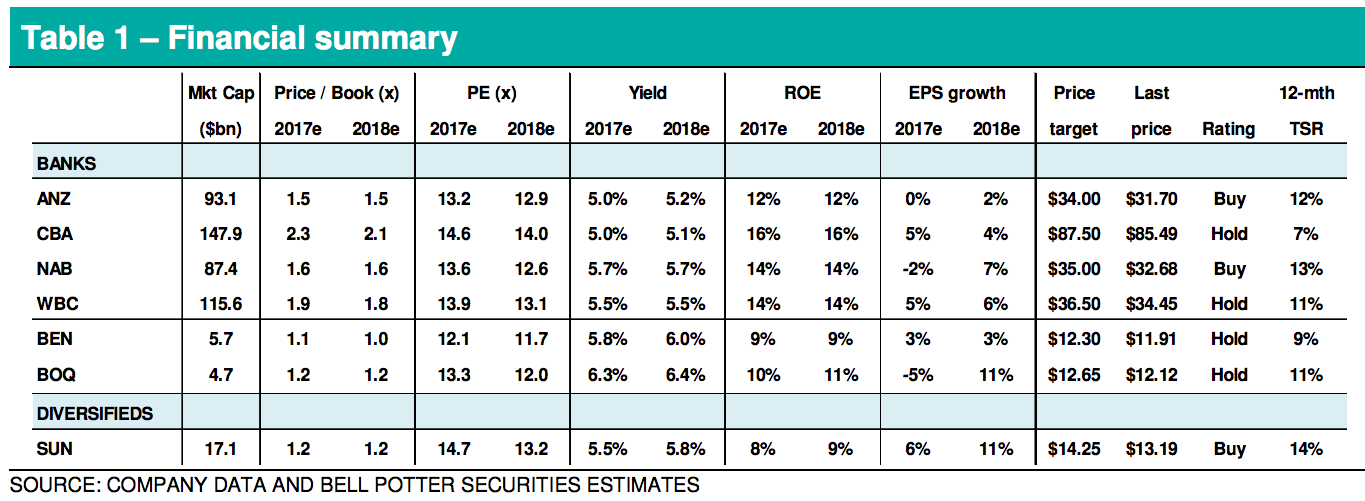

While there are no changes to our forecasts, we have revised some price targets after benchmarking domestic retail and business bank SOP valuation multiples against CBA: ANZ $34.00 (previously $33.50); NAB $35.00 (previously $33.80); and WBC $36.50 (previously $37.00). The only rating change relates to WBC, now a Hold (previously Buy) purely based on valuation. NAB and ANZ are our top major bank picks while SUN remains our deep-value diversified play (general insurance and banking top line, efficiencies and further surplus capital in the event of Life sale).

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bell Potter Securities is a leading Australian stockbroking, investment and financial advisory firm that provides a comprehensive offering of financial services to a diversified client base that includes individuals, institutions and corporations.

5 stocks mentioned

Stockbroker

Bell Potter Securities is a leading Australian stockbroking, investment and financial advisory firm that provides a comprehensive offering of financial services to a diversified client base that includes individuals, institutions and corporations.

Expertise

Stockbroker

Bell Potter Securities is a leading Australian stockbroking, investment and financial advisory firm that provides a comprehensive offering of financial services to a diversified client base that includes individuals, institutions and corporations.

Expertise

Comments

Comments

Sign In or Join Free to comment