Bassanese Bites: RBA rate cut tomorrow

Week in Review

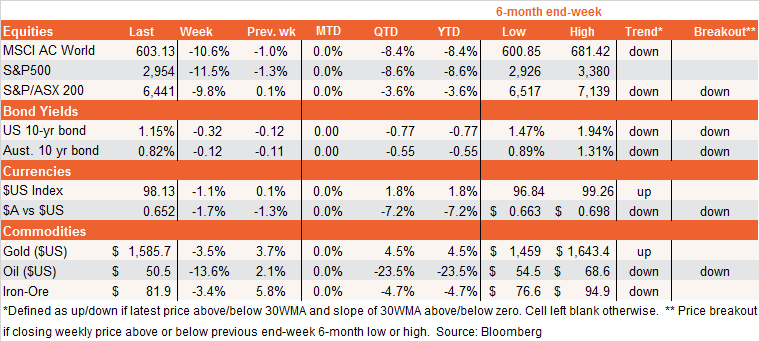

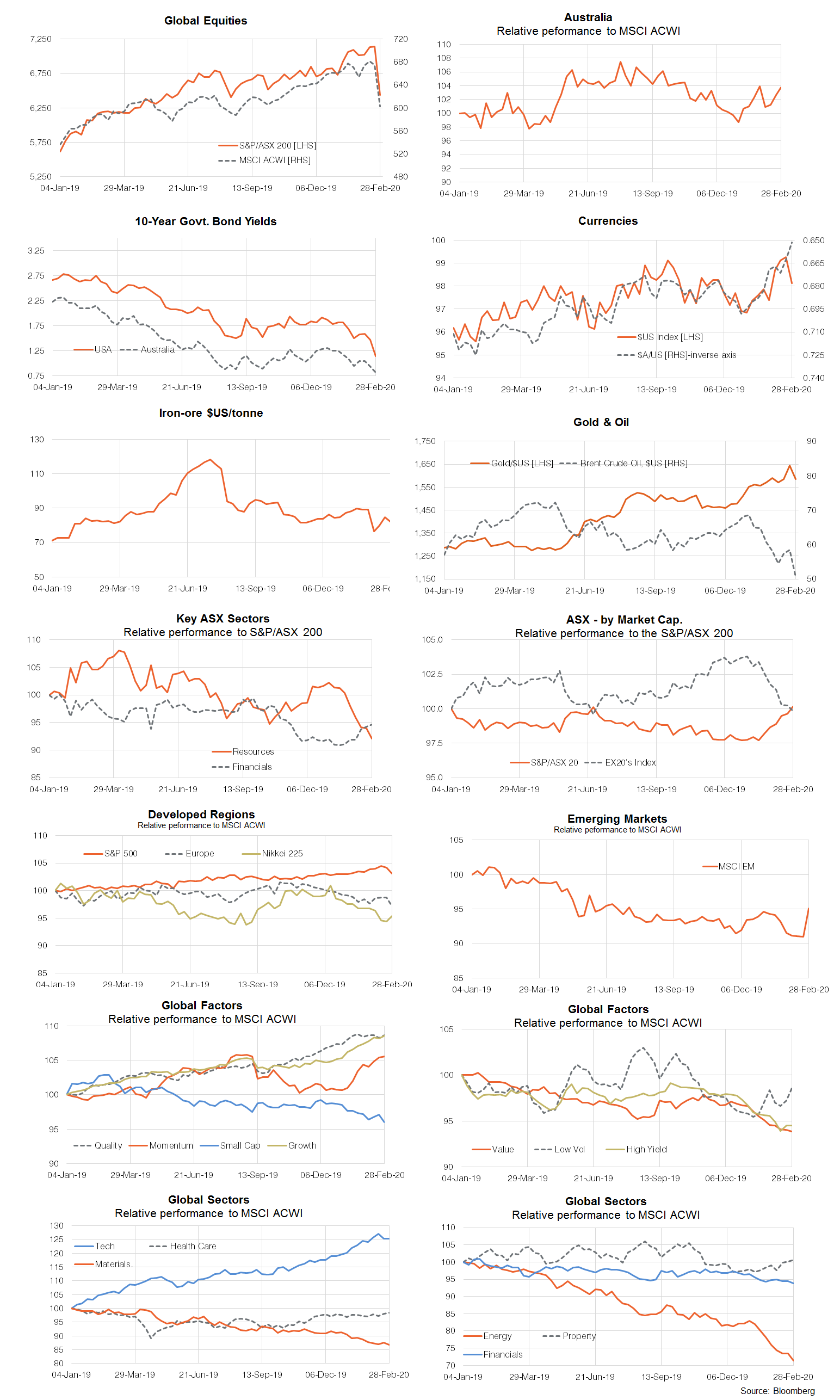

Where to begin? Clearly fears of the coronavirus took centre stage last week, causing the biggest one week drop on Wall Street since the financial crisis. It’s also the fastest “correction” (i.e 10% decline from previous peak) in history. Are markets over reacting? It’s hard to be certain they are, as while the coronavirus outbreak appears to have stabilised in China, the new concern is its potential spread to other major economies such as Europe and the USA. On this score, history suggests it may be wishful thinking not to expect a sharp rise in new cases in these major centres of global economic activity over coming weeks, which could further unnerve global markets.

With 88,000 affected, this virus outbreak is already 10 times larger than the SARS outbreak of 2003. It could potentially get as bad as the Swine Flu outbreak of 2009 which infected an estimated 1 billion people, or 15% of the global population. The Swine Flu’s death rate, however, was only around .02% – whereas the coronavirus fatality rate is currently around 3% (the SARS death rate was 10%). In the USA, the Swine Flu affected around 60 million, with around 12,000 deaths.

Helped by a low fatality rate, however, the Swine Flu did not materially affect global markets through 2009, which remained focused on recovering from the GFC. With equity markets more extended this time around, and the death rate higher, this time could be different. As a result, I can only repeat what I said here last week:

With global equity PE valuations at historic highs (albeit arguably justified by low bond yields) and markets having shrugged off virus concerns so far, it’s probably reasonable for a pullback of sorts to kick in over the next few weeks (or even months) as the clear negative economic shocks – even if considered short-term – are absorbed. Also still troubling are reports of virus outbreaks outside of China – with South Korea, Italy and even Iran new areas of concern. With with regard to the virus itself, therefore, it’s still seems too early to conclude the worst is over.

Of course, the economic data around the world is likely to be universally bad in coming weeks also as production and tourism are disrupted. China’s weekend PMI reports on both manufacturing and services were shocking (composite PMI covering both services and manufacturing sank to 28.9!). Trying to help will be central banks, with the Fed last week hinting it will likely cut rates at its March 17-18 meeting – if not before.

Week Ahead

Markets will be fretting nervously over possible (inevitable?) further coronavirus outbreaks in the USA. There would then be a cycle of announced travel and trade restrictions, which would then be inevitably felt in the economic data in the months ahead. From a markets perspective, however, what will matter is when the rate of new cases in the USA peaks – which could still be several months away.

In Australia, following the recent rout in global stock markets and the weekend collapse in Chinese industry indicators, I have brought forward my expectation for the next RBA rate cut this year from August to March (i.e. this week). The RBA will cut rates on Tuesday to get ahead of the likely slump in both business and consumer confidence in the months ahead. A follow up rate cut in May is also now anticipated, with “quantitative easing” now at least a 40% chance in the second half of the year.

Will rate cuts more hurt than help confidence? Perhaps. But in time of apparent crisis, the RBA will want to feel ahead not behind the curve. Indeed, Australia now faces its greatest risk of recession since the global financial crisis, with private demand already weak, and with much less fiscal and monetary firepower to respond.

The Federal Government also needs to seriously consider an economic statement, outlining further stimulus measures before the May Budget. There is no time to wait.

Underlining our current challenges, Q4 GDP on Wednesday is likely to show the economy remained sluggish late last year, with growth running at around a 2% annualised pace at best.

This too shall pass

If all the above appears too dramatic, I suggest to readers than we’re still likely only facing a short term shock to economic growth, with good prospects of some recovery in the second half of the year if the virus is able to to contained globally within three months or so. Investors with a long-term time horizon might in fact see the next few weeks and months as a buying opportunity.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment