Buy Hold Sell: 3 top-rated and 2 overlooked value stocks

The rotation from growth into value is well upon us with many beaten down stocks now finding favour in the market. As the country returns to a semblance of normality, brokers are upgrading their outlook on these stocks and investors are following.

To discuss these stocks, Matthew Kidman is joined by Steve Johnson of Forager Funds and Ben Rundle from NAOS Asset Management. The trio consider companies including, 1) Westpac - who has had a tough year in the headlines but is now backed by 6 of the largest brokers to outperform 2) Woodside - the oil giant up 30% in the last month and 3) Vicinity Centres - a shopping centre exposed REIT that could benefit as the country reopens (Broker ratings can be found below, data provided by FN Arena).

Additionally, each fundie brings their best pick for an overlooked 'value' stock.

Notes: Watch, read or listen to the discussion below. This episode was filmed on 2 December 2020

Edited Transcript

Matthew Kidman: Welcome to Buy Hold Sell brought to you by Livewire Markets. My name's Matthew Kidman, and we're going to talk value. In the last few weeks you know what's happened. Value stocks, they've stuck their head up again. Can it last? Is there value out there? And to talk about it are some of the best value investors in the land, Steve Johnson from Forager and Ben Rundle from NAOS. Ben, we'll start with you. Westpac. The banks have taken off. Westpac's been the ugly duckling in the banks. Can they keep going?

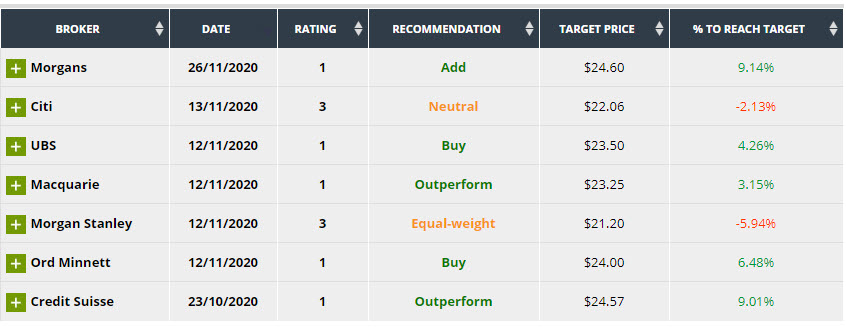

Westpac (ASX:WBC)

Westpac consensus (6 Buys, 1 Hold)

Ben Rundle (Buy): I think so. I think Westpac's a buy. I think the landscape for the banks has significantly changed in the last few months. So if you look at kind of the last couple of years, the regulator and the government's just been one way against the banks, whereas that seems to have changed. So the dividend capping, apart from APRA, is potentially going to get taken away. Stamp duty in New South Wales potentially removed, which I think is good for credit growth. Responsible lending laws have been removed, economic growth starting to pick up, and the banks are starting to get some financial support from the RBA, too. So I think the landscape's changed and Westpac's a buy.

Matthew Kidman: Steve, it's been easy to outperform the market, underweight banks. Guess what happened last month? It was a barnstormer. Buy, hold, or sell Westpac?

Steve Johnson (Hold): Exactly right, and it's been 10 years of struggle for banks, not just here in Australia, but globally. I'm a really big bull on the big banking franchises around the world. I think they're so deeply unloved, and I think, like you've got here in Australia, with a lot of countries you've got a pretty attractive oligopoly in the space and people are underestimating how much their problems are going to get passed onto the customers. Okay, interest rates are down, it's hard to earn your net interest margin, but we're an oligopoly. We're going to pass that onto the customers eventually. I think you will see that. We still have the most expensive banks in the world, though, and I would say hold because of that. I think there are better opportunities. For people just investing on the ASX, Virgin UK listed here, I think, is better value than the Aussie banks. And we own Lloyd's listed in the UK, which is, I think a similar quality to what you've got here, trading at half the price.

Woodside Petroleum (ASX:WPL)

Woodside Petroleum (6 Buys, 2 Holds)

Matthew Kidman: Okay. Let's get onto gas. Woodside. Angus Taylor thinks gas is part of solving the issue. Others think it's part of the problem. Down and out, Woodside, buy, hold, or sell?

Steve Johnson (Buy): It's a buy for me. I think there's just so much pessimism about the space. It's a pretty high quality business in regards to the sector that it's in. And I think you're more likely than not to see a bit of upward pressure on prices over the next five years, given the lack of investment. It's not taking away from the longterm issues that the industry faces, but you've got a lot of pessimism factored in today.

Matthew Kidman: It's really been knocked about, but surely these fossil fuel-related businesses are dead, aren't they, Ben? Buy, hold, or sell?

Ben Rundle (Buy): Look, I think Woodside's a buy as well. Interestingly, their production rates at the moment are around what they guided to about two or three years ago, so they've clearly got very good visibility in the business. And to your point on fossil fuels, I think the gas side of the business, I think that's not a bad alternative to power some of these growing economies. So it's a buy for me.

