Dividends the size of Jupiter!

With Australian investors love of resources and a passion for dividends, it seems incredible that a company could yield over 24% in a commodity with strong fundamentals and growth drivers.

Jupiter Mining (JMS AU) listed on the ASX in April 2018 and has since seen their share price slide from an IPO price of 40c, down to a low of 23c! The price has recently rallied back to around 31c as a potential supply shock has awakened investors.

Recently the Ghana Manganese Company (GMC) was ordered to stop production from the government in Ghana pending an audit of the company due to suspicions they were not paying the government their fair share. Welcome to Africa!

This potential supply shock adds to an already tight Manganese market. Depending on how long this shut down lasts, the price of manganese could react favorably. That said, the supply side in the manganese market has tightened anyway with restrictions in China and supply depletion of existing mines. Along with increased demand due to Electric Vehicles (EV) and Chinese steel demand the fundamentals for Manganese look strong. The price of Manganese has been steady and is forecast to rise in the years ahead.

Jupiter is a 49.9% owner of the Tshipi manganese mine in South Africa. The majority ownership is of the project puts the Black Economic Empowerment (BEE) with a larger percentage than is required under South African ownership laws (so the political/geographical risk could be perceived as lower than if this ownership slice was smaller?). While this risk maybe warrants a discount, how much discount should be expected for such an asset?

Jupiter is debt free and is a tier 1 mine (lowest cost quartile producer) with a high grade, long mine life (100+ Years) and a board determined to focus on this single asset and return capital to shareholders - the strategy seems simple.

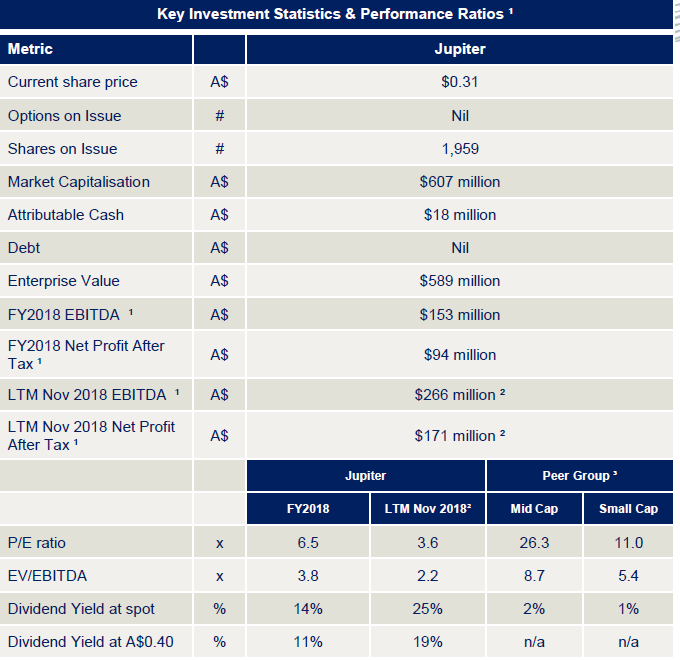

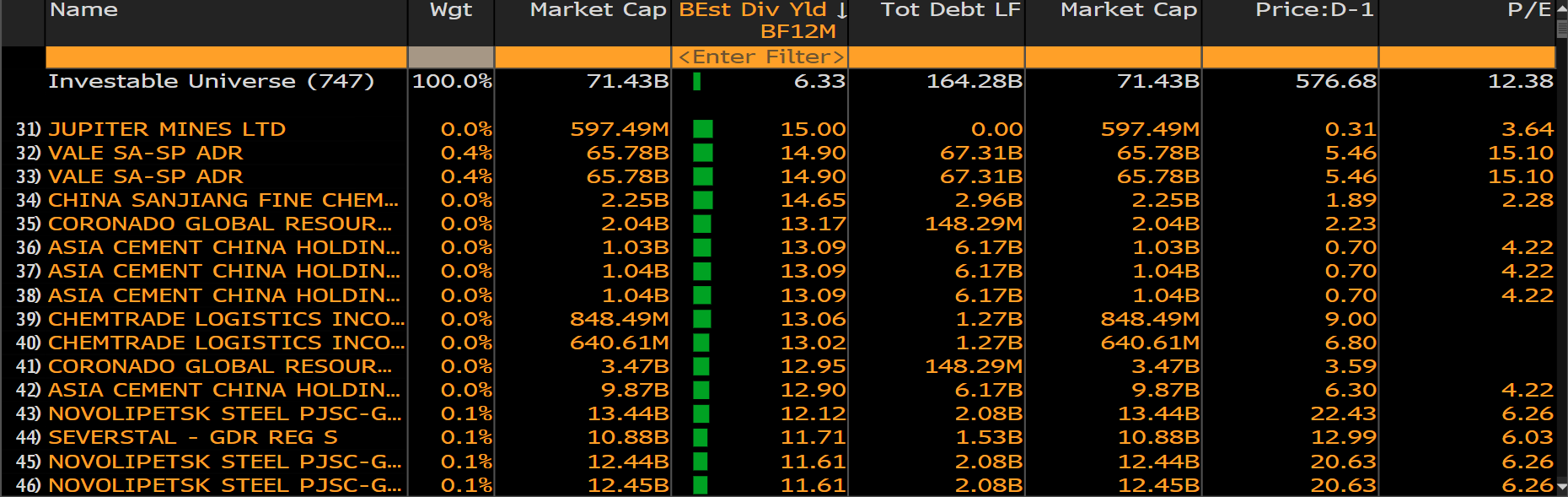

The company has essentially said they plan on paying out the majority of free cash flow as dividends and have been paying out far more than they indicated in the prospectus (>70%). Some of the metrics are listed in the table below.

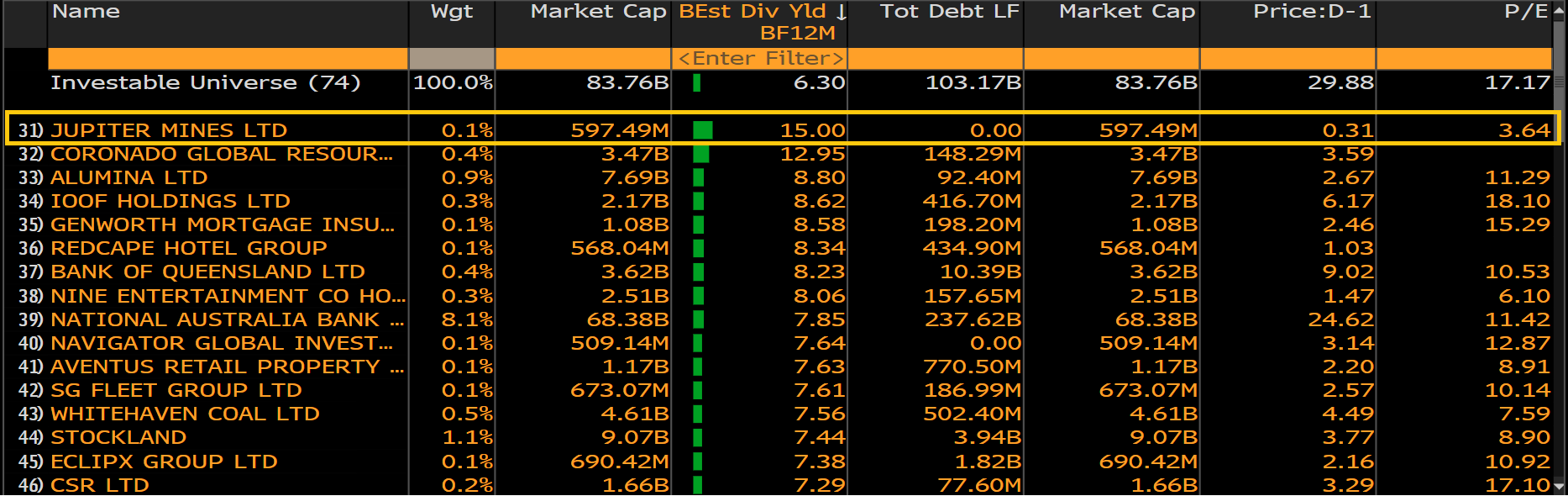

To date, the company has delivered on their promises and is currently the highest yielding stock on the ASX, trading on a P/E of 3.64x earnings. The 2.5c dividend recently declared (Ex-Div 6th of May) along with the 5c already paid (7.5c since listing) puts the yield at 19% from IPO and 24% from 31c. With the potential upside in the manganese price, it seems there is a low risk to earnings ahead and more dividends for patient shareholders.

In fact, JMS is not only the highest dividend payer in Australia but also one of the highest yielding resource companies across the developed World (although earnings risk on some of these others names looks much higher - Vale for example!).

It seems incredible that such a long life, tier 1 asset could trade at such attractive valuations with such attractive dividends. With a supply shock to the manganese market and investors starting to take note, perhaps Jupiters boring business is finally getting noticed by investors.

Disclosure: We own shares in JMS AU

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott is the Executive Chairman at Fiftyone Capital. As the previous CEO, Scott founded the company to manage not only his own wealth, but the wealth of other investors and families looking for a safe harbour for their capital.

1 topic

1 stock mentioned

Scott is the Executive Chairman at Fiftyone Capital. As the previous CEO, Scott founded the company to manage not only his own wealth, but the wealth of other investors and families looking for a safe harbour for their capital.

Scott is the Executive Chairman at Fiftyone Capital. As the previous CEO, Scott founded the company to manage not only his own wealth, but the wealth of other investors and families looking for a safe harbour for their capital.

Comments

Comments

Sign In or Join Free to comment