Brexit: Initial thoughts from the UK

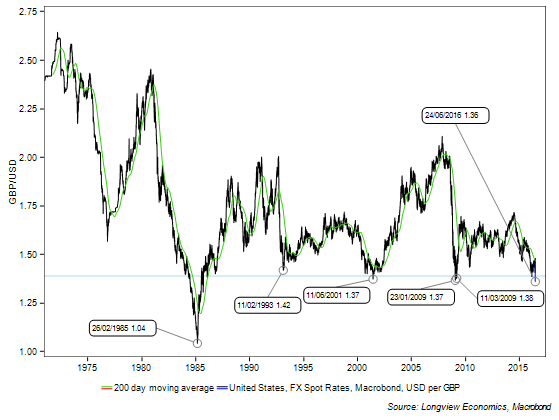

On Friday the UK has surprised markets by voting to leave the European Union (by 52% to 48%). Of the 12 regions of the UK – Northern Ireland, Scotland and London voted to Remain while the other 9 regions voted to Leave. The GB£ fell to an intra-day low of 1.32 Friday morning (down ~10.9%) i.e. a break below technical support of 1.37 – 1.45 (see FIG 1 below). The next key support level is ~1.03 (i.e. the mid-1980s lows). Article 50 is the part of the Lisbon treaty, which, once evoked, sets in motion a two-year process in which a member state can notify the EU council of its decision to leave.

The decision to trigger Article 50 is a decision for the UK Prime Minister alone and, once triggered, results in the UK’s ejection from the EU at the end of the two-year period (unless the rest of the EU unanimously* decides to extend the negotiations). In that time – i) the UK still votes on EU policy (& the timeframe could be extended if it’s agreed by all EU member states); ii) The UK would be excluded from all discussions (and voting) regarding the relationship between UK and EU; and iii) The European Council will negotiate with the UK on tariffs/quotas/free movement etc.

*Albeit there’s some dispute over the issue of unanimity.

There’s an outside chance of a renegotiation of terms despite comments to the contrary in recent weeks by both Leave and Remain campaigns. Jean-Claude Juncker also made similar comments earlier this week (warning that ‘out is out’ and that the UK won’t be able to negotiate a better/different deal than the one already agreed by Cameron earlier this year).

Policy & Central Banks action: Draghi has said that the ECB stands ready to take immediate action in a Brexit outcome. He said there are extensive consultations of all central banks in the world and the IMF (albeit, at this stage, there are no plans and no commitments). Last weekend German Finance Minister Wolfgang Schaeuble said EU policy makers have safeguards in place to avoid “chaotic developments” (without elaborating). There has been a growing expectation that the BoE will loosen monetary policy (despite GB£ weakness/ and the prospect of higher/imported inflation). There’s also a reasonably high likelihood of global coordinated central bank stimulus in the near term.

Points of uncertainty:

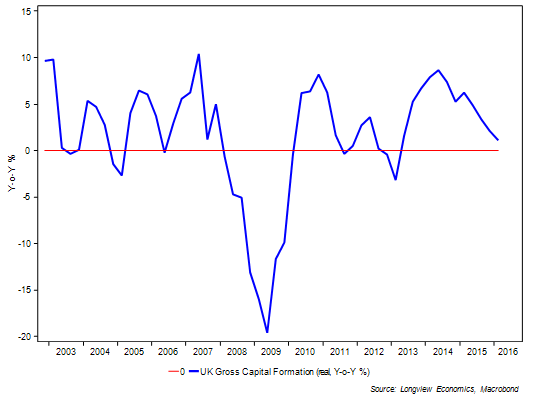

The UK economy: There’s potential for uncertainty to dampen consumer & business confidence (and to delay business/capex decisions). There has already been some softening of confidence and investment spending data in recent months/quarters (e.g. see FIG 3). Given that there’s likely to be increased stimulus from central banks with no change in the UK’s EU relationship for two years, we expect the downside in the economy to be less significant than the widely touted central bank case of Treasury/OECD/IMF and so on. Growth may just stagnate near term.

Scotland: All 32 of the ‘voting areas’ in Scotland voted in favour of ‘Remain’ and Nicola Sturgeon has said that the vote “makes clear that the people of Scotland see their future as part of the European Union.” Another referendum on Scotland’s membership of the UK is now likely.

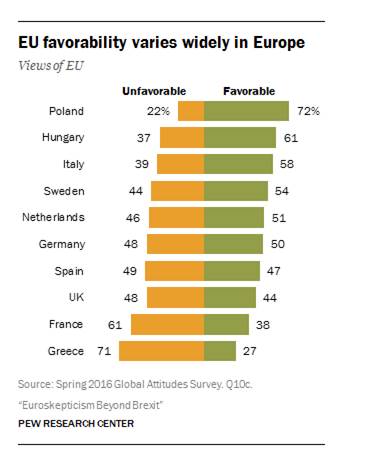

Europe – possible EU fragmentation & break up risk: Results of a recent YouGov poll suggest that, if the UK leaves the EU, there are high expectations that other EU members will follow. Those expectations are strongest in Sweden & Denmark – (suggesting that they are front runners for countries most likely to follow the UK). Polls also suggest that Norway, while it isn’t part of the EU, is likely to try to revisit/review its deal with the EU. Pew centre polls also highlight that both the French and Greek populations view the EU as more unfavourable (than the UK population do) – see FIG 2 below.

Initial market thoughts:

Our medium term market models are mostly neutral and mid-range (as laid out in this week’s Longview Alert No.39, 22nd June 2016: "Move Temporarily & Tactically FLAT; a.k.a. Risk Reward favours NEUTRAL positioning (ahead of possible BREXIT)". With current downside momentum in markets – those indicators are likely to move sharply lower (i.e. towards BUY levels). The risk reward though favours watching and waiting for central bank policy response/stimulus and BUY/strong BUY signals from the models before looking to move OW equities (in tactical portfolios). We remain defensively positioned in strategic portfolios (for detail see Quarterly Global Asset Allocation No. 26, 21st June '16: “Remain Strategically Defensive”).

FIG 1: US$ per GB£ (shown with 200 day moving average)

FIG 2: EU member state sentiment towards the EU (PEW Research)

FIG 3: UK investment spending (Y-o-Y %)

Longview Economics blog: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation advice; and Global thematic, macro and commodities research.

2 topics

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Comments

Comments

Sign In or Join Free to comment