Beyond the Jargon: Short Selling

Short sellers are not the most popular participants in financial markets. Investors may recall that during the height of the financial crisis in ’08 and ’09, short sellers were blamed for some of the volatile price movements, particularly in major banks, and short selling was subsequently banned in many developed markets. So, are short sellers the enemy of long-term investors? Or is there a role for short sellers in setting more efficient prices?

Alternative terms: Shorting, going short.

Short explanation: When an investor sells an asset that they do not own, with the intention of purchasing it back at a lower price in the future. If successful, the investor profits from the fall in the value of the asset.

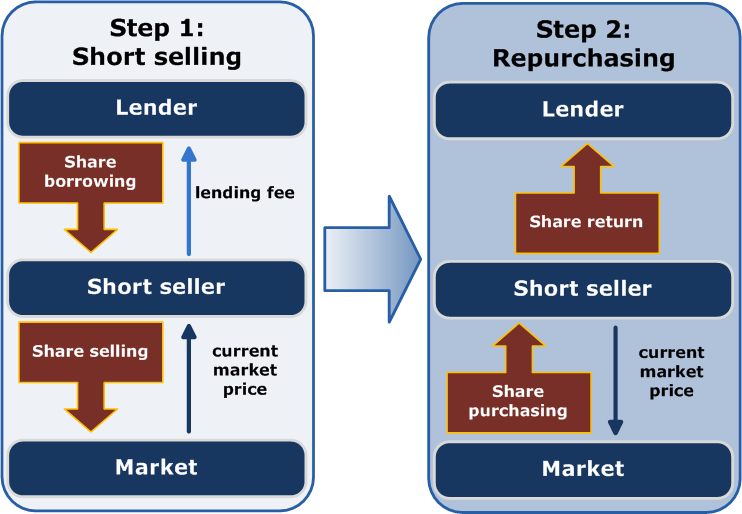

More detail: While short selling involves selling an asset that’s not owned, it’s not as simple as just going to your broker to sell shares in a company. If you wish to short sell an ASX-listed company, it must first be borrowed from an owner. Large institutions, particularly super funds, can enter into securities lending agreements, where they’re paid a fee to lend their stock to a short seller. In addition to the fee, the short seller must also cover any dividends that are paid while they’re short the stock; this can make it very expensive to maintain a short position for an extended period of time.

The Mechanics of Short Selling

Image credit: Wikimedia Commons, User: Grochim

Image credit: Wikimedia Commons, User: Grochim

In 2008, ASIC introduced a “ban on short selling and a reporting system to maintain an orderly market and mitigate the risk of market abuse.” In a review in 2012, ASIC found that the short selling ban “broadly met their regulatory objectives by reducing the risks that might have occurred as a result of unrestricted short selling.”1

Since the GFC in particular, perceptions of short sellers have been quite negative; that they’re predators taking advantage of long-term investors and driving down stock prices. But short selling is an important, if lonely and difficult activity.

"I would line them up against the wall and shoot them, all the short-sellers," Harvey Norman's Gerry Harvey, as reported in The Sydney Morning Herald, Nov 21, 2008.

A regular ‘long only’ investor has a lot to support them. Dividends supplement capital gains, markets tend to move up over the long term, gains are unlimited, while losses are capped at 100%. For an investor who owns an asset, their exposure increases when the market moves in their favour, while poorly performing positions become less significant.

For short sellers, all of these positives are turned on their head. Dividends are a cost, the rising tide of markets becomes your enemy, the gains are capped at 100%, and the losses are unlimited. As a position moves against you, your expose gets higher and higher – hence the dreaded ‘short squeeze’, when higher prices force short-sellers to buy stock to cover their position, sending the stock even higher.

I asked Chad Slater, joint-CIO of Morphic Asset Management, who uses shorting as part of his strategy, for his view: “While there is no ‘secret sauce’ to shorting that makes it beyond individual investors, it is quite a different mindset for investors. The usual rules of buy and hold don’t apply. I’d advise against most individual investors doing much of it unless they have a lot of discipline and focus.”

Despite all these difficulties, short selling plays an important role both at a portfolio level and for the overall market.

At the portfolio level, short selling allows an investor to hedge out particular risks, express a negative view on a stock, and profit from both the upside and downside moves in the market.

On this topic of risk, Chad told us: “One of the biggest misconceptions we find is that the idea that shorting increases risk. Within a well-constructed portfolio, it actually lowers your day to day risk. What it is, though, is ‘brittle’. What I mean by that is think of it like standing on an empty coke can. It can support a lot of weight, but if twisted it can collapse on itself. Shorting not done in properly diversified portfolio and without risk rules can crush your returns like the coke can”.

At the market level, short selling has been found to increase liquidity, and increase market efficiency. Dr Don Hamson found in 2008 that the ban on short selling during the GFC actually decreased liquidity and increased volatility2. Swedish Economist, Stefan Karlsson, has stated that “the ability to sell short helps move markets closer to [an efficient price]3.

If you’re interested in learning more, Chad Slater from Morphic Asset Management penned a more in-depth guide to short selling in January 2016:

The Visual Capitalist has also prepared a great infographic explaining some of the broad concepts in an easy-to-understand visual format.

References:

1. ASIC

2. The FINSIA Journal of Applied Finance issue 4 2008

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium,.

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment