Do you really want to set and forget?

Nick Reddaway

Drummond Capital Partners

The annual returns of investment markets are clearly positive over a long period of time, and when markets go through bad periods often the advice is to effectively stand pat. This advice may be appropriate for a young professional with 30 years of earnings and accumulation ahead of them, but for investors who are approaching retirement or have just sold a business and invested their life’s work, this is the last thing they need.

While relying on the long-term average return of asset classes to decipher optimal portfolios is fine, it doesn’t really account for the variation that can occur in the medium term nor the changing relationships between assets over time.

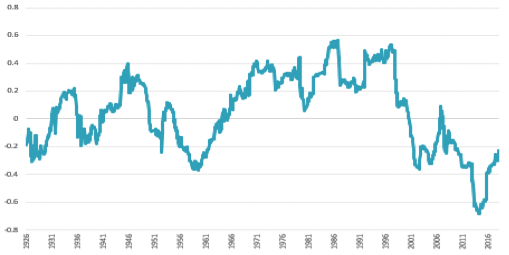

Diversified asset allocation typically refers to having a combination of growth assets (equities) and defensive assets (bonds). Bonds did exceptionally well during the financial crisis in 2008 while equities did poorly. So by owning bonds your overall portfolio performance was better than just owning equities. Yet even this relationship changes dramatically over time (see below).

Rolling 5-year US Bond & Equity Correlation (1926-2018)

Source : Drummond Capital Partners, R. Shiller

Clearly, there are times in capital markets when you want exposure to risk premia and times when you don’t. We base our strategic asset allocation on 40 years of data given some 90% of returns are derived from long term asset allocation decisions rather than individual security or manager selection. Yet we know, and expect, that the future will be very different from the past.

Importantly, we recognise that each client’s investment experience can differ wildly depending on when they began their investment journey. A 20% drawdown today can equate to a large dollar value for investors that have already accumulated a large pool of assets that may not be so concerning to those at the start of that journey. Our primary obligation (and our obsession) is to manage this risk for our clients. No one knows the sequence they will get into the future. It is not acceptable to just assume that future returns will resemble the long-term average return without active management.

To help put into perspective the necessity for active asset allocation, consider the forward 10-year total return from the ASX All Ordinaries Accumulation Index.

ASX Forward 10yr Return vs Average Return

Source : Drummond Capital Partners, Reuters

As you can see, the average annual return from 1979 to 2018 has been 11% p.a. However, someone beginning their investment journey in 2007 on the premise of the long term 11% p.a. return but then only achieving 3% p.a. over the next 10 years, may indeed wish they had opted for a different asset mix given the coming volatility in equities. The severely negative returns through the financial crisis in 2008 get completely swallowed by average returns over long periods. While this supports the argument to stick with it in fear of making the wrong decision at the wrong time, it doesn’t make the person in question feel any better about their actual experience.

Of course, we cannot predict the future of markets any better than the next person and we don’t try to. We do however know that recommending to our clients a static asset mix based on long term average returns simply doesn’t reflect what their actual experience will be like. Instead of being put in a static box of defensive, balanced or growth for example, most clients we speak to want to take risk when it’s going up, and take chips off the table when it’s not. It’s common sense.

Winning by not losing

Realistically, severe negative periods are typically felt in equity markets every decade. So not being able to significantly reduce risk when fundamental market conditions change just doesn’t make sense. The problem is that there is no single set of rules that works, no single event or indicator that works across time in all markets. And of course, markets often go down faster than the time afforded to investors on the way up. That’s why investors must be nimble and have conviction.

Using a set of fact-based inputs along with significant experience as active portfolio managers to drive the tactical asset allocation framework over the medium term (i.e. moving the portfolio between a growth and balanced or conservative position) a dramatically better outcome can be achieved. By adopting this approach, we do miss some of the peaks but our clients avoid the worst of the significant market drawdowns. Over time this preservation of capital and active participation in the good times creates a significantly better investment journey.

Ultimately we believe a considered, experienced and rational approach is required with a capital preservation mindset always at the fore

What you say and what you do

There was no one reason for the sudden risk off environment in October. Perhaps the hawkish fed and rising rates were the trigger but underlying that was a culmination of other factors (Emerging Markets weakness, trade wars, credit concerns, peaking global growth, rising rates, quantitative tightening and full valuations) that finally saw the buyers stand back. It’s not a trivial list.

We wrote about the risks in our Q2 and Q3 quarterly and of course lots of commentary has surfaced in reaction to the drawdown, exploring the reasons for the weakness and what to do - or not do - now.

We acted to significantly reduce risk in the third quarter. We took our clients’ portfolios exposure to growth assets from our neutral position of 50% to a defensive level just below 30%. Timing is everything and we did this ahead of the point where markets capitulated. The typical diversified portfolio (60% growth / 40% defensive) has now experienced their worst drawdown since the financial crisis across October and November.

The below chart shows the Australian equity market and the actual 2 periods where we took steps to reduce our Australian equity exposure by 40% (the red circles showing when we sold Australian equities).

40% Reduction in Australian Equities in Q3

This action was mirrored in our international equity exposure and other parts of the portfolio. Neither of these were knee-jerk reactions to weak markets but rather were a considered approach to reducing portfolio risk in an ongoing assessment of the underlying market conditions.

Being in a defensive position during this period afforded us the time to assess the value emerging in the equity markets driven by the ongoing risks already touched on rather than worry about large falls in the value of our portfolios.

Today we consider that many of the markets worries prior to the fall have in some way been addressed. Steps have been taken towards a more positive trade war outcome; the Federal Reserve has become less aggressive in its tone towards rising rates; growth expectations have become more realistic for 2019 and bond yields have fallen making equities relatively more attractive. Given equities have become cheaper at the same time despite these positives emerging, we felt it was an opportune time to move from this defensive position in growth assets towards a balanced position.

We have refrained from increasing exposure to large capitalisation Australian equities given the structural headwinds facing many of Australia's largest corporates on top of the freeze in Australian property and the negative consequences that could have for the economy. For now, Australia is cheap for a reason and we view other parts of Asia offer greater value.

While we have moved our portfolio back towards a more neutral stance in growth assets, we are cognisant of the many risks that remain in the global economy. Our portfolios remain liquid, and currently have 40% allocated to alternative investments. Consequently, our clients’ portfolios remain in a relatively conservative position.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nick has spent over 18 years working in alternative asset management roles including co-founding an Australian long-short fund. Nick also recently co-founded Drummond Capital Partners, which manages globally diversified multi-asset portfolios.

Nick Reddaway

Managing Partner / CIO

Drummond Capital Partners

Nick has spent over 18 years working in alternative asset management roles including co-founding an Australian long-short fund. Nick also recently co-founded Drummond Capital Partners, which manages globally diversified multi-asset portfolios.

Expertise

Nick Reddaway

Managing Partner / CIO

Drummond Capital Partners

Nick has spent over 18 years working in alternative asset management roles including co-founding an Australian long-short fund. Nick also recently co-founded Drummond Capital Partners, which manages globally diversified multi-asset portfolios.

Expertise

Comments

Comments

Sign In or Join Free to comment