Defensive Equities: The best of both worlds

Christopher Dixon

Cooper Investors

Surely few topics have had more column inches dedicated to them than discussions around predicting market peaks and troughs. This has become evident again in the commentary and headlines amidst volatility caused by COVID-19.

Have we seen the market bottom? Have markets run too fast? Have central banks written cheques corporate earnings can’t cash? Is it too late to buy or should we wait for a retest of the lows?

While tempting to engage in such dialogue, this is unhelpful thinking for true long term investors.

As observed by David Swensen, Chief Investment Officer at Yale University in his seminal book on endowment investing Pioneering Portfolio Management, market timing is not a strategy because it cannot be consistently applied with any degree of success.

You might get lucky once or twice, but in the long term you’re betting on a coin toss. Studies have shown investors who are consistently out of the market during the best days of each year significantly underperform long term averages - as the old adage goes, building wealth is about time in the market, not timing the market.

Of course, it is human nature to desire gains whilst trying to avoid the pain of loss.

And avoiding pain is especially important when approaching the end of an investment life, a period when new savings can be minimal (or even zero) and there may be enforced regular distributions for, say, individuals in decumulation phase or perhaps a bequeathed trust fund. For a pensioner the opportunity to recover from a significant market drawdown is impaired by both urgency (recovery could be years away) and the inability to dollar cost average (hard for retirees to put fresh savings in at the market lows like a youngster can).

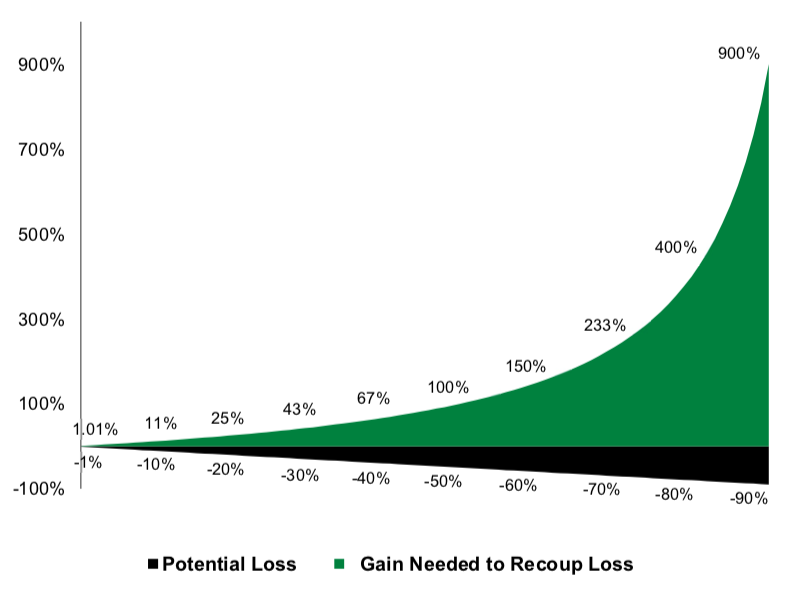

Consider the simple maths of market drawdowns. As the size of the loss grows it requires exponentially more upside to recover – a stock that halves needs to double to get back to par.

But can we ideally keep up with the market and avoid if not all, then some of the downside - can we have the best of both worlds?

At Cooper Investors we have refined our investment philosophy for Endowment or decumulation phase investors around the concept of ‘Capture Spread’; the difference between upside and downside capture for a given portfolio.

Consider the following theoretical exercise

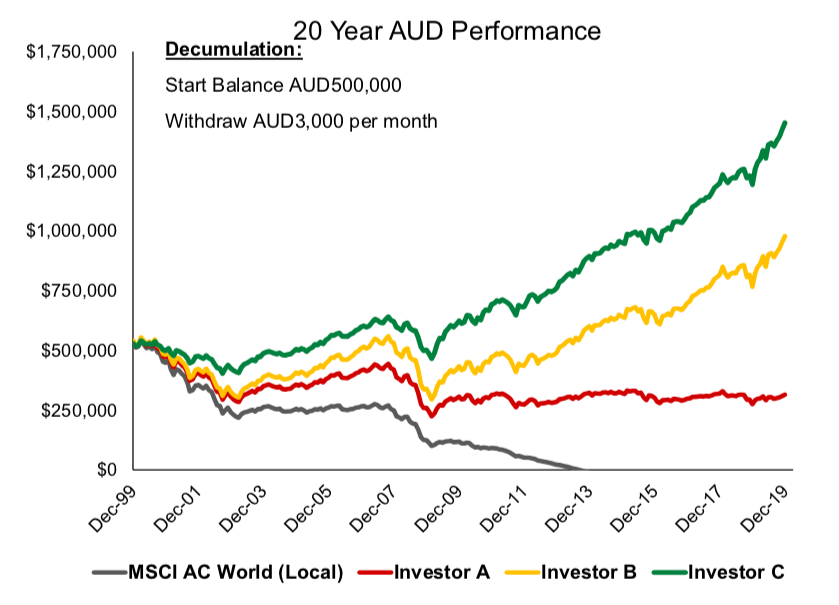

Four investors each invest AUD500k into Global Equities 20 years ago and withdraw AUD3k a month (7% of initial capital per year) to live on. One invests in the index (MSCI AC World) while the other three construct equity portfolios that provide varying participation in the index return.

Investor A keeps up with a rising market (Upside capture of 100%) and does a bit better in a falling market (Downside Capture 80%) for a ‘Capture Spread’ of 20% (100% - 80%).

Investor B beats a rising market by 10% (Upside capture of 110%) while similarly beating a falling market (Downside capture of 80%) while Investor C lags the rising market (Upside capture 80%) but takes less than half of drawdowns (40% Downside capture) for Capture Spread of 40%. In summary:

- Index Investor: Downside Capture 100%, Upside Capture 100%

- Investor A: Downside 80%, Upside 100% = Capture Spread 20%

- Investor B: Downside 80%, Upside 110% = Capture Spread 30%

- Investor C: Downside 40%, Upside 80% = Capture Spread 40%

What are the conclusions?

The index investor runs out of money after 13 years.

With some downside protection Investors A, B and C have extended their pools of capital and with a Capture Spread of above 30% Investors B and C have actually grown their assets. But the clear winner here is Investor C.

With significantly lower downside capture, despite lagging rising markets and 7% per annum distributions, their capital has almost tripled over the journey. While these outcomes may of course differ with alternate time periods it seems reasonable (especially in light of recent events) to model significant drawdowns as at least once-in-a-decade events.

So what are the key areas to focus on when constructing a portfolio for capture spread, and specifically lower downside capture?

Diversification is of paramount importance. Global equity correlations have been rising and recently hit similar levels to the GFC around 0.9. In an Endowment portfolio the aim is to have, as far as possible, stocks that do different things and are exposed to diverse end markets, employing an ‘anti- thematic’ mindset. Example diversifiers in the Cooper Investors Global Endowment Fund are Swedish family-linked industrial investment firm Latour AB (STO: LATO-B) and Canadian gold royalty company Franco-Nevada (TSE: FNV). The latter actually exhibits negative correlation with many equities.

Regarding Portfolio Construction, Endowment portfolios are biased towards more stalwart-type companies and will be underweight cyclicals. Note this does not mean zero cyclical exposure – during cyclical rallies a portfolio with no cyclicals might lag to an unacceptable extent so some high quality cyclical exposure is warranted and indeed is a further desirable source of diversification.

Finally Stock Selection hurdles require additional consideration than in a fund seeking short term outperformance. With a desire to take less risk there is little tolerance for balance sheets carrying high debt loads or for companies lacking pristine track records of earnings quality, capital allocation and governance behaviours.

A 'capture spread' strategy

At Cooper Investors we create domestic and international Endowment-style portfolios that aim to have lower volatility than their respective markets and to outperform during periods of weakness. Click the 'FOLLOW' button below for more insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris has been co-PM of the CI Global Equities Fund since November 2011, focussing on European and Japanese companies. He has travelled extensively, living in four countries and investing across multiple asset classes over his 15 year career.

1 topic

Christopher Dixon

Portfolio Manager - Global Equities Funds

Cooper Investors

Chris has been co-PM of the CI Global Equities Fund since November 2011, focussing on European and Japanese companies. He has travelled extensively, living in four countries and investing across multiple asset classes over his 15 year career.

Expertise

Christopher Dixon

Portfolio Manager - Global Equities Funds

Cooper Investors

Chris has been co-PM of the CI Global Equities Fund since November 2011, focussing on European and Japanese companies. He has travelled extensively, living in four countries and investing across multiple asset classes over his 15 year career.

Expertise

Comments

Comments

Sign In or Join Free to comment