Collection House Limited (ASX: CLH)

Given the recent negative report published on Credit Corp (ASX: CCP) please find following a note we recently wrote on Collection House (ASX: CLH), their biggest competitor:

Market Price: $1.57

Market Cap: $213m

Business Summary

Collection House Limited is an Australian receivables management company, providing organisations and individuals with solutions in credit management, collections and customer care. Founded in 1994 and listed on the Australian Securities Exchange in 2000, the CLH is made up of a number of brands offering a range of professional, ethical and effective products and services. The company broadly consists of two major segments; Collection Services, and Purchase Debt Ledgers.

CLH has a strong relationship with international banks, financial institutions, large corporations, public utilities, and all levels of Government. CLH is the only publicly-listed end-to-end receivables management company. Across offices in Adelaide, Brisbane, Melbourne, regional Victoria and Sydney - as well as in New Zealand and the Philippines the company employs over 850 staff.

Since inception the company has evolved from being exclusively a traditional debt collection business to become a complete receivables management provider; covering compliance and ethics, corporate governance and processes, and technology and analytics.

1H18 Results

Collection House Limited recently reported 1H18 results in line with expectations and an upgrade to full year guidance. Total revenue for the Group was $63.4 million, a decrease of 4% compared to 31 December 2016. Consolidated net profit after tax (NPAT) was stable at $8.2m for the six months to 31 December and full year estimates have increased to $19.7m - $20.4m (previously expected to be $19m -$19.7m).

Collection Services Segment: Collection Services reported revenue of $33.1 million in 1H18, down 1% on 1H17. Productivity improvements gained through enhanced processes and the introduction of new contact centre technology were offset by some client revenue being deferred, which is now expected to report in the second half.

Purchased Debt Ledger Segment (PLD): The PLD segment reported revenue of $30.3 million, down 6.5% on 1H17. PDL collections were down 3.6% to $50.4m. Management are expecting a turn-around in the 2H18 and beyond on the back of increased investment in productivity and improved analytics. Turning around four previous periods of decline, the Company reported $320 million of active repayment arrangements as at 31 December 2017, up from $317 million at the end of FY17.

ThinkMe Finance – Continued Diversification

ThinkMe finance is a wholly owned subsidiary of CLH and is the company’s first foray into consumer finance. On the 24th of May 2018 CLH announced that ThinkMe had secured a full credit licence from ASIC. Originally a finance broker ThinkMe was an intermediary helping retail customers with loan applications, however, with the new license they will be able to provide loans directly to customers.

ThinkMe is well prepared to succeed in the consumer credit sector, having already established a digital portal for applications due to their existing business, and a successful loan approval process. In addition, CLH will be focused on cross selling ThinkMe loans and finance options to its other businesses that specialise in debt recovery. The ability to provide financing will allow existing CLH customers to refinance their debt and replay defaulted accounts with more manageable repayments with an interest rate far below the legislated caps. Moreover, ThinkMe will allow clients to repair their credit record by recording their on-time payments.

Initially the market had viewed the ASIC financing approval negatively with the stock falling on the day of the update.

Balbec Deal – De-Risking Debt Ledgers

On May 1st 2018 CLH went into a trading halt on the back of a deal with Balbec (a private equity group) in which CLH will offload a portion of debt for $19.5m in cash. This move shows management are committed to taking a more conservative stance on their existing debt legers; they are proposing to reinvest the $19.5m in further debt purchases this calendar year. The market approved of the deal with the shares rising from $1.42 to $1.56 upon reinstatement.

The deal with see CLH transfer the cash flow generated from a $39.5m debt ledger to the U.S. based Balbec over the next 5 years. Additionally, CLH will receive a monthly fee from Balbec for recovering the debt.

CLH has the option to repurchase the residual rights to collect the remaining arrangements at the end of the five-year agreement at a market price determined by the performance of the accounts during the term of the agreement. The transaction is a disposal for accounting purposes and will result in a profit in FY18 of $4.9m after tax, deal costs and other adjustments required as a result of the transaction.

CLH has been utilising this call option program since 2017 and it has been successful with smaller deals so far. Investors have been confused by the strategy and accused management of transforming the business into a broker rather than debt collector – management have denied these claims.

Our View

Over the last few years CLH has had a difficult time, slashing profit guidance throughout FY16 on the back of ‘an unfavourable economic environment’ due primarily to ‘excessively high’ prices of debt. Since 2016 the share price has fallen from a high of $2.49 to its current price of $1.57 (a 36% fall). Strangely, CLH’s closest listed rival, Credit Corp Group Limited, has seen record levels of debt ledger purchases and has been experiencing record level profit growth over the same time period. However, we think CLH has started to turn things around, with the de-risking of their debt leger books and the push for management to cross sell additional products to customers. The success in the strategy has already started to show, with management recently upgrading their expected earnings forecasts for the full year.

A strong underlying thematic in which we are looking to gain exposure is the rising interest rate environment. In the current low interest rate environment we have seen Australians take on high levels of household debt; the ratio of household debt to disposable income was recorded at 188.6% in April this year – a 4.4% growth over 12 months. The RBA’s reluctance to raise interest rates (due to high levels of mortgage debt and the risk of a collapse in the housing market) will only create more issues moving forward. CLH positively exposed to a growth in the debt recovery sector and is a great way to take advantage of high debt levels and the potential of an interest rate hike.

Numbers

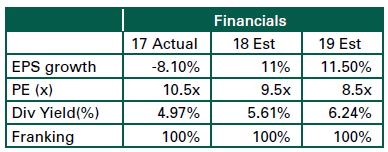

CLH looks strong on the numbers with a forward P/E of 8.5X, a PEG of 0.9, return on equity of 11.5% and an EBIT interest cover of 5.6X. Whilst the growth profile looks favourable due to the strong industry tailwinds, the company has strong existing cash flows and pays a conservative dividend fully franked dividend of 5.61% based on a 50% pay-out ratio. Credit Corp (CLH’s closest competitor mentioned above) trades on a P/E of 14.5X and a dividend of 3%.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 topic

2 stocks mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX innovators with massive potential

Livewire Markets