Coronavirus rattles markets: What's next for global growth?

Matt Reynolds

Capital Group

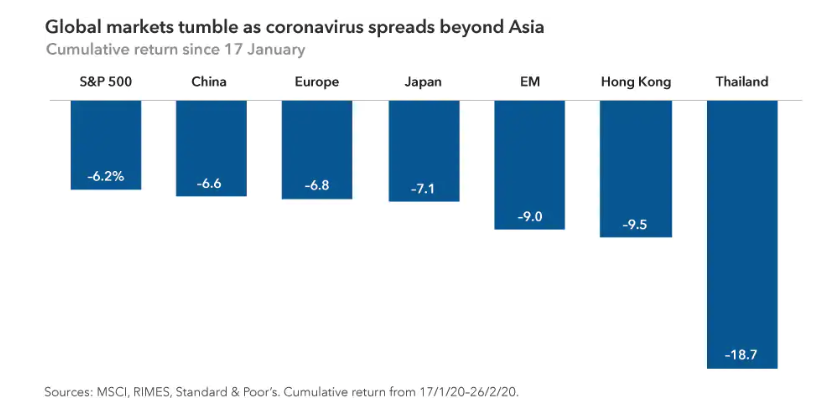

Global stocks fell sharply on Monday following confirmation that the coronavirus has spread to Italy, South Korea and Iran, raising fresh questions about the potential impact on global economic growth and business sector supply chains dependent on China.

After reaching a record high on February 17, the S&P 500 Composite Index has declined by 12%, as of February 27, suffering its first market correction since 2018.

A rising number of infections in Europe, in particular, has prompted markets to re-evaluate concerns about a global pandemic, even though the number of reported cases in mainland China has declined since news reports about the outbreak accelerated around the 17 January.

“Until this week, the consensus market view of the coronavirus has been fairly benign, but now as it spreads beyond Asia, investors are clearly taking it more seriously,” says Capital Group portfolio manager Jody Jonsson. “The market is starting to consider what it means for global trade and travel. The bond market is worried about recessionary conditions in certain areas, including China, Japan and potentially Europe.”

Is supply chain impact fully priced in?

Given China’s stature as the world’s No. 2 economy, one of the most difficult questions that markets are grappling with is the possible impact on global supply chains, and the corresponding effect on multinationals and economic activity in other countries.

For instance, what happens if China cannot send the intermediate products needed in the U.S. or South Korea or Japan to assemble finished goods? Are there enough truck drivers to move products, and do the ports have enough containers available?

“We know for the past month that most people in China have stayed at home and haven’t returned to factories or offices. I believe China’s economy will experience negative growth in the first quarter, and then it’s just a question of how quickly the country can get back to work,” says Stephen Green, a Capital Group economist based in Hong Kong.

“When we’ve pressed our industry contacts about the timing of workers returning to manufacturing plants and offices, we have heard mid-March,” Green adds. “That is the base case. But I believe that hinges on the number of confirmed coronavirus cases in China continuing to come down and people gaining more confidence in those numbers and returning to work.”

Even then, there are logistical challenges.

Factory operators have to get permission from the local government to reopen, and health inspections have to be done. Many cities and industrial zones can require 15 certificates. Is enough material on hand to make the product and are there enough workers to run the plant at full capacity? Once you’ve produced the product, is there a truck driver to get it to the port and are there workers at the port to load the goods on a ship? All of these questions are incredibly hard to solve at this time.

“So, in my view, I don’t think the Chinese economy will normalize until April at the earliest,” says Green.

Apple, which relies heavily on manufacturing plants in China, is the most prominent example yet of the broad ripple effects of the coronavirus on global business. The iPhone maker warned on 17 February that its revenue for the current quarter would fall short of estimates.

Capital Group U.S. economist Jared Franz says that his early research this week shows that computers, electronic equipment and industrial machinery are the three industries most vulnerable to supply chain disruptions from China.

Global investment implications

This poses a potential threat to Europe’s fragile industrial recovery, with Germany the most exposed through trade links. Meanwhile, France and Italy also have significant exposure to China through tourism, services and luxury goods. And Japan, on the brink of another recession, is heavily dependent on China for intermediate goods that go into its manufacturing.

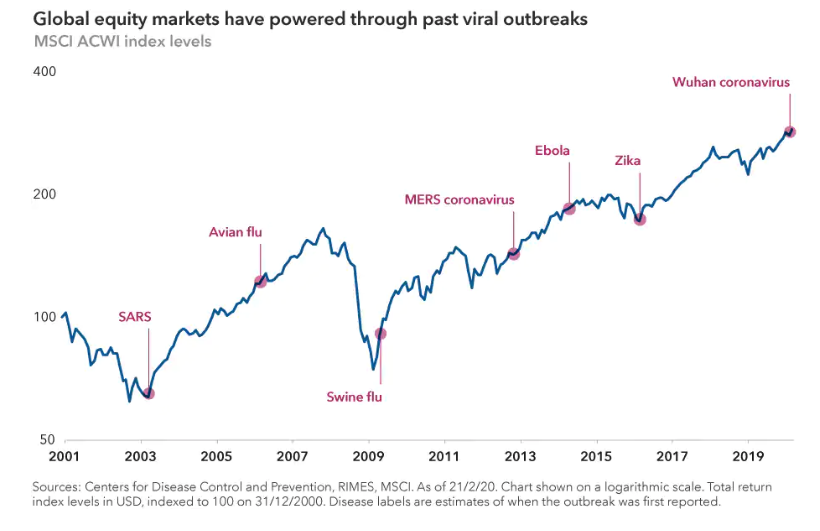

The complexity and timing of this outbreak may make resumption of normal growth more halting and unpredictable. Global supply chains are tighter and more dependent on China than when the SARS outbreak hit the country in 2002 and 2003.

With China now making up almost 20% of global gross domestic product, China’s slowdown from this outbreak will probably have broader impacts than the SARS outbreak.

While the U.S. economy began 2020 in a much stronger position relative to the rest of the world — with very low unemployment, a robust housing market and a confident consumer — it is not immune to China’s slowdown and supply chain problems.

“If the virus spreads further and China’s manufacturing base in not fully functional by April or May at the latest, we could shave half a percentage point from U.S. GDP in the first half of the year,” Franz adds. “And if it lasts longer, the impact could be more severe in the second.”

Leading Chinese officials have said getting the country’s economy up and running again at full strength is a top priority. They have expressed that the coronavirus is a temporary setback to economic growth. So far, stimulus measures from Beijing have included interest rate cuts, more liquidity for small- and medium-sized enterprises and postponement of debt collections.

The virus is taking its toll on business across the world.

Many airlines have cancelled flights to the country. And some companies are lowering earnings guidance for 2020, including some of the world’s biggest cruise line operators and consumer goods makers.

Some companies are opting out of planned conferences as fear of the virus spreads.

“In some ways, the impact is greater on certain companies outside of China — obviously, airlines and cruise companies fall into that category,” says Jonsson. “But it’s also providing a boost to some industries, especially e-commerce and gaming companies. As more people stay home, you’re seeing massive increases in the consumption of home entertainment and online shopping activities.”

This is certainly the case for Chinese technology giant Tencent, which operates one of the world’s largest mobile video game and social media platforms.

Adds Jonsson, “There are a number of industries where I've decided to wait and see how this plays out. For example, when it comes to luxury goods companies or travel-related companies, I think we have time to observe how widespread this situation becomes before making any big decisions in those areas.”

Key takeaways

- China likely to see flat to negative growth with disruption from coronavirus

- The global economy will likely suffer from China’s impact

- Investors should brace for continued market volatility

Position your portfolio to navigate through cycles

Capital Group believes in a smarter way of investing that combines individuality and teamwork into a tailored approach to help investors meet their goals. Find out more, by clicking 'CONTACT' below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The University of Sydney. He also holds the Chartered Financial Analyst designation. Matt is based in Sydney.

2 topics

1 contributor mentioned

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Comments

Comments

Sign In or Join Free to comment