Bassanese Bites: BetaShares Global Market Review

Global Markets

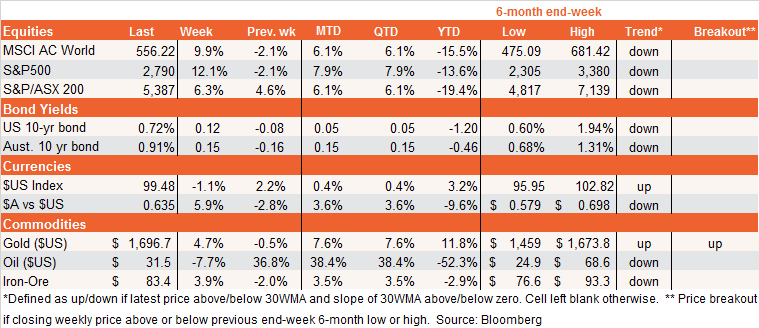

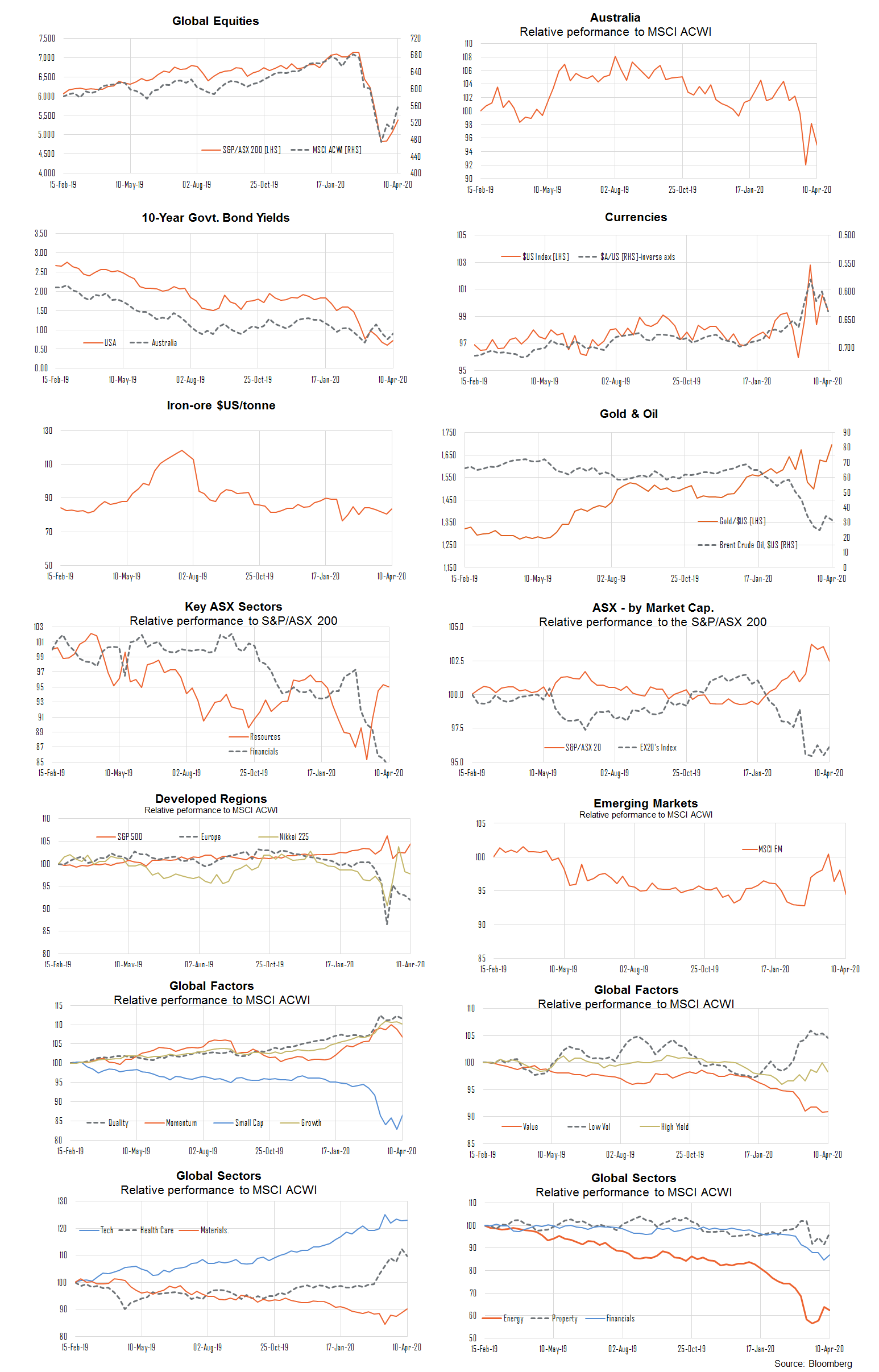

The S&P 500 rebounded a lazy 12% last week as Wall Street again easily managed to look past weak economic data and focus instead on yet more Fed support programs and further progress on “curve flattening”. Markets remain hopeful that as US infection rates ease, the US can eventually lift social distancing restrictions and the economy can therefore enjoy the much hoped for “V-shaped” recovery. Indeed, last week the Fed conveniently timed its latest support announcement (purchases of local government debt and underwriting of bank loans to embattled small businesses) to coincide with another shocking weekly jobless claims report – and sure enough, the market focused on the former!

Of course, we should not forget that strong rallies – such as we’ve seen in recent weeks – are typical in bear markets and the sharper the initial decline, the faster is often the first bounce. That said, compared to the GFC, it should be said what is supportive of markets this time around is that 1) stimulus is stronger and more timely, as given this recession is “undeserved” there’s less push back against bailouts and moral hazard and 2) the leading US sector this time around – technology – is less negatively affected by lockdowns than others. Against this, we’re still facing the worst US recession since the Great Depression.

Whether the rally last remains to be seen, I still suspect we’re due for at least one decent re-test of previous lows at some stage. For starters, even if the US moves past peak infections, it will still face months of lingering restrictions (given a vaccine and better treatments are still months away) and the ever-present risk that they could be re-imposed in a heartbeat if a second wave emerges. This is hardly a recipe for a V-shaped recovery in business and consumer spending.

Another test for markets will come this week with the start of the Q1 US earnings reporting season. If there’s any saving grace, earnings were still holding up OK for much of Q1, and companies are likely to refrain from providing much forward “guidance” if they can avoid it.

That said, as I’ll outline in a blog post this week, it’s still likely that both 2020 and 2021 US earnings (the latter if only due to base effects) will eventually need to be slashed in coming months, which at current levels would have the market trading at more than 20 times forward earnings – something not seen since the tech bubble. Even today, the market is now trading at a lofty 17.3 times forward earnings. Maybe the market can “look through” this earnings slump – in a way it has never done in past recessions – but given likely persistent uncertainty regarding the economic rebound, it’s a big ask.

Australian Market

As in the US, our market is also hopeful that a peak in infection rates will ease restrictions. But again markets may well be disappointed over how fast this can happen and we will still need to endure several months of shocking economic data and a slashed corporate earnings and dividend outlook.

Indeed, Treasury itself is now publicly forecasting a doubling in the unemployment rate to 10% by June – even with the massive $130b wage subsidy. There’s also open talk of many companies cutting their dividends, includes the banks.

The testing data continues this week, with the NAB business survey today and the Westpac consumer confidence survey tomorrow. The March labour force report on Thursday is also expected to show a loss of 40,000 jobs and a lift in the unemployment rate to 5.5%

Has the market bottomed? It’s a big ask.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment