Emerging Market Debt: Dumb, Dumber and Dumbest

One of the classic signs that the credit cycle is nearing the end is that borrowers that shouldn’t be getting financed not only get funded, but get it at terms that seem crazy. I’ve recently written about the silly things happening in global high yield debt, Chinese debt and the global attitude to sovereign debt. Continuing this theme are recent examples of emerging market sovereign debt; Greece, Argentina and Iraq. Each of these shouldn’t have been funded, but the desperation for yield saw all three get funded on terms that seem crazy. Here’s the detail on each.

Argentina

In June, Argentina sold $2.75 billion of US dollar denominated 100 year bonds at a yield of 7.92%. At the time, this was a mere 5.18% yield pick-up over 30 year US treasuries. Argentina has a long history of defaulting on its government debt, including 4 defaults in the last 35 years. The 2001 default took 15 years of negotiation and litigation to resolve, with most bondholders losing their shirts and a few who bought late and fought hard getting extraordinary returns.

The current outlook shows that not much has changed for Argentina. Inflation is running at over 20% and the government is aiming to cut the deficit this year to 4.2% of GDP, hoping to stimulate the economy out of recession. Investors are banking on the recent change in government to increased foreign investment and see sound economic management implemented. The need to reduce politically popular subsidies will be a major hurdle to that. S&P’s rating of “B” and Moody’s at “B3” reflect the country’s weak credit profile. Taking all of this into account, Argentina is unlikely to get through a decade without defaulting let alone 100 years.

Greece

In July, Greece sold €3 billion of 5 year bonds at 4.63%, a 4.78% yield pick-up relative to 5 year German government bonds. Investors have particularly short memories on Greece’s debt, with the 2012 default seeing bondholders take losses of around 75%. The 2014 issue of 5 year bonds traded as low 56% of face value, a horrible ride for those who bought into it. The constant negotiations for further bailouts always come with the threat that Greece won’t make further concessions and this time the Europeans and the IMF might have had enough.

Greece’s position remains precarious, debt to GDP currently stands at 179%. The economy has been stagnant for years as its government continues to resist the structural reforms proposed by the IMF and Europeans. Some are optimistic as Greece recorded a primary surplus (before interest expenses) in 2016. However, to achieve a fulsome surplus Greece needs to be funded at around 1%, well below the 4.78% yield it is paying bond investors. Unlike the buyers of the recent bond issue, S&P (B-) and Moody’s (Caa2) don’t see good prospects for Greece paying back its creditors.

Iraq

In early August, Iraq sold $1 billion of 5 year bonds at 6.75%, a 4.93% premium to US treasuries. Iraq faces three major medium term issues; the ongoing war, export revenues reliant on upon oil prices and dependence upon military and financial support from the US government. Each of these is out of its control. The 2016 deficit at 14% of GDP shows Iraq clearly cannot service its debts without a substantial financial turnaround. By buying the bonds, investors have effectively banked the equity case of the war ending and oil prices improving. The credit ratings from S&P (B-) and Moody’s (Caa1) are a better reflection of Iraq’s economic prospects.

Conclusion

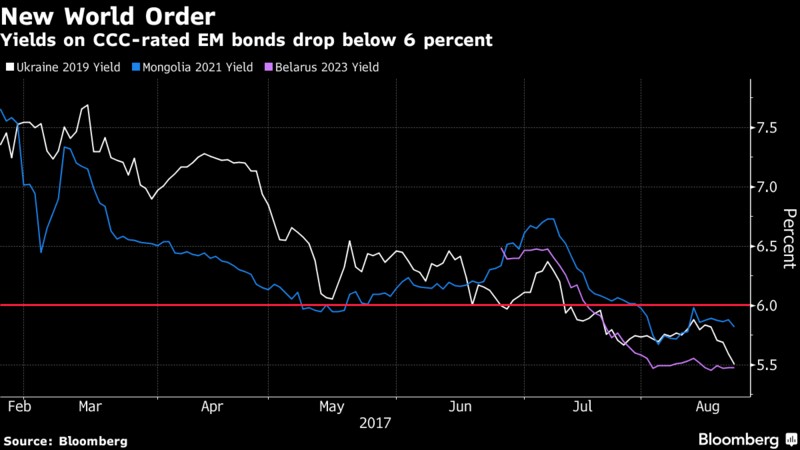

In considering emerging market debt, investors have to be careful to consider each country on its own merits. In the examples of Argentina, Greece and Iraq, bond buyers have suspended sceptical analysis. They’ve banked the equity case, hoping for a substantial change from historical precedents, even though they won’t get a share of the upside if the rosy scenario occurs. The examples aren’t unusual; as shown in the graph below from Bloomberg Belarus, Mongolia and Ukraine are all CCC+ rated but have bonds yielding less than 6%.

These examples point to the greater fool theory playing out in many credit markets. We’ve now reached the point in the credit cycle where further gains seem dependent upon more dumb money arriving and pushing spreads even tighter. Calling the top of any cycle is nearly impossible, but calling out the current higher risk/lower return environment is simply common sense.

Written by Jonathan Rochford for Narrow Road Capital on August 24, 2017. Comments and criticisms are welcomed and can be sent to info@narrowroadcapital.com

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

4 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment