CSL Limited: Moving into value territory

The Commonwealth Serum Laboratories was established in Australia in 1916 to service the health needs of Australia during world War I. Since then CSL has provided Australians with rapid access to 20th century medical advances including insulin and penicillin, and vaccines against influenza, polio and other infectious diseases. CSL Limited was incorporated in 1991 and listed on the Australian Securities Exchange (ASX) in 1994.

Market Cap: $89.23b

Share Price: $196.96

Subsequently CSL has acquired a number of companies which have now folded into three main divisions:

CSL Behring

CSL Behring is a global biotechnology leader supplying a broad range of quality medicines to markets throughout the world. Therapies are provided for bleeding disorders, immunodeficiencies, hereditary angioedema, neurological disorders and Alpha-1 Antitrypsin Deficiency.

CSL Plasma

A subsidiary of CSL Behring, CSL Plasma is the largest collector of human blood plasma in the world, sourcing plasma from hundreds of thousands of donors globally to produce a range of life-saving medicines for critically ill patients.

CSL Seqirus

Seqirus is one of the largest influenza vaccine companies in the world and a major partner in the prevention and control of influenza globally. It is a transcontinental partner in pandemic preparedness and response, and a leading supplier of influenza vaccines to global markets for both northern and southern hemisphere seasons.

Recent share price fall

Although CSL has recently fallen from highs of $230 per share down to $196 at current levels, over the last year investors has still seen a one-year return of roughly 30%. As growth stocks have outperformed the broader market over the last few years (notwithstanding recent share price falls) investors have become acclimatised to CSL’s steep share price inclines. The recent negativity surrounding the stock is based upon uncertainty around the valuations attributed to high growth stocks and broader market sentiment. Despite this, CSL has managed to outperform key industry peer Cochlear (+15% over 1 year) due do its strong economic moat and the projected long term growth thematic in its plasma and influenza businesses.

R&D day

On the 5th of December 2018 CSL hosted a briefing to update investors on R&D activity.

R&D Investment Breakdown

The group faces a leaner period with regard to product launches, although we remain comfortable that the rapid product rollout in the past couple of years will support earnings growth for the foreseeable future. CSL have committed to spending 10% of global revenue on R&D for new and existing products.

- R&D is focused in Australia; revenue is primarily derived from the northern hemisphere.

- CSL have had 5 major product launches across all divisions over the last 12 months, focused mainly around influenza vaccines – it has been a huge achievement for the company and the highest number t in its history. They are making meaningful contributions to the business now and will continue to do so in the future.

- CSL’s core plasma business is predicted to grow at high single digits annually for the next several years. This is a good organic growth figure, but given CSL’s growth profile it will look for significant contribution from products in the R&D pipeline. Russia is the key sector for expansion; with a population of 144 million people there is unmet need for immunoglobulins which is 10 to 15 times lower per capital in Russia as it is in the U.S.

- FDA approved new influenza vaccine for six month old children for the rest of a person’s life. The U.S. health department has recommended the entire population of the United States over the age of six months be vaccinated. (previously it was only six month – four year olds) Large growth potential.

- Expecting their new cell based influenza vaccine approved in Europe for over nine year olds (cell based is a new treatment that adapts with changing influenza viruses). Cell based influenza treatment was approved in the U.S. in 2016 and now CSL is confident their new treatment will be approved in Europe over the next year.

- The same dossier that was submitted to the U.S. government recommending children be vaccinated from the age of six months (for the rest of their lives) is being submitted to the Australian market which they expect to be approved in 2019. Currently the Australian government recommends the vaccine for ages five and over.

- Expected approval of specialised vaccines for over 65 years old in the U.S. in 2019 and then will submit to European and Australian governments following U.S. approval.

Our view

After falling 14% from its highs we believe that CSL is moving into value territory given its expected earnings outlook and its history of outperformance vs market expectations. CSL is Australia’s largest healthcare business with exposure to international and domestic healthcare spend. It is the number one and preferred player in the market; working alongside governments to provide the best healthcare possible for the masses. It is committed to fair and even distribution of approved treatments, regardless of how high or low the price of a product can be sold for, setting up solid foundations for future business in different regions around the globe.

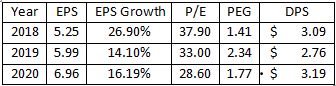

The FY18 result was impressive. Revenue grew by 11% to $10.6 billion, earnings per share (EPS) increased by 29% to $5.25 and the total full year dividend grew by 26% to $3.09 per share. CSL’s P/E has always been high, justified by delivering consistent and sustainable EPS growth. It invests heavily in research and development to create the next products that will help people, drive profits and strengthen political goodwill. Strong immunoglobulin demand, a 24% increase in its specialty products sales, and a 53% increase in influenza vaccine sales were the key drivers behind recent performance.

Additionally, a broader theme supporting CSL is its unique market position with unmatched size and distribution channels; when new treatments are developed, CSL will have the opportunity to buy them and use their extensive production and distribution networks to monetise their investments. For smaller developers, CSL provide scale, and thus have first right of refusal when new products come to market. Management remain positive on revenue growth from both new and existing products and have a history of consistently outperforming expectations.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 stock mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment