Coronavirus: the investment impact in seven charts

The spread of coronavirus, COVID-19 has created fresh uncertainty for the global growth outlook and sparked volatility in financial markets.

We offer key facts on the spread of the virus, interspersed with views from Schroders economists and fund managers.

What has been the impact so far?

The human impact has been significant, with more than 4250 deaths now confirmed (11 March 2020), the majority in Hubei province in China. This is far greater than the Severe Acute Respiratory Syndrome (SARS) outbreak that killed close to 800 people in 2002-2003.

Chinese authorities have reacted by enforcing quarantines, as well as restricting public gatherings, travel and tourism.

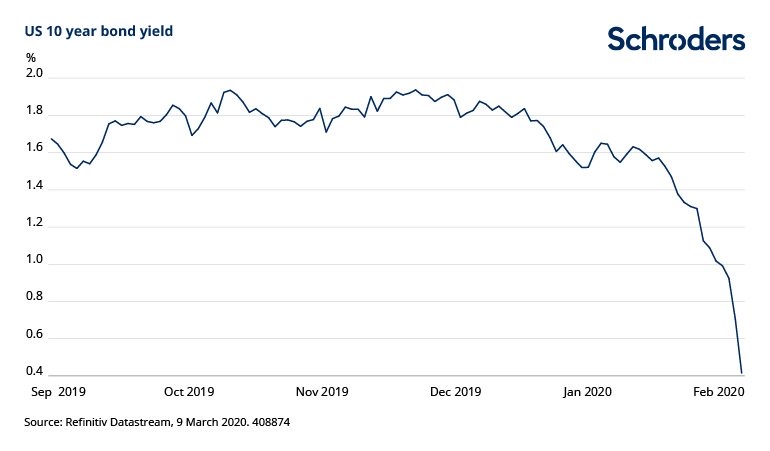

From a financial markets perspective, the response had been fairly muted amid signs that the rate of infection in China had peaked. However, the acceleration of cases in South Korea, Iran and Italy has led to fears that the virus could have a far greater impact than markets were initially anticipating. The charts below show how stock markets have been hit while demand for bonds has risen, which has the effect of pushing down yields and increasing prices.

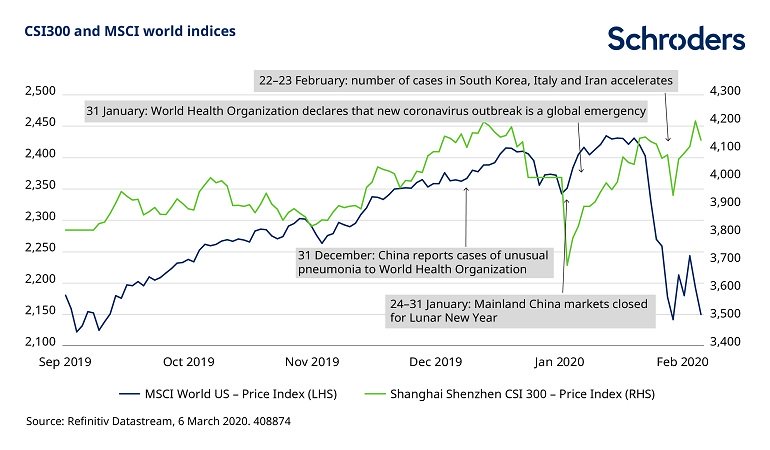

After an initial rebound, global (MSCI World Index) and mainland China markets have seen renewed falls

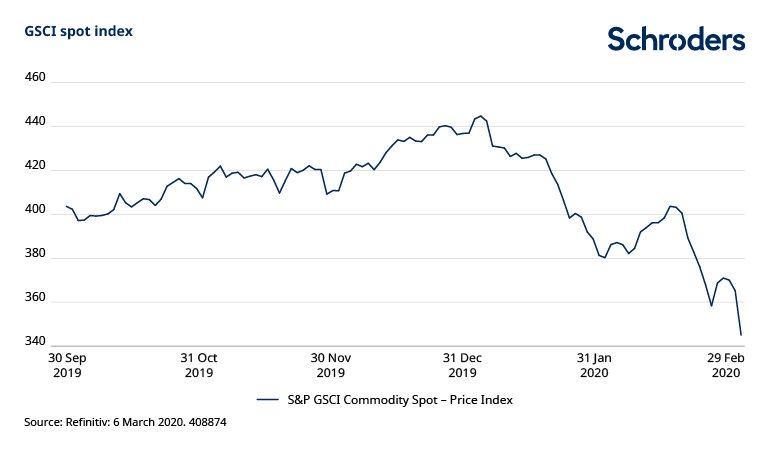

Among other markets, commodity prices have also felt a disproportionate impact. China is the dominant consumer of many raw materials, particularly metals for use in industry. As a result, the impact on prices has been significant, as illustrated by the S&P GSCI, a measure of broad commodity price performance.

This has implications for countries which are commodity exporters. Latin America, in particular, Brazil, Chile, Colombia and Peru have all seen marked volatility in their equity markets and currencies.

Commodity prices fell sharply as the severity of the outbreak escalated

Why is this outbreak different to previous incidences such as SARS?

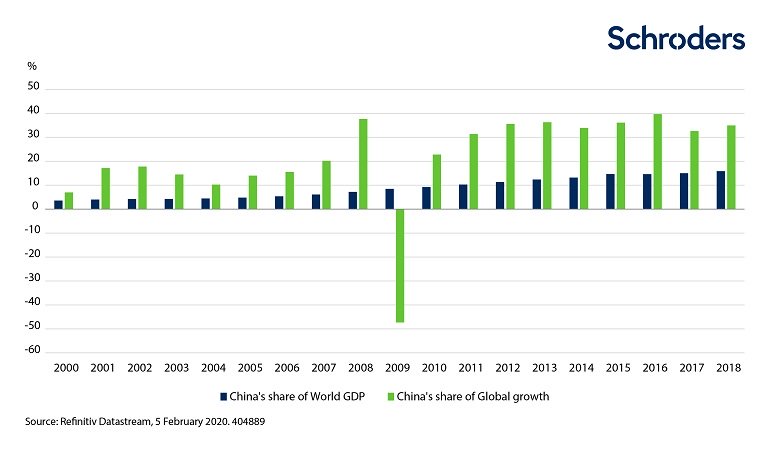

China’s place in the global economy has changed dramatically since the SARS outbreak. China represented 4.2% of the global economy in 2002 and contributed 18% to world GDP growth. By 2018, its share of world GDP had risen to 15.8%, with 35% of global growth coming from China, as highlighted in the chart below.

The impact of weaker economic activity in China will therefore have a proportionately greater impact on overall global growth. After a year in which US-China trade tensions weighed on global growth, market expectations were for an improvement this year. This was predicated on the improvement in trade relations between the two sides over the fourth quarter of 2019, culminating in the signing of the so-called “phase one” trade agreement on 15 January. The coronavirus outbreak has cast significant uncertainty over this outlook.

How China’s share of global GDP and global growth has increased since 2000

What signs are there of health in China’s economy?

The first point to make is that China’s economy has systemic significance. It accounted for 28.4% of global manufacturing output in 2018, according to the UN Statistics Division, compared to 16.6% for the US. In 2004, the US share was 22.3% when China was at just 8.7%. China’s economy has also become more integrated with the rest of the world.

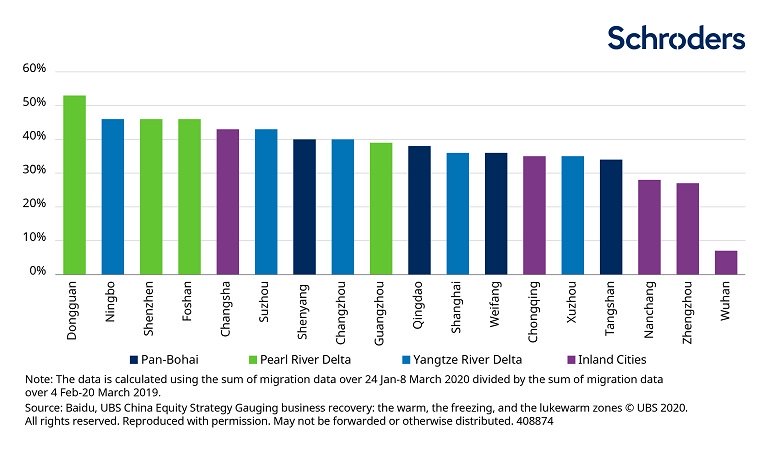

It is hard to precisely gauge the extent to which factories have managed to re-open after the Lunar New Year on 25 January, and at what level of production capacity. Migration data produced by the Chinese tech company Baidu, shown in the chart below, suggests that a large proportion of workers are yet to return. Wuhan, which is where the epidemic is believed to have originated, has seen the fewest workers return. Non-essential business for Hubei, the wider province of which Wuhan is the capital and is home to around 60 million people, remains closed for non-essential business until 11 March.

The percentage of workers returning post the Lunar New Year relative to 2019

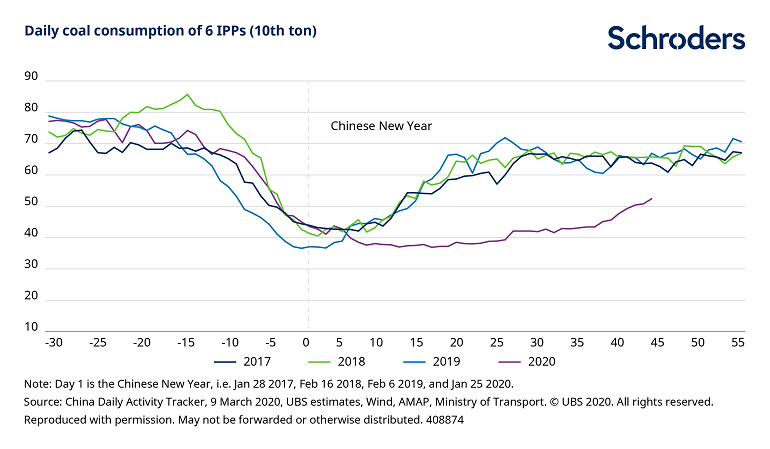

A quick review of coal consumption at six independent power plants, shown in the chart below, underlines the drop-off in activity. Coal consumption is seasonally lower around the Lunar New Year, but usually begins to recover within 15 days.

Coal consumption of six independent power plants after the Lunar New Year

President Xi has now urged people to return to work, but indicated that this should be subject to regional health risks. Quarantine measures and restrictions on movement will likely continue for a number of regions, presenting further logistical challenges to exporters. The greater the duration of the outbreak and the longer measures to prevent its spread remain in place, the greater the ramifications for global supply chains, global trade and growth.

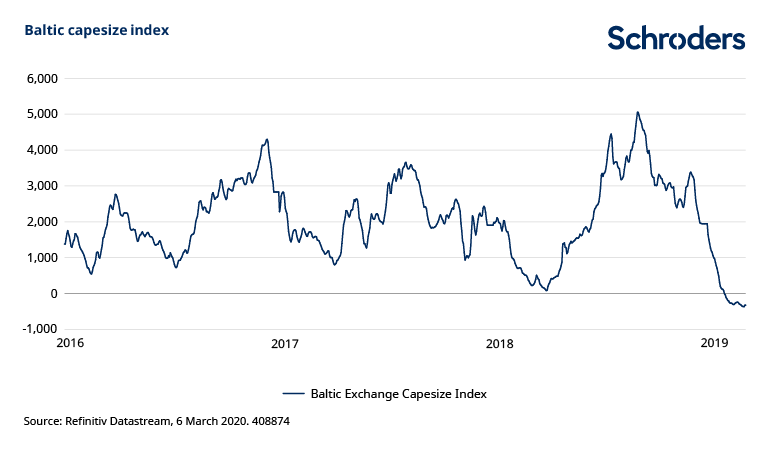

The Baltic Exchange’s Capesize Index has turned negative

The majority of world trade is transported by ship. With container companies cutting back sailings to China, owing to coronavirus concerns, backlogs at Chinese ports have increased. Should these persist or continue to mount, total global trade, in terms of both volume and value, could fall.

Those economies which are more exposed to trade, including the majority of Asia but also Australia and Europe, may feel the chill. South Korean car manufacturer Hyundai has already had to close several of its plants in South Korea due to a shortage of parts which are imported from a company in China.

The Baltic Exchange’s Capesize Index, atracker of global shipping volumes of the largest bulk container vessels, turned negative for the first time ever earlier this month, as the chart above illustrates.

Other effects have included cruise ships in several Asian ports falling under quarantine, with passengers restricted to their cabins for 14 days. Those economies more reliant on tourism more broadly may be impacted, in particular those with a high dependence on visitors from China. We will be exploring the impact on sectors in further articles on Schroders Insights.

Views from Schroders Australian Multi-Asset team

Simon Doyle, Head of Fixed Income and Multi-Asset, said: "Our view was, and remains so, that China’s role in global supply chains is much more critical today than before and that we are starting from a much weaker position in terms of both economic fundamentals globally and monetary dry powder.

Central banks (and governments) will respond. The US Fed and the RBA have already cut rates. We will also likely see a fiscal response in Australia as the government deals with a series of shocks impacting the local economy. While the playbook of late has been for markets to respond favourably to central bank support, the headwinds may be a bit stronger this time around, with the pronounced yet uncertain economic and social implications of COVID-19 yet to be fully understood.

We were relatively well positioned for the COVID-19 outbreak and its spill-over into markets – not because we had any special insight or forewarning, but because our investment process had been clear on the point that valuations were stretched and risk premium narrow. This made markets vulnerable to any shock that pushed the economy off its narrow and optimistic path, even if the timing was impossible to predict."

Never miss an insight

Stay up to date with all of our latest content by hitting the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Established in 1961, Schroders in Australia is a wholly owned subsidiary of UK-listed Schroders plc. Based in Sydney, the business manages assets for institutional and wholesale clients across Australian equities, fixed income and multi-asset and global equities.

We believe in the potential to gain a competitive advantage from in-house global research; that rigorous research will translate into superior investment performance. We believe that internal analysis of investment securities and markets is paramount when identifying attractive investment opportunities. Proprietary research provides a key foundation of our investment process and our world-wide network of analysts is one of the most comprehensive in funds management.

1 topic

1 contributor mentioned

Schroders

Established in 1961, Schroders in Australia is a wholly owned subsidiary of UK-listed Schroders plc. Based in Sydney, the business manages assets for institutional and wholesale clients across Australian equities, fixed income and multi-asset and...

Expertise

Schroders

Established in 1961, Schroders in Australia is a wholly owned subsidiary of UK-listed Schroders plc. Based in Sydney, the business manages assets for institutional and wholesale clients across Australian equities, fixed income and multi-asset and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets