Election watch: What the U.S. race means for investors

Matt Reynolds

Capital Group

Heading into 2020, the U.S. presidential election looked set to be one of the biggest stories of the year. The coronavirus pandemic drastically changed that narrative, pushing politics aside as a health care crisis triggered the worst economic downturn since the Great Depression.

With the U.S. election now less than 100 days away, however, investors are turning their attention back to the November 3 ballot. Amid rising COVID-19 infections, a battered economy and civil unrest in several U.S. cities, President Donald Trump is trailing former Vice President Joe Biden by a wide margin in major polls.

Many pundits are already predicting a resounding defeat for the incumbent president, but it’s far too early for investors to anchor on that outcome, says Capital Group veteran political economist Matt Miller.

“We have more than three months to go before the election. That’s a lifetime in politics,” Miller says. “Given the rapid pace of developments and a compressed news cycle, we could have many turns of the wheel between now and November. In my view, the race will tighten as the Republican and Democratic campaigns shift into overdrive.”

Election scenario planning

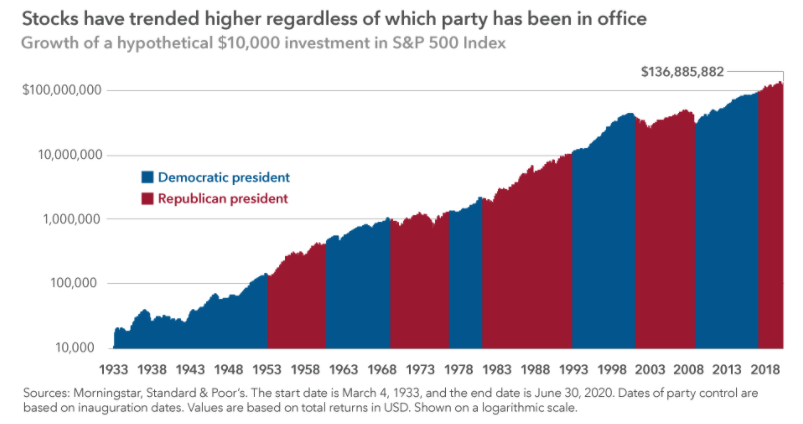

For long-term investors, the outcome of U.S. presidential elections hasn’t mattered as much as staying invested and maintaining a diversified portfolio. Markets have tended to power through presidential elections — with some volatility along the way — regardless of whether a Democrat or a Republican won the White House.

That said, election scenario planning plays a role in macroeconomic analysis, particularly in recent years as governments have increasingly intervened in the financial markets during times of crisis.

Excluding a contested election — which is certainly within the realms of possibility — here’s a brief look at four scenarios that could play out in November and the implications for investors.

Scenario 1: Democratic sweep

Democrats win the White House, the Senate and maintain control of the House — otherwise known as a “blue wave.” This scenario would produce the greatest degree of political change, starting with the likely reversal of Trump’s policy agenda on many fronts, including taxes, immigration and regulation.

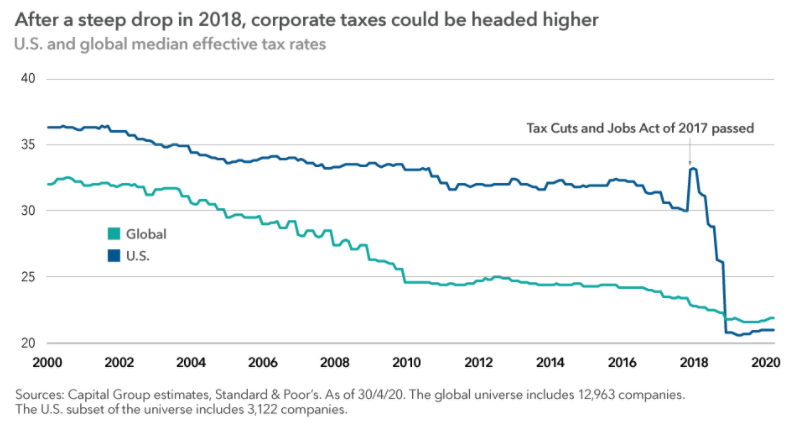

One result could be a full or partial rollback of the Tax Cuts and Jobs Act of 2017, which included significant tax reductions. Overall corporate tax rates declined from 35% to 21%, providing a major boost to corporate earnings. A full or partial reversal would have the opposite effect, prompting investors to take that into account when estimating the overall corporate earnings outlook.

“We would see a much bigger emphasis on taxation and regulation across the board, with significant implications for the energy sector, telecommunications and technology companies,” Miller explains. “We could also see the elimination of the filibuster in the Senate, which, unlike today, would allow legislation to pass with a simple majority vote.”

Scenario 2: Gridlock

Biden wins the White House; Republicans maintain control of the Senate. This outcome would likely result in a gridlock scenario where it could be difficult to pass major legislation. Senate Republicans could block major Democratic initiatives, much as they did during the second term of the Obama presidency.

“In this case, I think we would see Biden governing through executive orders,” says Clarke Camper, executive vice president and head of government relations in Capital Group’s Washington, D.C. office. “There would be a great deal of pent-up frustration on both sides of the aisle. That’s an easy outcome to predict, though, perhaps not as easy to live with.”

Under this scenario, federal regulatory agencies would also likely exercise more power. From a financial markets perspective, that could mean more aggressive enforcement by the Securities and Exchange Commission, as well as a renewed policy push by the Department of Labor in connection with its oversight of employee retirement plans.

Scenario 3: Status quo

Trump wins reelection, and Republicans keep the Senate. This scenario involves the least amount of change since it is, indeed, where we are today. The House is likely to remain in Democratic hands, so the current environment of political confrontation would continue — along with the rancorous but so far successful attempts to approve COVID-19 relief legislation, including the $2 trillion CARES Act (Coronavirus Aid, Relief, and Economic Security Act).

“Regardless of who is in the White House in January, there's going to be a lot of post-COVID cleanup work to do,” explains Reagan Anderson, a senior vice president with Capital’s government relations team. “Today we are in stabilisation mode, and we will hopefully be moving into recovery mode by 2021.”

Scenario 4: Unlikely split

Trump wins reelection, and Democrats take the Senate. This scenario could set the stage for even greater hostility than we’ve seen in the past two years. While such an outcome is theoretically possible, it’s unlikely given the political dynamics of key Senate races, which increasingly track the presidential vote in each state.

“For instance, if Republicans lose key Senate races in Arizona, Colorado, Maine and North Carolina, then that’s clearly indicative of a ‘blue wave,’” Miller explains. “It’s hard to imagine Trump winning the White House if that happens.”

Either scenario involving Trump’s reelection raises another risk: If he wins without a majority of the popular vote as he did in 2016, Miller warns, that could lead to more civil unrest and further demands to abolish the Electoral College.

Investment implications

Election season can be a tough time for investors to maintain a long-term perspective, given the strong emotions often evoked by politics. Campaign rhetoric tends to amplify negative and divisive issues. This election, in particular, is unprecedented in modern times — marked by the combination of a deadly pandemic, a global economic recession, widespread civil unrest and extreme market volatility.

Moving to the sidelines would be an understandable approach for anxious investors who prefer to wait and see what happens. As history has shown, however, that is often a mistake. What matters most is not election results, but staying invested.

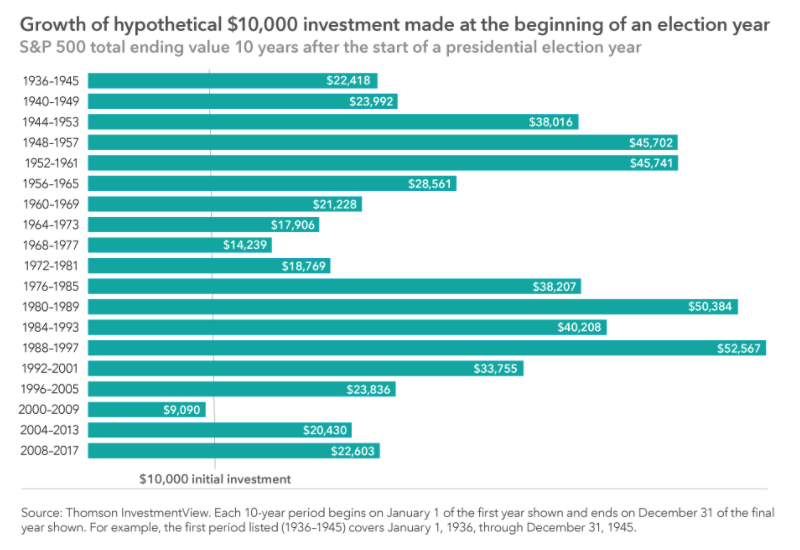

Consider the historical performance of the Standard & Poor’s 500 Composite Index over the past eight decades. In 18 of 19 presidential elections, a hypothetical $10,000 investment made at the beginning of each election year would have gained value 10 years later. That’s regardless of which party’s candidate won. In 15 of those 10-year periods, a $10,000 investment would have more than doubled. While past results do not guarantee future returns, election-year jitters should not deter investors from maintaining a long-term perspective.

The only negative 10-year period followed the election of George W. Bush in the year 2000. During that decade, the S&P 500 posted a negative return amid two seismic events: the 2000 dot-com crash and 2008 global financial crisis.

In contrast, the biggest election year return would have been in 1988, when George H. W. Bush won office, and $10,000 would have grown to $52,567 by the end of 1997.

By design, elections have winners and losers, but the real winners have been investors who stayed the course and avoided the temptation to time the market.

Put today’s investment news into long-term perspective

Capital Group believes in a smarter way of investing that combines individuality and teamwork into a tailored approach to help investors meet their goals. Find out more by clicking 'CONTACT' below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The University of Sydney. He also holds the Chartered Financial Analyst designation. Matt is based in Sydney.

2 topics

1 contributor mentioned

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Matt Reynolds

Investment Director

Capital Group

Matt Reynolds is an Investment Director at Capital Group. He has over 20 years of industry experience including head of Australian equities – core at Colonial First State Global Asset Management. He holds a bachelor's degree in Economics from The...

Expertise

Comments

Comments

Sign In or Join Free to comment