Chart of the day: Oil over-supply in 2020

“That which cannot go on forever, won’t” - Herbert Stein, American economist, 1916-1999

Volatility in equity markets has eased modestly over the past week or so as US markets have risen four out of the past five days. The gain has been around 17% (compared with the S&P/ASX 200 index, which is up about 14% before today). Of course, both markets remain more than 20% off their highs (the iniquity of rising from a level more than 30% off its peak). Is it possible the extent of global stimulus is providing a more positive backdrop? In Australia, the Morrison-led government’s AUD 130 billion wage subsidy deal, its third stimulus, drove the equity market up 7% yesterday. Or maybe the selective examination of COVID-19 country trends holds some positive vibes? It certainly hasn’t been better-than-expected data driving the recent moves, with most leading indicators foretelling of imminent recession and rising unemployment globally.

Another one of our signals that isn’t yet gesturing a trough in markets is the oil price, with oil futures dropping 6.6% to $20.09 a barrel on Monday, a level last seen in February 2002. The key driver was concern that quarantine measures are knee-capping global demand. As we well remember, this really began back in early March when Russia and Saudi Arabia couldn’t agree on limiting production and, rather than agreeing to disagree, decided to try and cripple each other (and the US shale industry) by boosting production instead.

Of course, as we highlighted several weeks ago, oil at $20 a barrel appears unlikely to be a general equilibrium solution. While Saudi Arabia is believed to be able to pump oil at $10 a barrel, Russia’s cost of production is between mid-$20s to low $40s. And Russia’s fiscal break-even is $40 to $50, while Saudi Arabia’s is estimated to be over $80 by the International Monetary Fund. This, of course, begs for a new agreement by these protagonists to limit production/supply. The only problem is demand is also falling sharply at the same time.

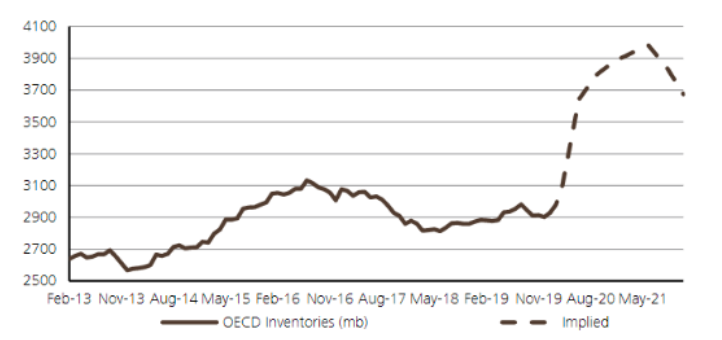

This brings us to today’s chart by UBS showing a forecast sharp rise in inventories through mid-2020 into mid-2021. According to UBS, a decline in oil demand in 2020 and the market share war is “driving an estimated over-supply of almost unprecedented levels in mid-2020”. A downturn in US shale activity, with capex cuts of 20% to 30% announced, likely helps supports oil demand in H2 2020. UBS continues to expect long-term oil prices to remain tethered to the $60 to $80 per barrel range—but now sees the lower end of this range being sustained until at least the end of 2025.

Crude inventories (mm barrels)

Source: IEA, UBSe

Be the first to know

I’ll be sharing Crestone Wealth Management's views as new developments unfold. Click the ‘FOLLOW’ button below to be the first to hear from us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

2 topics

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment