Boral Limited (ASX: BLD)

Boral Limited is a multinational company dealing in building and construction materials. Founded in Australia, it also has extensive operations in the United States and Asia. The company has over 12,000 employees working across over 600 operating sites. Boral was demerged from the ‘old’ Boral Limited in February 2000. The ‘old’ Boral Limited, comprising energy assets, was renamed Origin Energy. The spin-off assets, comprising building and construction materials, became the ‘new’ Boral Limited. Boral and Origin Energy are now separately listed companies on the ASX and are entirely independent of one another.

The ‘old’ Boral began as an oil and bitumen refining company under the name of Bitumen and Oil Refineries Australia Limited. It later changed its name to Boral Limited using the acronym of the company’s name.

Boral has changed its core business since its inception, and now has a diverse area of operations within the building industry, including asphalt,road line marking, concrete, plasterboard, timber, windows, quarry, landfill, transport, roof tiles, bricks and pavers. Boral also produces cement via Boral Cement (formerly Blue Circle Southern Cement).

Market Price: $4.87

Market Cap: $5.71b

The company has three main divisions as follows:

USG Boral

In early 2014, Boral Limited and USG Corporation formed a 50/50 joint venture known as USG Boral. With approximately 3,500 employees, USG Boral is a leading manufacturer and supplier of gypsumbased wall and ceiling lining systems, mineral fibre acoustical ceiling systems, metal framing,joint compounds, high-performance panels and accessories throughout Asia, Australia and the Middle East.

In Australia, USG Boral Building Products has plasterboard manufacturing plants in Queensland, New South Wales and Victoria; a specialty plasters and jointing compounds plant in Victoria; cornice plants in New South Wales and Victoria; an integrated national network of more than 50 specialist trade centres; and Australia’s largest residential wall and ceiling installation service – USG Boral Linings (UBL).

USG Boral in Asia is a multi-country plasterboard producer in the region. USG Boral in Asia has 21 manufacturing sites across China, Thailand, Indonesia, South Korea, Vietnam, India and Malaysia, producing plasterboard ceiling tiles and suspension systems, metal framing, jointing compounds and industrial plasters throughout the region.

Boral Australia

Boral Australia is a major supplier of products and materials to the residential and commercial construction, and roads and engineering markets. As one of Australia’s largest and most experienced construction materials suppliers, Boral has the resources and the expertise to perform for customers Australia wide. This division has many subdivisions producing concrete, quarry operations, asphalt, cement, logistics solutions, property management services, bricks, stone, roof tiles and timber for flooring markets.

Boral North America

The North America division combines the Construction Materials and Building Products businesses of Boral USA and Headwaters Inc., following Boral’s acquisition of Headwaters in May 2017. Boral North America has a national fly ash processing and distribution business and manufactures stone veneer, concrete and clay roof tiles, concrete block, light building products and windows for residential and commercial construction markets. Boral North America also has a construction materials business in Denver and has a 50% share of the Meridian Brick joint venture.

First Half Financial Year 2019 Result

On the 4th of February, Boral pre-empted their result with a disappointing trading update. The company officially reported on the 25th of February and the results were in line with the trading update. Net profit after tax (NPAT) was down by approximately 6% at $200 million even though sales increased by nearly 5% to $2.93 billion. Net debt was slightly higher than consensus at $2.3 billion and there was a small 0.5 cent increase in its interim dividend to 13c.

By divisions, the Australian result was slightly ahead of expectations with concrete prices up 3% and cement prices up 1%. Earnings were negatively impacted by an 8% decline in concrete volumes, less favourable geographic and product mix, project delays and weather challenges.

In the US, heavy rainfalls impacted volumes. The company is working to increase their fly ash supply and intend to implement price increases. The Headwaters synergies are performing as expected with the company on track to deliver US$25 million for the full year.USG Boral was weaker than expected mainly due to increased competition and a cyclical downturn in South Korea. Boral is in talks to take a much larger stake in the joint venture and reiterated their strong preference to use debt and asset sale proceeds to fund any further investment.

Outlook

Whilst the slowing Australian residential market is concerning, the CEO Mike Kane commented that he does not expect it to collapse, rather he thinks it will moderate over the next couple of years and then expects it to stabilise, followed by a recovery. He estimated the US residential market is approximately 5-6 years away from reaching its peak. Mr Kane thought the Australian infrastructure boom is not even half way in to the cycle and that there has been chronic under-investment in infrastructure in the US. He estimated there will be at least US$3 trillion spent on infrastructure in the US in the coming years.

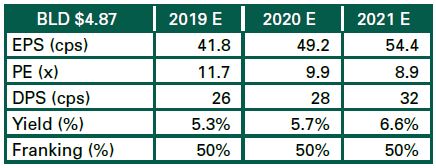

When you combine Boral’s attractive leverage to the emerging boom in infrastructure both here and in the US, appealing exposure to the US construction markets generally, USG improvement and further synergies from the Headwaters acquisition, we believe the investment case is still compelling. Whilst bad weather has plagued the company’s activities over the half, one must remember the work is still there and a bottle-neck of demand is waiting for Boral’s products. As such, we’d expect to see a significant skew to the upside in the second half of FY19. Trading on a 2020 P/E ratio of 9.9X and 5.7% yield, the stock is cheap relative to its peers and own history.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 topic

1 stock mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment