Chart of the day: Could FX volatility be much lower from here?

“When an investor focuses on short-term investments, he or she is observing the variability of the portfolio, not the returns – in short, being fooled by randomness." Nassim Nicholas Taleb (American statistician, options trader)

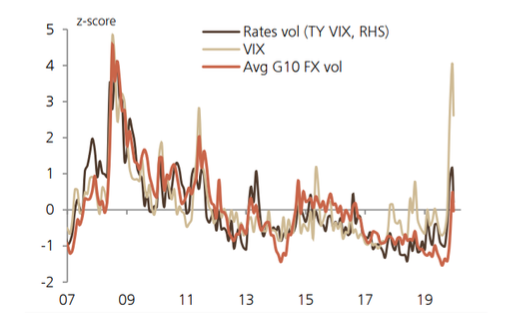

Our chart today from UBS shows volatility compared across fixed income (rates), equities (VIX) and currencies (G10FX). What’s interesting here is that since before the GFC (and I suspect throughout history), currency (FX) volatility has for most of the time exceeded the volatility of equity markets and bond yields. However, more recently, the volatility of FX has been much lower. Indeed, compare the current COVID-19 crisis with the GFC in 2008-09.

So, what’s going on? As UBS posits, “monetary policy has arrived at its endpoint”. All the major global central banks have cut rates to zero (or their effective lower bound very near to zero) and engaged in quantitative easing in “a highly synchronised fashion” over the past couple of months. This has led to a few consequences. Firstly, central banks for now are no longer equipped to be the ‘first responders’ to future demand shocks (…indeed the equity market’s post GFC ‘put’ is now a bit more of a ‘putt’). Secondly, unless we are expecting a sudden rebirth of inflation, central bank rates are going to be around zero for quite a while, even as demand likely rebounds in H2 2020 and 2021. As such, it’s unlikely we are going to see FX markets driven by cross-country divergences in rates policies…everyone’s at zero! If we are looking for dispersion, it’s now going to be found in fiscal policy, which likely now holds the future dominant policy role. However, this may well be much more difficult for FX markets to grasp than more visible interest rate differences.

The bottom line is that, with interest rates globally and in Australia at zero, it’s possible that FX volatility will be much lower, and UBS suggests more in line with equity volatility. The latter point still leaves the Australian dollar vulnerable to any near-term equity market drawdown, if equity markets suddenly decide that, despite progress in containing the pandemic, that the damage to the economic outlook justifies a valuation discount to the market’s pre-COVID-19 highs! However, it may also mean the Australian dollar is less volatile ahead, and “FX markets should revert to more trending and less mean reverting [volatile] behaviour” until there is more dispersion in global central bank policy rates. Arguably, the cost of hedging should go down if this is true. But let’s not hold our breath!

Finally, using a scoring tool that considers leading activity indicators, real rates, terms of trade, current accounts and valuation, UBS lists the Australian dollar as the second most bullish currency in the G10 from here. UBS is forecasting the Australian dollar at USD 0.69 at the end of 2020 and USD 0.71 at the end of 2021. From today’s USD 0.6480, that’s a rise of 6.5% and 9.6% respectively.

Volatility across fixed income, equities and currencies

Source: Haver, UBS.

Be the first to know

I’ll be sharing Crestone Wealth Management's views as new developments unfold. Click the ‘FOLLOW’ button below to be the first to hear from us

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment