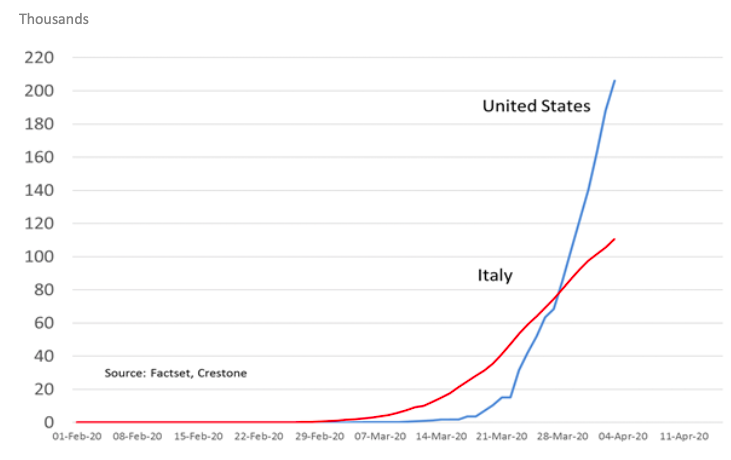

Chart of the day: accelerating spread of COVID-19 in the US

“If isolation is the furnace of transformation, I could be ashes by now.” ― Stephen Christian, The Orphaned Anything's: Memoir of a Lesser Known.

US equity markets fell (relatively) sharply overnight, with the S&P 500 index giving back 4.4% of its 15.8% rally from its 23 March low. It’s still up around 10%, though still down around 27% from its pre-COVID-19 high. But it wasn’t the data causing the fall, at least, not the published data. The US’s key manufacturing ISM beat estimates for March, easing only from 50.1 to 49.1 (versus consensus for 46.0) - virtual noise - and likely reflecting both the momentum of the US economy as it entered 2020 and arguably the US’s slow response in appropriately responding to the virus’ spread until late in March.

The market would appear more focused on the data behind our chart today, namely the accelerating spread of COVID-19 across the US, which has now taken over from Italy (which took over from China) as the disease’s epicentre. As the chart reveals, there is little sign of containment in the US, and experts suggest ‘peak spread’ – and the flattening out of cases (such as in China, South Korea and now Italy) that periodically calmed markets’ nerves – remains a couple of weeks away. It is not the macro data today that is weighing on markets, but the macro data ahead. Consensus for Friday’s March US payrolls has been steadily trending from -60,000 last week to around -200,000 currently. However, April holds the prospect of more than 1 million lost payrolls.

At Crestone, we continue to monitor key signals to guide us closer to when markets may trough. Over the past couple of weeks, a number of these have been ticked off—namely policy stimulus, while we have made progress on valuation, a re-tightening of credit spreads and weak data. However, at this stage, we are yet to achieve ‘peak disease’, which appears the most critical for markets (to the extent it impacts whether the outlook is a U-, V- or L-shaped recovery).

US versus Italy—Daily COVID-19 cases

Source: Factset, Crestone.

Be the first to know

I’ll be sharing Crestone Wealth Management's views as new developments unfold. Click the ‘FOLLOW’ button below to be the first to hear from us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

1 topic

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment