Bond markets power ahead

Anthony Doyle

Firetrail Investments

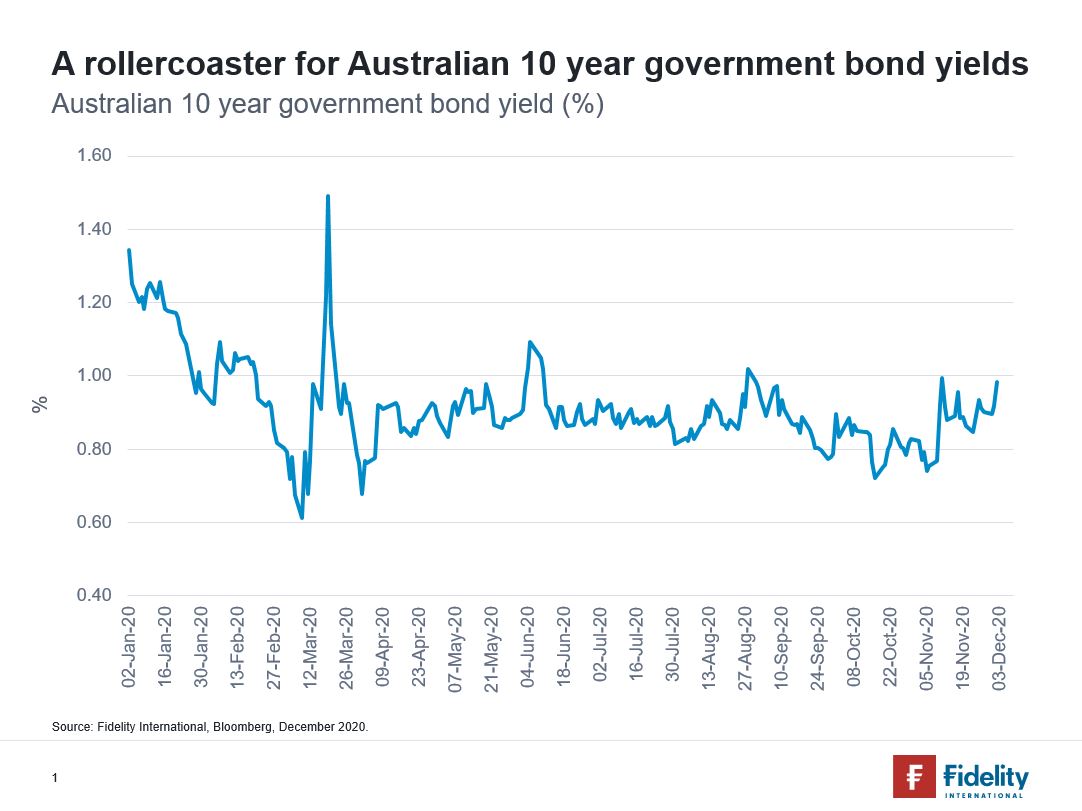

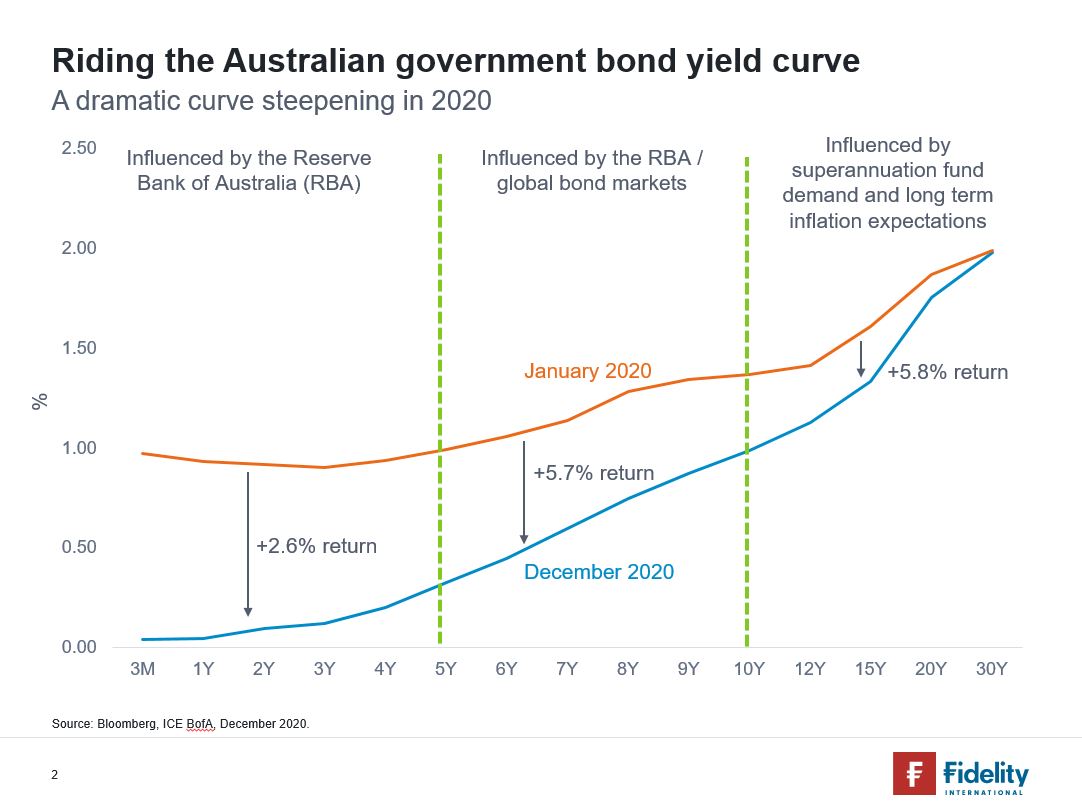

Australian government bond yields have collapsed in 2020, fuelled by the Reserve Bank of Australia’s unprecedented intervention in the market via yield curve control and quantitative easing. The 3-year government bond yield, heavily influenced by the RBA, has collapsed from 0.90% to 0.12% over the course of the year. Investors in the benchmark 10-year government bond have experienced a rollercoaster of emotions, with the yield falling to an all-time low of 0.61% on March 9 before spiking to 1.49% only 10 days later at the height of this year’s panic. The 10-year yield has largely been range bound since between 0.80 and 1.00%, and currently sits at 0.98%.

The action in the government bond market this year has led to a dramatic steepening of the yield curve. Short dated yield plummeted the most, driven by a change in expectations of Australian interest rate expectations and the RBA’s manipulation of 3-year government bond yields via yield curve control. Despite the large fall in yields at the short end of the curve, the best returns this year have come from the belly and long-end of the curve (5+ year maturities). Medium and longer dated government bonds are much longer duration and are hence more sensitive to changes in bond yields.

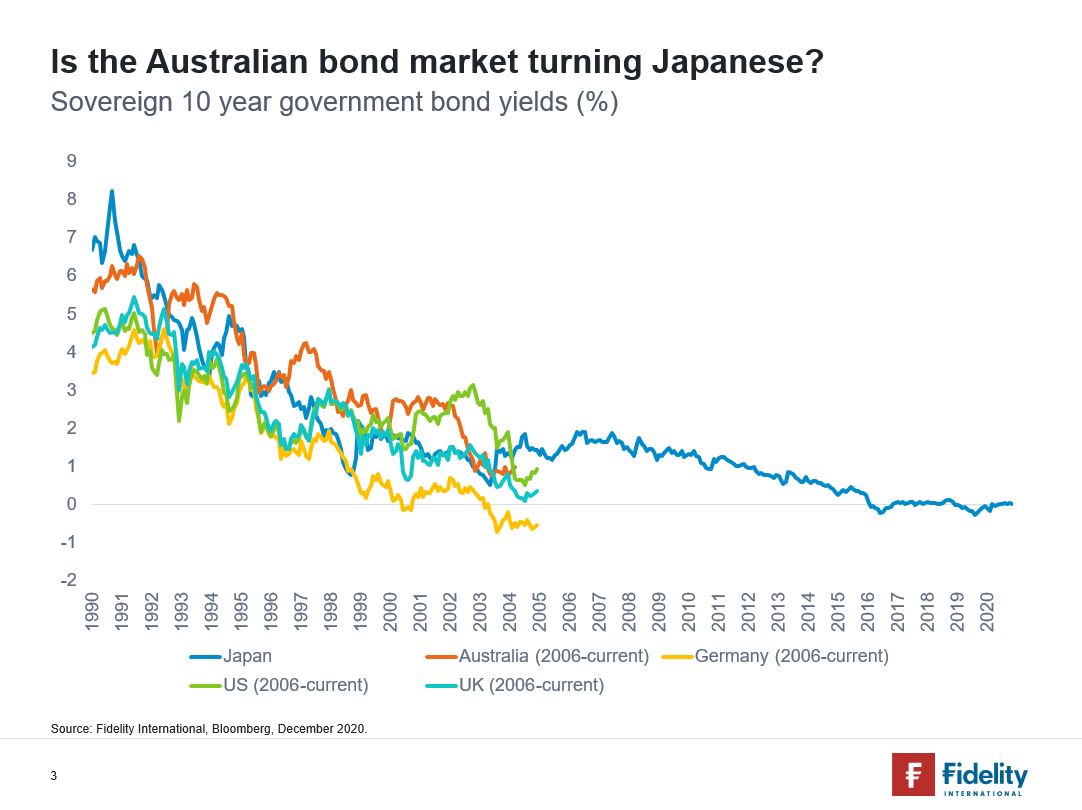

The question for Australian government bond investors now is how low will yields go? To help answer this question, it is useful to look at the experience of international government bond markets.

Japan’s economy in the 1990’s was embroiled in a cycle of low growth, low inflation, and increasing levels of government debt. It was the beginning of a recession that would last years - known as the ‘lost decades’ - and exposed Japan as being a nation predisposed to building excess saving at both the household and corporate sectors. It sparked what would become an era of unconventional policy measures by Japanese monetary and fiscal authorities, all aimed at boosting aggregate demand at a national level. Fast forward to 2020, and there are many parallels to be drawn from Japan thirty years ago, and how governments and central banks are attempting to stimulate their economies today.

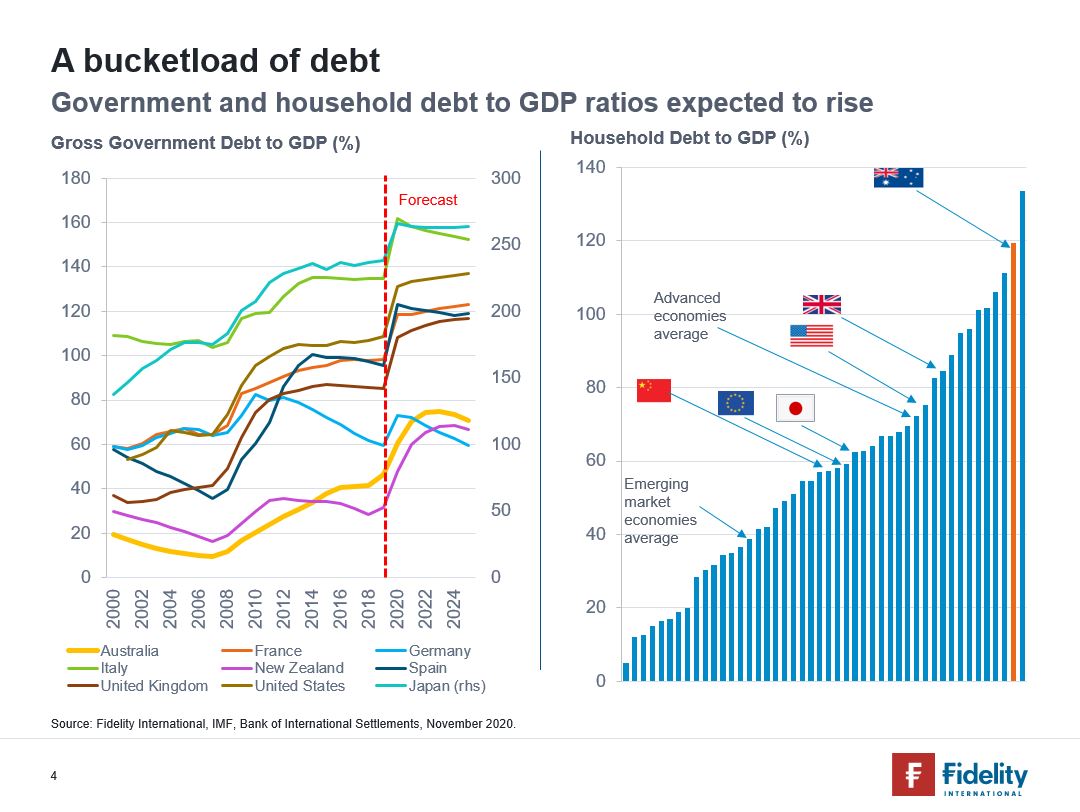

Australia’s government balance sheet came into the crisis from a position of strength, allowing the Federal government to implement one of the most stimulatory fiscal policies seen anywhere in the world. The effects were immediate which combined with our world-class experience of containing Covid-19, resulted in a strong return to economic growth in the third quarter of 2020. However, our vulnerabilities lie in the household sector, with Australia recording the second highest level of household debt to GDP in the world. These high debt loads on the household sector require low interest rates to enable the servicing of large mortgages and ever higher house prices to allow households to maintain high consumption levels.

Against the current backdrop of lower structural growth and low inflation, it’s fair to assume that central banks and governments will remain key actors in financial markets for some time to come. In Australia, it seems unlikely that the path for inflation will materially deviate from current expectations for at least the next 3 years or so.

With these challenges in mind, investors have grown reliant on policy makers to do all they can to support asset prices – perhaps justifying the disconnect between market and economic performance, and the changes in historical correlations that we have seen so far this year. Despite the global recession, we have seen equity markets continue to rally while bond yields remain anchored at low levels.

If developed market economies are turning Japanese, we can expect to see further downward pressure on government and corporate bond yields – not only because of lower growth and inflation expectations, but also because of the forced buying nature of domestic savings institutions. We can also expect to see Australian fixed income markets continuing to move into a much lower volatility phase that may last for some time, while corporate bond issuance, particularly from banks, is likely to be somewhat lower than in the past. In this environment, it would take a brave portfolio manager to have the conviction to short the Australian government bond market.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Enjoy this wire? Hit the like button to let us know.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

........

This document is issued by FIL Responsible Entity (Australia) Limited ABN 33 148 059 009, AFSL No. 409340 (“Fidelity Australia”). Fidelity Australia is a member of the FIL Limited group of companies commonly known as Fidelity International. Prior to making an investment decision, retail investors should seek advice from their financial adviser. This document is intended as general information only.