Emerging Markets are leading the way in Fintech

The marriage of finance and technology, or fintech, is finding a natural home in emerging markets (EMs), where the penetration of traditional banking and insurance services is typically low. The lack of infrastructure and growth of mobile phones make emerging markets ripe for alternative financial solutions. In many cases, consumers have leapfrogged traditional financial service offerings straight to online solutions. Importantly, these fintech companies are reaching an ever‑larger audience, offering unique services that traditional banks cannot. With many EM companies leading the charge, there are growing opportunities for investors.

Fintech growth is accelerating at a blistering pace

Some 2 billion adults globally still do not have a bank account—most of whom live in emerging markets. Advances in fintech are working to broaden financial inclusion. Consumers are increasingly able to benefit from new innovations in the way financial service firms deliver products and services.

A huge driver of this trend has been the rapid proliferation of mobile phones and improving internet connectivity. Since infrastructure can be more limited, many developing countries might be described as “mobile first.” For many people, mobile handsets are their sole connection to financial tools, information, and other vital services. Fintech companies are using that to their advantage, devising financial solutions to meet the distinct requirements of these markets.

Asia is at the vanguard of the fintech revolution, leading the way in consumer adoption of financial technology products and services. In China and India, more than half of adult consumers active online said they regularly use fintech services,1 according to a 2017 survey conducted by Ernst & Young. Meanwhile, sub‑Saharan Africa accounts for more than half of mobile money services worldwide. With the massive growth in the emerging world middle class, fintech companies are seizing the opportunity.

The lack of infrastructure and growth of mobile phones make emerging markets ripe for alternative financial solutions. - Chuck Knudsen, Portfolio Specialist, Emerging Markets

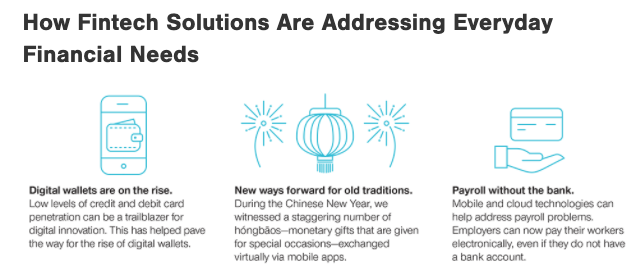

How Fintech solutions are addressing everyday financial needs

Low levels of credit and debit card penetration can be a trailblazer for digital innovation. This has helped pave the way for the rise of digital wallets, which have become increasingly popular in emerging economies. Companies like Alibaba or Tencent benefited from the huge growth in this area.

This becomes particularly obvious during Chinese New Year when a rising number of hóngbāos—monetary gifts that are given for special occasions—are exchanged virtually via mobile apps. In 2019 alone, more than 820 million electronic “red packets” were sent over China’s Lunar New Year holiday, according to WeChat. That means that more than twice the population of the United States used WeChat’s hóngbāo feature during China’s new year holiday.

Mobile and cloud technologies can also help address payroll problems. Firms such as M‑Pesa, a mobile money transfer service based in Kenya, have been at the vanguard in that regard. It means that employers can pay their workers electronically, even if they do not have a bank account.

Building partnerships to develop solutions

Africa is a global leader in mobile money, which has become an important component of the continent’s financial services landscape. Mobile network operators have been first to take advantage, but more recently, fintechs have established a solid footing in the market, and several banks are beginning to compete aggressively for the mobile banking customer.

While some banks have chosen to “go it alone,” others are forming partnerships in hopes of reaching the market faster. These companies span the full spectrum of financial services, from payments and current accounts, to savings, loans, investments, and insurance. Just over half of the 282 mobile money services operating worldwide are located in sub‑Saharan Africa, according to the GSMA, an industry organisation that represents the interests of mobile network operators worldwide.

Mobile and cloud technologies can help address payroll problems.- Irmak Surenkok, Portfolio Specialist, Emerging Markets

A recent report by McKinsey suggests that there are currently around 100 million active mobile money accounts in Africa. This far exceeds customer adoption in South Asia, with 40 million active mobile money accounts creating the second biggest region for mobile money in terms of market share. And these companies are solving a genuine problem. Until recently, it would have been incredibly difficult for migrant workers in Nairobi, for example, to send wages back to their family who are living in the countryside. Now they can do so at the touch of a button.

Why now for Fintech?

We are excited by the potential for software‑enabled payments where the opportunity is vast and could cause an upheaval in the payment industry. Up to now, the first step in a merchant’s life consisted of a trip to the bank to seek financing to start their venture. A payment‑processing product was therefore a natural cross‑sell for banks. Today, merchants start their journey by choosing a software that will help them manage their new business. That change is driving a shift in payment distribution away from banks and toward software‑enabled payment providers.

But the payment industry has more room to grow. In addition to software‑enabled payments, business‑to‑business (B2B) payments will likely also cause a stir in the fintech sector. These firms look to fill the gap left by banks’ withdrawal from small and medium‑sized enterprise (SME) lending, while also providing solutions in payment processing and workflow streamlining. B2B is a multi-trillion‑dollar market that rivals the consumer payments industry in size. The industry is just beginning to gravitate toward more modern payment technologies and away from manual processes. This could drive growth for the payments industry for many years to come.

Financial institutions are also now beginning to speak “fintech” and are becoming more aware of how innovation can transform their businesses. Established technology companies are seeing the value of partnering with fintechs as they tackle the complexity of entering the financial services industry—for example, local regulation, capital requirements, and reputational risk.

Disruption of the industry pulled forward

Financial inclusion in developing markets has become even more important during the coronavirus pandemic. For those who cannot access mobile phones, the ability to visit bricks‑and‑mortar banks and manage their money has been even more limited, if not cut off entirely, worsening the already very limited availability and support offered by traditional banking in many emerging countries. Mobile solutions are proving to be a lifeline in emerging economies, and that issue of accessibility has been brought front and centre into the minds of consumers. Those who have been able to access the internet in such markets find that through their fintech services they can instantly tap in to much‑needed financial resources to keep their businesses and lives in order.

Financial inclusion in developing markets has become even more important during the coronavirus pandemic - Daniel Hurley, Associate Portfolio Specialist, Emerging Markets

As the whole world shifts toward a new reality, there will be an abundance of post‑pandemic opportunities for businesses. There will be new niches and exciting ideas as people realise that the digital tools on which they have relied during this disruption are, in fact, providing important services, regardless of the conditions. Fintech firms can use this opportunity to build their reputations and emerge even stronger once the crisis has passed.

Key insights

- Digital innovation is disrupting and reshaping financial services at a rapid pace.

- Emerging markets are leading the way in this new world of Fintech, with many companies at the forefront of innovation.

- Inclusivity in financial services has become even more important for consumers in emerging markets during the coronavirus pandemic, and fintech firms are poised to capitalise.

1 EY FinTech Adoption Index 2017: The rapid emergence of FinTech.

Invest with confidence

T. Rowe Price focuses on delivering investment management excellence that investors can rely on—now and over the long term. Hit the 'follow' button below for more of our investment insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott Berg is the portfolio manager for the T. Rowe Price Global Growth Equity Strategy.

2 topics

Scott Berg is the portfolio manager for the T. Rowe Price Global Growth Equity Strategy.

Expertise

Scott Berg is the portfolio manager for the T. Rowe Price Global Growth Equity Strategy.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management