COVID concerns and world trade’s surprising resilience

“When you do testing to that extent, you’re going to find more people, you’re going to find more cases…So I said to my people, ‘Slow the testing down, please.’ They test and they test.” President Trump, Tulsa Rally, 21 June 2020.

In a relatively quiet week ahead for domestic and global data, attention is likely to focus on signs that COVID-19’s spread is potentially less contained than hoped. As we have been highlighting for some time—and a catalyst for trimming our emerging market (and overall equities) position from 1 June—the spread of the virus has been accelerating in a number of large less developed economies, namely Brazil and India. Germany has also seen (likely containable) cluster outbreaks toward the end of last week. And in Australia, Victoria has, over the past few days, seen a surge of community transfers sparking debate over the pace of easing lockdown restrictions and border openings.

For Australia, one of the more interesting data points this week will be the international trade data for May. As a reminder, Australia’s trade data has been positively surprising, with an AUD 8.8 billion surplus in April after a record AUD 10.5 billion surplus in March. This has been driven, in part, by elevated prices for our resource exports (particularly iron ore), as well as the domestically led collapse in import demand. China’s Q2 efforts to re-start its economy, particularly via domestic infrastructure activity (creating demand for our bulk commodities), has also helped. While May is likely to see a further pull-back in the surplus, the better-than-expected data has been supporting Australia’s growth, currency and Prime Minister Morrison’s budget.

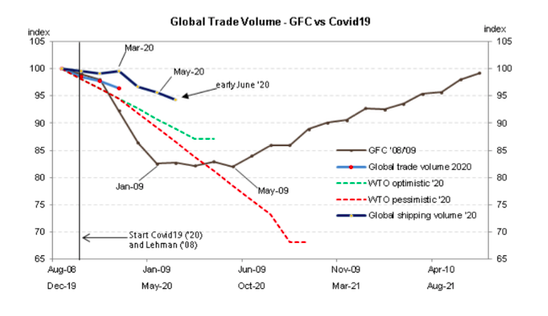

This brings us to our chart today, which highlights some interesting UBS Evidence Lab research which tracks 28,000 container ships around the world with the goal of getting an early read on trends in world trade—both its decline and recovery. Two things stand out. Firstly, and surprisingly, there has been a relatively modest slowing in world trade so far this year. As the chart shows, early June data is down only 6% compared with a decline of 18% during the GFC. Moreover, World Trade Organization simulations suggest trade volumes should fall between 13% and 32% this year. The only modest slowing in global trade may be indicative of better underlying demand conditions globally.

The second feature is that, despite a bounce in global manufacturing PMIs in May and June (in part due to the easing of lockdown restrictions), the data does not yet show any signs of a rebound in shipping volumes. There is a range of less positive reasons why this may be the case, hinting at a further slowing in trade volumes ahead. The reasons include a significant lag between when businesses re-open, demand recovers, and new supplies are ordered. Further, business uncertainty is also likely to weigh on the willingness to order (and instead run-down inventories and order less). And finally, PMIs are overstating the extent of a pick-up in activity, with rebounds more likely indicating things are not getting worse, rather than that getting better.

What world trade collapse?

Source: UBS, WTO, Haver, CPB.

Follow our daily updates

We share Crestone Wealth Management views on a range of macro topics that we're watching. Click the ‘FOLLOW’ button below to be the first to hear from us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment