Debt LIT discounts in focus

Rodney Lay

Risk Return Metrics

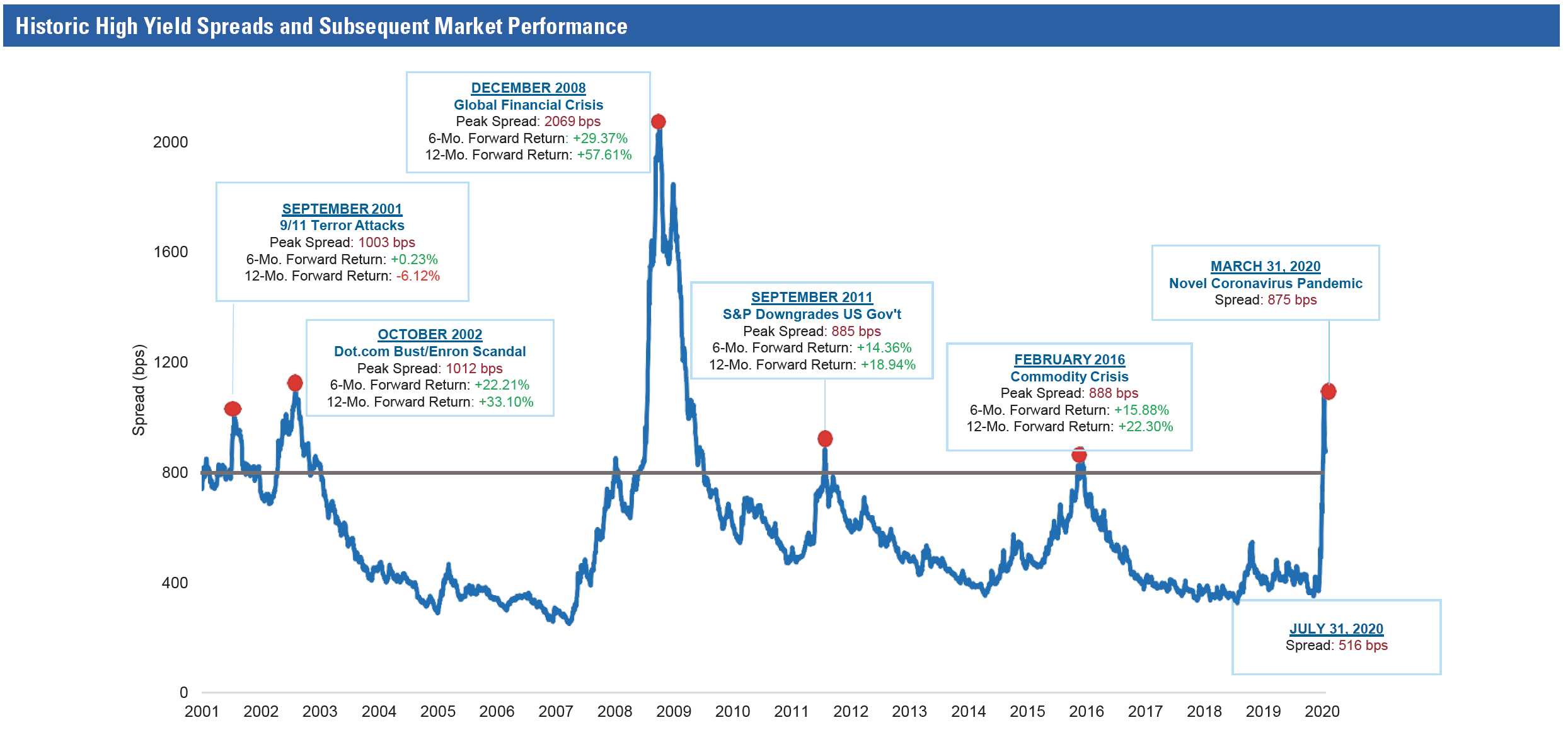

The latest Listed Managed Investments Monthly for July 2020 focuses on the implied default rates of each debt listed investment trust and compares these figures to historic averages in the aggregate high yield and loans markets.

The conclusion: implied default rates of all debt listed investment trusts (LITs) are not correlated with historical rates, neither at the broad market nor manager levels.

For example, Gryphon Capital Investment’s (ASX:GCI) 7.5% discount to NTA at 31 July 2020 (now 11%) implies a default rate (as opposed to loss-given-default) of around 150%, assuming a recovery rate of 95% across its Residential Mortgage Backed Security (RMBS) book. We remind investors, Australian RMBS has never experienced a single default.

We also put the spotlight on GCI and the state of play in the Australian RMBS section and Regal Investment Fund (ASX:RF1) following a volatile performance period.

A PDF containing the full report is available below.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Investment analyst with particular experience in listed and unlisted investment strategies, equities and structured products.

4 topics

2 stocks mentioned

Rodney Lay

Risk Return Metrics

Investment analyst with particular experience in listed and unlisted investment strategies, equities and structured products.

Expertise

Rodney Lay

Risk Return Metrics

Investment analyst with particular experience in listed and unlisted investment strategies, equities and structured products.

Expertise

Comments

Comments

Sign In or Join Free to comment