China, what just happened?

Charlie Aitken

Aitken Investment Management

Substantial outflows from emerging markets ETFs, driven by US Dollar strength, triggered large and relentless selling in the largest index weightings in Hong Kong (Chinese equities). Fears of a “trade war” have also weighed on China sentiment.

The Hang Seng China Enterprises Index (HSCEI) fell -7.6% in June, while the Chinese mainland benchmark, the Shanghai Composite Index (SHCOMP) fell -8.0%. From mid-January peak both indices are now down over -20%, triggering a technical “bear market”.

It has been a brutal and indiscriminate technical sell-off in Hong Kong. However, we remain confident in the investment case for Chinese consumer facing companies and the major technology platforms which have pulled back to what we consider compelling investment arithmetic. We will explore that investment arithmetic later in this note.

While Chinese stocks listed in China had a very poor month, it seems somewhat odd to us that China facing stocks listed on developed market exchanges such as the NYSE or ASX proved broadly immune to any price falls. That most likely suggests this is a violent emerging market to developed market rotation, rather than a wholesale de-rating of all things China facing.

We believe this is a technical ‘clearance sale’ in leading Chinese equities and we want to emerge from this rotational correction holding the very best fundamental portfolio of tier one Chinese structural companies we can.

Outflows from Emerging Market equities

The US dollar rally that began in May has seen significant outflows from Emerging Market equities. We can use the IShares MSCI Emerging Market ETF (“EEM.US”) as a good proxy to illustrate this point. EEM has seen a 20% redemption of units on issue since April (approx. $7.7bn of outflows at today’s prices). China is the biggest weighting in this ETF at 30% and Tencent is the biggest single stock weighting at around 5.5%, so redemptions from this ETF and all other products like it lead to direct selling of Tencent and other large cap Hong Kong Listed equities.

The following chart shows the number of units outstanding in EEM (the blue line) versus the DXY USD Dollar index (the red line) which we have inverted. In simple terms USD strength has seen an exodus from Emerging Market equities. For context the outflow in EEM over the past 8 weeks is greater than the outflow for the entire of 2015 when the world was in a China-centric deflationary spiral.

In 2015 evidence of a fundamental slow-down in China was obvious everywhere from Chinese economic data, to global PMIs, trade data, commodity prices and even Australian listed China facing equities. The most obvious example is BHP shares which have historically had a very strong correlation to H-Shares. The chart below shows the HSCEI Index (H-shares) versus BHP. One of these 2 is sending us the wrong message on Chinese economic fundamentals. The gap in this chart will close one way or another in the second half of this year. Note the divergence started around the same time as the EM exodus (BHP is not part of EM equities).

Is China grinding to a halt?

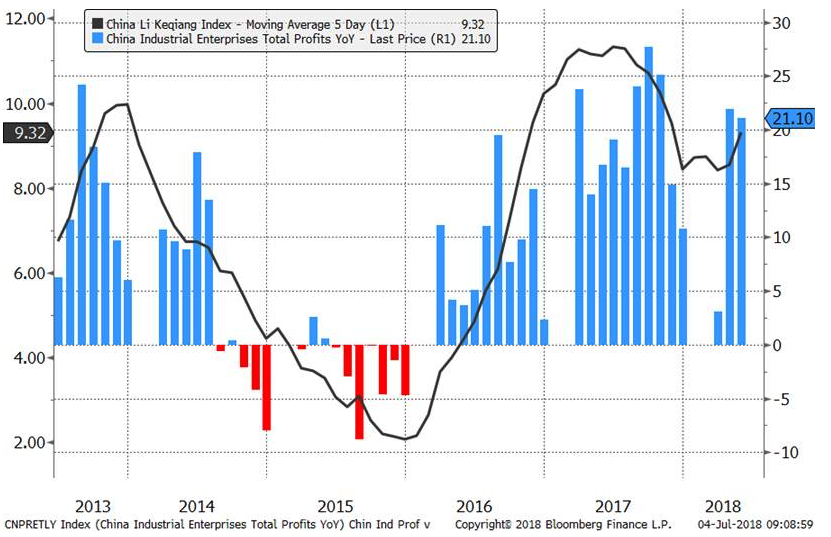

Relative to the strong-growth seen in 2017 we are definitely seeing a moderation of growth in China. This was evident in our recent trip to China and can been seen in monthly data series such as the YoY change in Industrial Enterprise Profits and the Li Keqiang index (which measures YoY change in rail freight data, power consumption and bank lending). However as can be seen below the picture at this stage is fundamentally different to what we saw in 2015. The key question is, are HK equities pre-empting a move in fundamentals or is this a market driven panic?

What are markets pricing in?

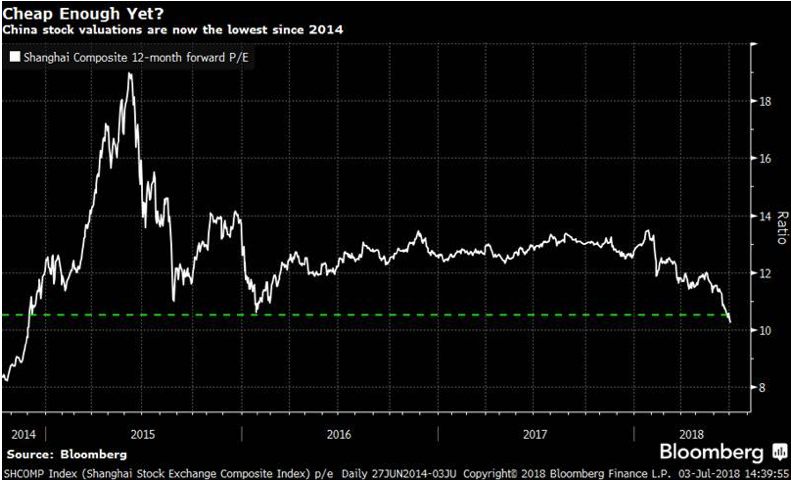

Whilst the 2015 bear market in Chinese equities saw a combination of very high starting valuations and badly deteriorating economic fundamentals the picture today is quite different. The market PE for domestic Chinese equities is already below the trough of 2015.

We see plenty of inconsistencies in global cross asset market prices at the moment. It feels like Hong Kong listed Chinese equities are pricing in a harsh slow-down in global growth whilst other equity markets (and other asset classes such as gold and commodities) are taking a more optimistic view.

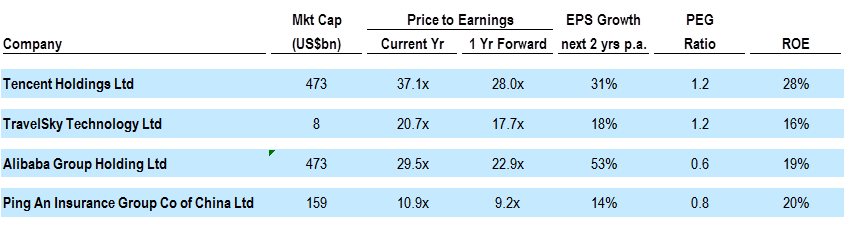

Below we present a snapshot of AIM’s four biggest Chinese holdings.

We believe all these businesses have very bright futures and are very attractively priced at current levels. They are the leaders of their industries, have expanding moats, have massive addressable markets, and are all platform businesses or benefitting from technology. We believe their earnings growth outlook is unchanged, we have recently met with management teams, and we have great confidence in their business strategy and execution abilities.

While it was a disappointing end to the financial year for those of us who are structurally bullish on China, we remain of the view that the potential for strong total returns remains in FY19 particularly given the entry points and highly attractive valuations of our core high conviction Chinese investments above.

Don’t run away from the clearance sale: take advantage and buy the best Chinese consumer brands while they are cheap.

Aitken Investment Management is a Global High Conviction Fund led by Charlie Aitken. For more information please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Charlie Aitken

Aitken Investment Management

Expertise

Charlie Aitken

Aitken Investment Management

Expertise

Comments

Comments

Sign In or Join Free to comment