Don’t judge a property by its building

Asset quality is more than just an attractive building. Most properties are valuable because of something else entirely.

Not long after my daughter turned five I took her to see her first movie, “Up”. It’s about an elderly man who, along with an unexpected young friend, tries to re-capture his youthful passion for adventure as ‘greedy developers’ (is there any other kind?) attempt to bully him out of his beautiful home – a home he and his recently-deceased wife had shared their entire life together.

It was a great movie, with many positive messages. And for me, naturally there was also a message about real estate. Those developers were offering anything they could to convince the old man to sell. Why? The house itself had no real value for the developers (but enormous value to the old man) – no, the property was valuable because the house sat on valuable land.

When the old man initially purchased the home, it was rundown and located in a neighbourhood of no particular note. But with the passage of time, and the benefit of demographics, this once simple home became very desirable (high quality) real estate.

It’s all about the land

Back in 1998, I was fortunate to have the opportunity to meet Milton Cooper, the founder and executive chairman of Kimco Realty – one of the first of the new listed REITs in the United States.

One of his philosophies stands out as a lasting memory. The idea was that land is where investors generate growth and eventually their total return, but the problem is that by itself, land is hard to finance and therefore difficult to hold for a period of time. Improvements are a necessary way of earning income, which allows the land to be financed and held for a long period of time. Ultimately, however, the improvements are cost of ownership via economic depreciation.

Ten years later, “Up” only helped to reinforce this idea.

The trick, it seems, is to identify very high quality land with a very low build cost (or at least a low cost to maintain), and generate enough current income that can attract appropriate finance (debt and equity).

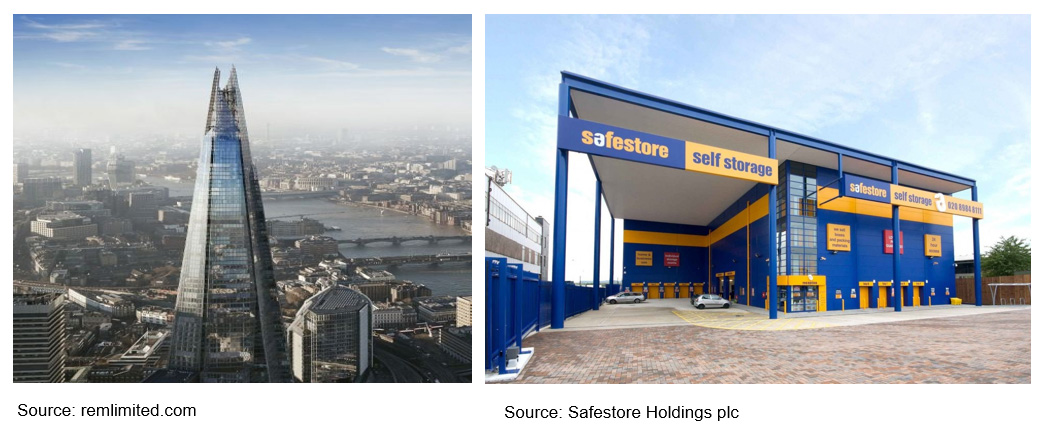

The building on the left is an office tower located in London called “The Shard”, owned by the State of Qatar. On the right is a storage facility also located in London, owned by listed REIT Safestore.

Most investors see the property on the left as very high quality: a prominent, well-located asset, with an institutional quality tenant roster and located in one of the most economically important cities in the world. It would also look great on an investment brochure.

I believe an argument can be made that the property on the right is of higher investment quality. Why?

- Recalling the lesson from Mr Cooper at Kimco, the improvements in real estate are really just a vessel in which to hold the land. In the long run, low cost improvements represent a low economic cost of holding the land.

- The Shard already represents the ‘highest and best use’ – the only real upside is from land appreciation, and the land represents a relatively small proportion of the asset’s value.

- Like the old man’s house in “Up”, the storage facility is probably not the highest and best use; hence its current value is likely to be understated.

- If land is to increase by (say) 5% per annum, there will be a better total return for assets where the land/build ratio is high (i.e. the value of the property is dominated by the value of the land). That is clearly true for the storage facility, where the value of the improvements (per square metre of land) are miniscule compared to the Shard.

- Finally, office tenants generally require significant capital contributions and incentives to sign or renew a lease, which further adds to the capital intensity of ownership – although, to be fair, we do not know enough about the Shard to know to what extent it applied in this specific case. Storage facilities have near zero capital commitments to new or existing tenants.

Identifying the opportunities

So the idea is simple enough, right? We just need to find storage facilities in major cities at a cheap price.

Sadly, that’s easier said than done. But there are other strategies that can take advantage of Mr Cooper’s incredibly valuable insight – that is, to identify real estate where the maintenance capital expenditure (what we call “stay in business CAPEX”) is low.

One of the great inefficiencies in real estate valuation (of which there are many) is the application of a capitalisation rate (multiple) to pre-tax, and pre-depreciation property income. And while we accept that at times valuation multiples try to encapsulate ongoing depreciation, the approach tends to be blunt and sometimes clumsy. Applying a more quantitative approach, we believe, leads to better investment decisions.

While some sectors may not look pretty for the purposes of a glossy brochure (e.g. Storage, Manufactured Homes, Healthcare), they have a powerful investment advantage: low ongoing CAPEX means more free cash for dividends and re-investment. For us at Quay, that means higher quality real estate.

Our own approach to defining asset quality includes thinking of land as the growth asset, and the improvements a vessel and cost to allow owners to finance the land – thereby effectively land-banking over the long term; and viewing REITs through the prism of an operating business, where low ongoing CAPEX allows more free cash flow for re-investment – and knowing that over time, this is a powerful investment advantage.

Asset quality is more than just an attractive building. It’s about attractive total returns.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris has nearly 30 years of experience working as a real estate specialist, with a background in investment banking and equities research. Prior to co-founding Quay, he worked in real estate investment banking at Credit Suisse and Deutsche Bank.

1 topic

Chris has nearly 30 years of experience working as a real estate specialist, with a background in investment banking and equities research. Prior to co-founding Quay, he worked in real estate investment banking at Credit Suisse and Deutsche Bank.

Chris has nearly 30 years of experience working as a real estate specialist, with a background in investment banking and equities research. Prior to co-founding Quay, he worked in real estate investment banking at Credit Suisse and Deutsche Bank.

Comments

Comments

Sign In or Join Free to comment