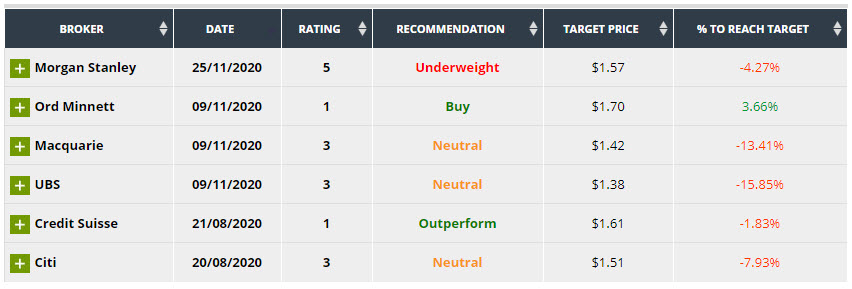

Vicinty Centres (ASX:VCX)

Vicinity (2 Buys, 3 Holds, 1 Underperform)

Matthew Kidman: Okay, shopping centres. I thought they were in decline forever. And all of a sudden, now that we've got a vaccine on the way, everyone's hanging out in the shopping centre. Vicinity. Buy, hold, or sell?

Ben Rundle (Buy): Yeah, it looked that way. I think Vicinity is a buy. They recently said that traffic in their centres ex Melbourne is almost back to pre-COVID levels. Retail sales are picking up. I don't think that re-leasing spreads will be positive just yet, but I don't think they’ll be quite as bad as what everyone thought. So the balance sheet's been fixed. I think Vicinity is a buy.

Matthew Kidman: You'll be hanging out at the shopping centre, the shaver shop, trim your beard there. Buy, hold, or sell Vicinity?

Steve Johnson (Hold): I'll say hold on this one. If you're going to own shopping centres, you need to own the destination shopping centres. And I mean, the big high-class ones that people want to go and visit because it's fun, I think they're going to be completely fine. Outside that, I think you're going to really, really struggle. They've been jamming up the rents for years. The percentage of company sales that have been going out to the landlords has gone from 6% and 7%, 20 years ago, to 15% today. And I think they're going to keep sending their customers broke if they keep doing that. So irrespective of everything that's happened in COVID here, I think it needed to reset. And I think COVID has been a reset for that trend of rapidly rising rents forever. But if you own the good ones, you're going to be fine.

AMA Group Ltd (ASX:AMA)

Matthew Kidman: Okay. Delve into your value bag. What's one stock that represents really good value at the moment?

Steve Johnson (Buy): Yeah, I'm pitching AMA today, which is a smash repairs roll-up. I'm normally a sceptic about the roll-ups and this company did a big acquisition about 12 months ago that hasn't worked as well as hoped. The share price did a big cap raising at a $1.40 to fund it. Share price went down to 20 cents in March. It's back at 70-something today. But I think the long-term story here is still a very good one about a corporate that has lower costs and lower ability to negotiate with its suppliers. Buying up mum-and-dad operators around the place and adding to its earnings by doing that. And I think you're going to see that story come back to the forefront for investors over the next few years.

Over The Wire (ASX:OTW)

Matthew Kidman: Ben, you got something that can match a good ding in the side of the car?

Ben Rundle (Buy): Yeah, I like Over The Wire. OTW is the code. They recently made a couple of acquisitions. So Over The Wire is a business which helps small and medium size enterprise with their internet, their telephony and their cybersecurity. There's been a huge amount of small cybersecurity companies on the market at the moment, which have rolled up a few others and are trading on huge numbers with no earnings. Over The Wire actually has earnings. They have made two acquisitions recently. One came with about 9,000 customers. Then that's on the top of Over The Wire's 5,000 customers. So I think if Over The Wire can cross-sell some of those, then you start to see organic growth in the business significantly pick up. They also acquired a data cloud business, which I think probably improves the overall earnings base for Over The Wire. Both of those businesses have come at higher margin. And if you put them all together, I think that the earnings power of that business is a lot higher than what people are expecting and management are significantly aligned with shareholders, so Over The Wire. My pick.

Matthew Kidman: We've been waiting for some value for a long time, and now it's time to pick up the phone and dial some in.

Enjoying Buy Hold Sell?

- Hit ‘follow’ below to get notifications of when we publish Buy Hold Sell

- Stay tuned for Monday (7/12), when Steve and Ben discuss 5 of the most traded stocks

- View the full Buy Hold Sell archive here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Buy Hold Sell is a weekly video series exclusive to Livewire. In each episode two fund managers give their views 'Buy, Hold or Sell' on five ASX listed companies. Not recommendations, please read the disclaimer and seek advice where appropriate.

3 topics

5 stocks mentioned

3 contributors mentioned

Livewire Markets

Buy Hold Sell is a weekly video series exclusive to Livewire. In each episode two fund managers give their views 'Buy, Hold or Sell' on five ASX listed companies. Not recommendations, please read the disclaimer and seek advice where appropriate.

Expertise

Livewire Markets

Buy Hold Sell is a weekly video series exclusive to Livewire. In each episode two fund managers give their views 'Buy, Hold or Sell' on five ASX listed companies. Not recommendations, please read the disclaimer and seek advice where appropriate.

Expertise

Comments

Comments

Sign In or Join Free to comment