Building a portfolio for the long term

Robert Swift

TAMIM Asset Management

This week we look at the always important topic of portfolio construction. Achieving an optimally balanced and diverse portfolio is more important than ever when heading into increasingly uncertain times and certainly, we would argue, a wiser move than exiting the market completely.

Not a day goes by without picking up the newspaper, only to find dire predictions of the world moving inextricably towards some sort of financial apocalypse. Whether it be a trade war or, closer to home, the property bubble coming to its inevitable end. We will go out on a limb and suggest that much of this has some basis in reality but with the caveat that very similar predictions had some basis in 2012 as in 2016 and every year since time began. If your time horizon is infinite then at least some of these predictions are going to come to fruition. Let us make one thing clear, we’re not saying that investors should live in a vacuum and completely ignore their surroundings, far from it and to misquote Alan Abelson:

“Do you know what investing for the long run but listening to market news everyday is like? It's like a man walking up a big hill with a yo-yo and keeping his eyes fixed on the yo-yo instead of the hill.”

We would suggest that far more money has been lost by investors trying to time the market than has been by investors during recessions. Yes, we are in the late-cycle stage of a global economic expansion and yes, we accept the premise that there are several issues in Australia ranging from excessive household/private debt to policy uncertainty. Governments and individuals alike globally have taken Oscar Wilde to heart when he suggested that anyone ‘who lives within their means suffers from a lack of imagination.’ It is perhaps more important as investors to think about what this means for our portfolios and to continue with our time-tested investment processes while allocating in a pragmatic manner.

No Systematic Bias (or at least question assumptions)

We’re all familiar with the notion that ‘everything is correlated in a downmarket.’ And although there is no magic formula when it comes to diversification, we can assume from experience that on a whole portfolio basis, most people would (unintentionally) have a bias towards a bull or bear market. This is best illustrated by the abundance of passive strategies geared towards either growth or having a sectoral basis.

For example, how many people question the implicit assumption made on the USD by being long on the so-called high growth tech stocks who derive the majority of their revenues globally (i.e. hence a short USD trade). In a similar vein, we question whether investors have thought through the notion of owning an investment property while also buying bank shares thereby doubling up on their residential property exposure.

Industry or Geography

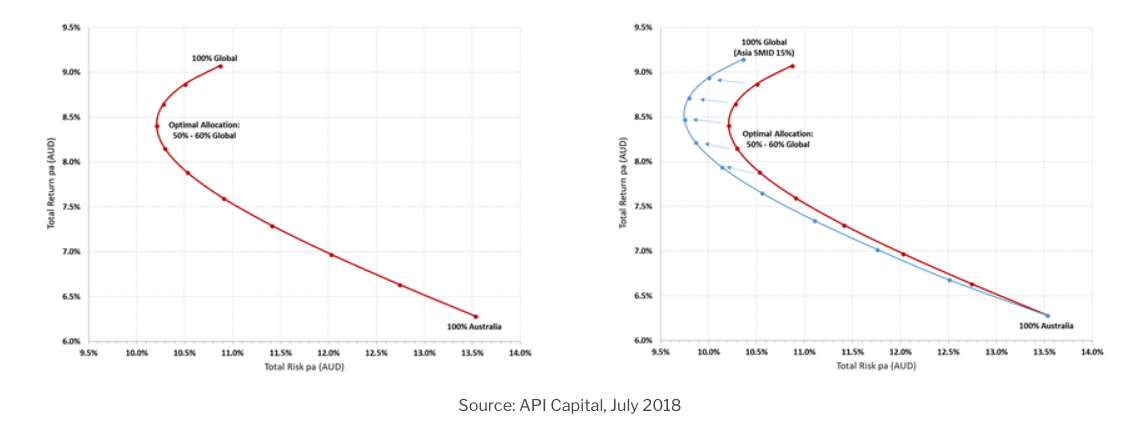

Diversification strategies when it comes to sector vs. geography is a contentious topic because, as with so many other topics when it comes to portfolio theory, the answer is not very clear cut. While early studies (for the geeks amongst you) showed that geographic or more specifically country factor diversification clearly enhanced returns over the long run, more recently this argument does not seem to be holding water. On an intuitive level, geographic diversification makes sense given we might have the ability to achieve greater returns via exposure to country specific factors such as local monetary and fiscal policies. We’ve previously alluded to the necessity of having global exposure in order to optimise portfolio’s from a risk vs. return perspective (below is a favourite graph of our Head of Global Equities, Robert Swift showcasing an optimal allocation or 'efficient frontier').

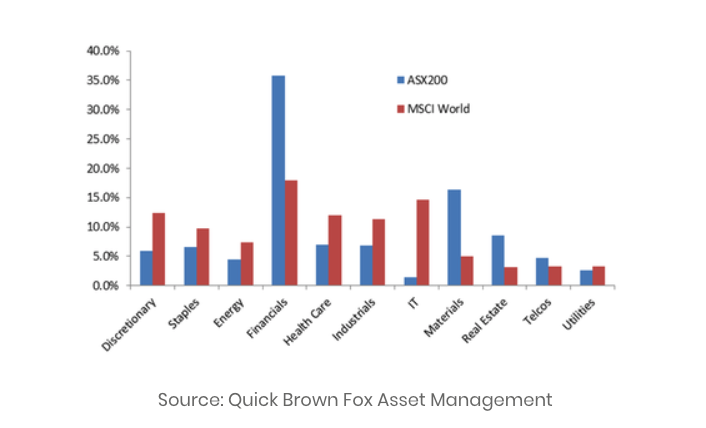

However, there is a caveat. Much of this might not be a result of macro-factors but the composition of the equity markets in individual countries. For example, being invested in Australia is the equivalent of making a disproportionate bet on certain sectors (e.g. banking or basic resources as can be seen in the chart to the below). In fact, a recent working paper by the ECB showcased a negligible difference between the two strategies unless you account for portfolio constraints (i.e. active management).

Another particular consideration to account for is the increasingly interconnected nature of capital markets. Markets are dynamic and while geographic diversification might have been a valid strategy in the past, recent trends have meant there has to be a more nuanced approach. That is why industry diversification is more relevant when it comes to developed markets, while in emerging markets the opposite is true. This is because of the increasing industrial alignment within broader developed markets versus the less developed emerging markets. In order to minimise correlation, you would need the opposite to be the case.

Be more discerning

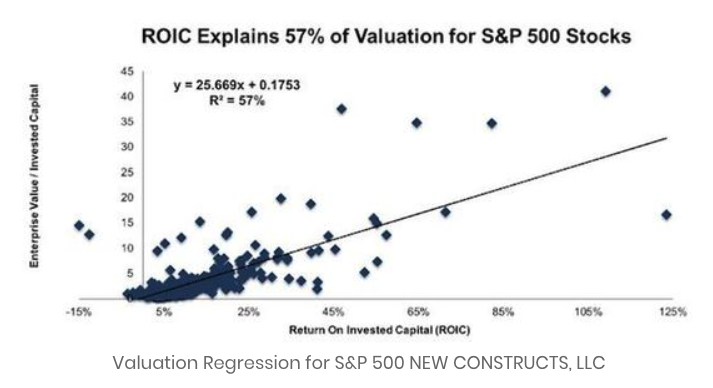

One of the biggest red-herrings we constantly hear is the notion of defensives. While it is undoubtedly the case that certain sectors in the economy exhibit cyclical tendencies more so than others, it is also true that in the event of a major downturn everything tends to be at least somewhat correlated. A better metric we would suggest for the long term investor is ROIC (return on invested capital). It is not a coincidence that the companies that tended to outperform and have positive returns during the 08-09 period were in fact those that were disciplined in their approach to capital expenditure.

All of the other common metrics used by value investors (ROE and EBIDTA etc.), and we are not saying these shouldn’t also factor in, show a weaker link to valuation than ROIC. Using just intuition its easy to understand this concept. It also follows that investors should be weary about the flurry of M&A activity and share buybacks that tend to take place especially in an expanding economy.

Absolute Return

While we do not subscribe to the belief that only one investment strategy works but rather that most strategies have validity just in differing market environments. It might therefore be strange to hear us advocate an absolute return strategy, however from an individual portfolio standpoint this should be the primary goal of all investors. With a long term view, we tend to agree with the notion that a benchmark is the only legitimate way to assess the calibre of a manager (taking downside risk management into consideration) it is unfortunately also the case that we cannot spend relative money.

It therefore makes sense than to have some parts of your portfolio set aside across asset classes that are able to provide a positive return irrespective of how equity markets behave. One would have to actively think and be prepared to ask tough questions around whether there are significant correlations. For example, an oft overlooked fact is that bonds and credit assets can have a latent beta which essentially means that they behave independently from equities when asset prices are rising and turn very quickly when equities are falling. Actively thinking about how to chop and change the underlying debt exposures is key within the current context. A similar case can be made for property, which despite the cynicism currently surrounding the market does present opportunities from a yield perspective.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Robert is the head of Global Equity Strategies at TAMIM Asset Management and is also the manager of the TAMIM Global Equity High Conviction IMA. Robert has worked as a fund manager in the investment industry for over 30 years. Before API & TAMIM he managed $20bn as head of multi strategies at BTIM in Sydney and prior to that was jointly responsible for over $200bn while a Chief Investment Officer at Putnam Investments in Boston, USA. He recently joined the investment committee at Local Government Super, an $8bn industry superannuation fund, based in Australia.

Robert Swift

Head of Global Equity Strategies

TAMIM Asset Management

Robert is the head of Global Equity Strategies at TAMIM Asset Management and is also the manager of the TAMIM Global Equity High Conviction IMA. Robert has worked as a fund manager in the investment industry for over 30 years. Before API & TAMIM...

Expertise

Robert Swift

Head of Global Equity Strategies

TAMIM Asset Management

Robert is the head of Global Equity Strategies at TAMIM Asset Management and is also the manager of the TAMIM Global Equity High Conviction IMA. Robert has worked as a fund manager in the investment industry for over 30 years. Before API & TAMIM...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions