Equities: Baton Now Passed to Earnings

Nick Morton

Resonant Asset Management

In this note, we contend that the global share market rally, which has been primarily US equity market driven, has thus far been entirely driven by central banks. The next phase will need to be driven by actual earnings and the real economy if it is to be sustained, and that will be a much trickier task.

Mission Accomplished

The Fed’s actions in March and April, note just in terms of size but in terms of scope, and way before the real economic impact of the coronavirus could be reliably forecasted, have propelled US equities by 11.3% on a rolling 1 year basis, as at end of May.

Mission accomplished? In terms of monetary stimulus (Figure 2), and the levers this central bank has at its disposal – the Fed may well think so – given we appear to have seen the peak in unemployment figures (Figure 1), and equity markets have rallied handsomely, bringing with it a degree of confidence.

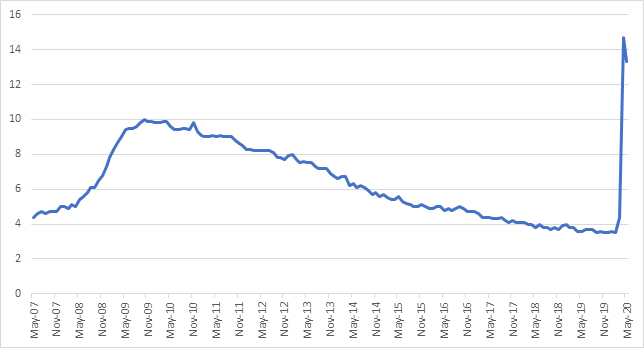

Figure 1: US Unemployment Rate ticks down in May 2020 from April Peak (source: Refinitiv Eikon)

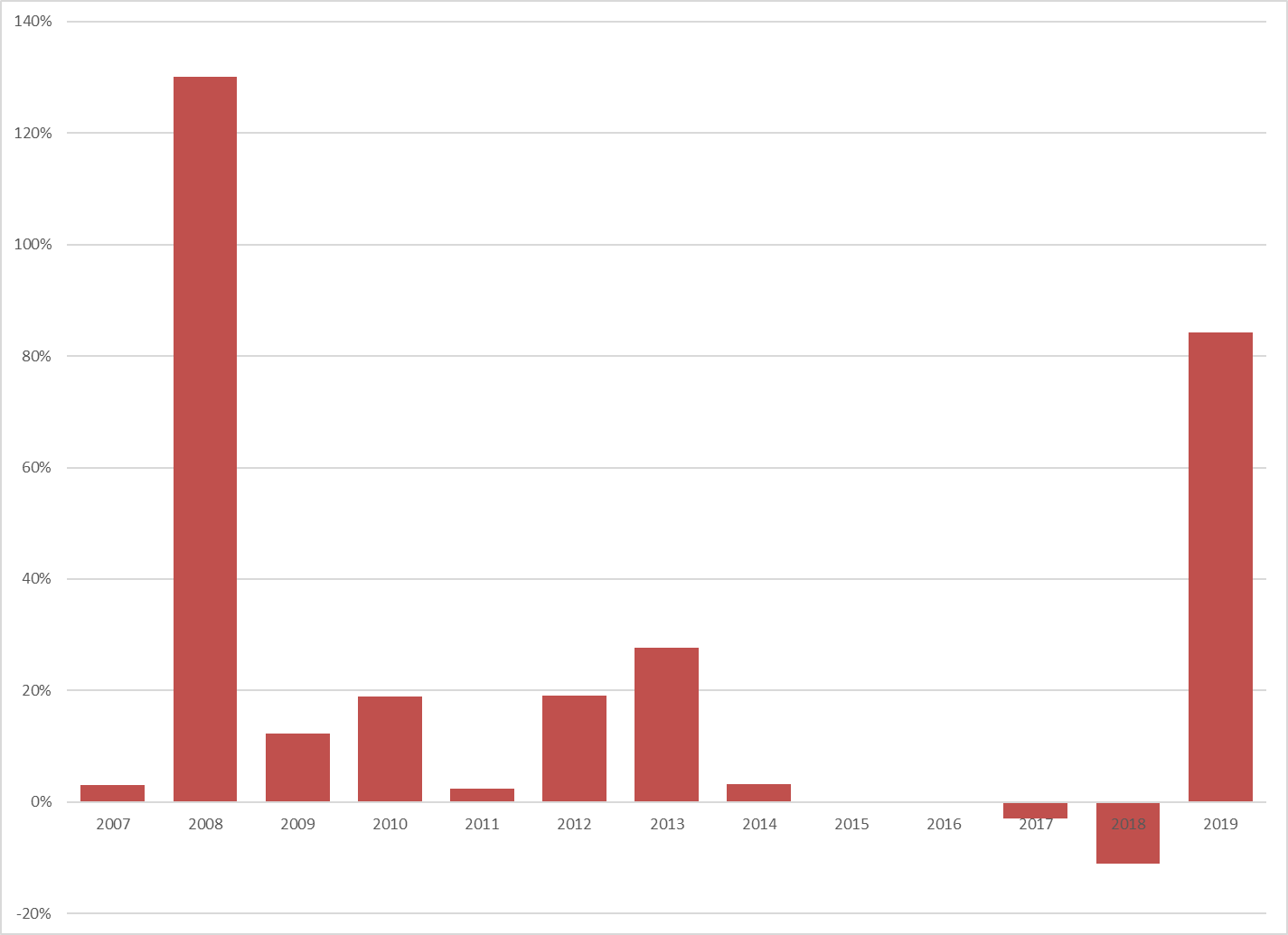

Figure 2: Fed Balance Sheet Asset growth (source: Refinitiv Eikon, Resonant Calculations)

But how much of this rally is explained by the Fed's actions, as opposed to increasing optimism, earnings, or corporate actions such as buy-backs?

To understand the future, as investors we need to understand the past.

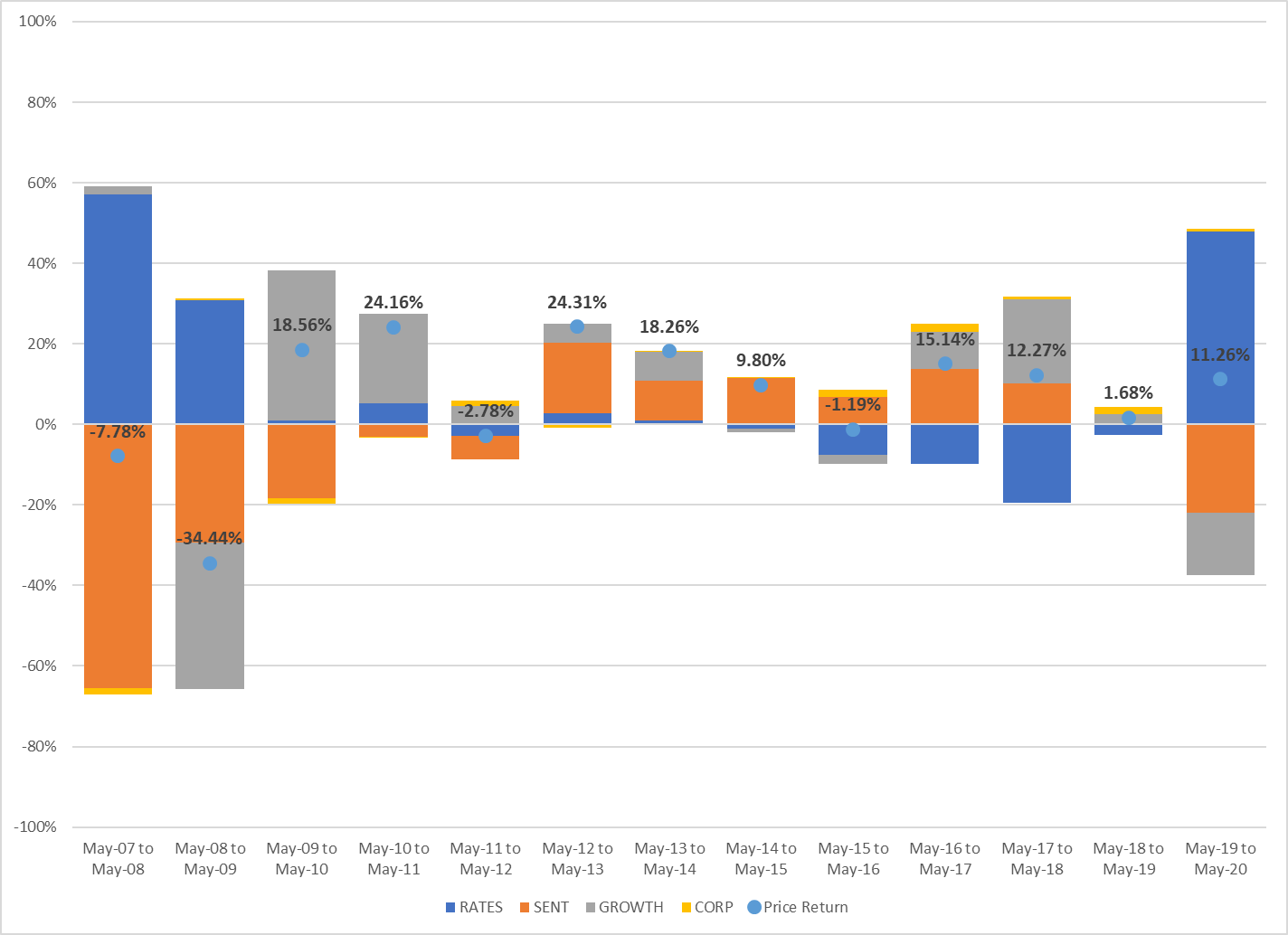

Resonant’s framework uses four factors, sentiment, corporate actions, growth, and rates.

In breaking down on the index level returns, Resonant decomposes price returns into four categories (figure 3):

Sentiment (SENT): Are investors feeling more or less confident about the outlook for the economy and shares? Sentiment and confidence plays a key role in bull markets.

Corporate actions (CORP): Have companies been buying back shares (positive) or raising equity (negative)? Buy Backs increase earnings per share, and raising decrease earnings per share. This lever is particularly relevant for Australian Equities.

Growth (GROWTH): Have companies been growing the bottom line? Typically if the economy is growing healthily then this will feed through to earnings, and through to the index.

Rates (RATES): Has the Central Bank been incrementally more supportive of risk assets? We use bank bill futures where possible, to incorporate fluctuations not just in the base rate, but in the banks’ collective willingness to lend.

The

four components are additive – so for the most recent reading, the price return

of 11% on the MSCI US index has been driven uniquely by Rates (+48%), counteracting Sentiment

(-21%), Growth (-15%). This suggests that without Fed Support, the Equity

market would have fallen -37% on a rolling 12 month basis as at end of May!

Figure 3: 4 factor breakdown of US Equity Returns (source: Refinitiv, Datastream, IBES, MSCI, Resonant Calculations)

The key takeaway from this chart is that this is a "risk-off rally" – the sentiment contribution (SENT) is negative for the 12 months leading to May 2020, which is an unusual state of affairs, and probably why so many professional investors are feeling uncomfortable.

The only other year since 1997 in which the contribution from sentiment was negative, and the market rallied is 2009-2010, which was driven by significant earnings growth as the economy came out of the great recession.

If indeed the most significant Fed monetary policy actions are complete then the baton will shift to earnings (GROWTH) – and these are potentially only currently reflecting a short lived recession, and nothing as deep as was experienced in 2008.

This may prove more challenging for US companies to achieve these sell-side earnings forecasts over the next 12 months.

Get investment ideas from industry insiders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nick has over 20 years of experience in markets, including 7 years at Citigroup as Head of Australian Quant Research, and 2 years at the CFS GAM Australian Core equities fund. He is CIO and co-PM of Resonant’s multi-asset SMA’s with direct stocks.

........

Resonant Asset Management Pty Ltd ABN 41 619 513 076, AFSL No 511759. Resonant is not licensed to provide personal financial advice to retail clients. The Information within this wire does not constitute personal financial advice. In preparing this document, Resonant has not taken into account your particular goals and objectives, anticipated resources, current situation or attitudes. You should therefore consider the appropriateness of the material, in light of your own objectives, financial situation or needs, before taking any action. You should also obtain a copy of the PDS of all products referenced before making any decisions. The data, information and research commentary in this document ("Information") may be derived from information obtained from other parties which cannot be verified by Resonant and therefore is not guaranteed to be complete or accurate, and Resonant accepts no liability for errors or omissions. Resonant does not guarantee the performance of any fund, stock or the return of an investor's capital. Past performance is not a reliable indicator of future performance.

1 topic

Nick Morton

Co-Portfolio Manager

Resonant Asset Management

Nick has over 20 years of experience in markets, including 7 years at Citigroup as Head of Australian Quant Research, and 2 years at the CFS GAM Australian Core equities fund. He is CIO and co-PM of Resonant’s multi-asset SMA’s with direct stocks.

Expertise

Nick Morton

Co-Portfolio Manager

Resonant Asset Management

Nick has over 20 years of experience in markets, including 7 years at Citigroup as Head of Australian Quant Research, and 2 years at the CFS GAM Australian Core equities fund. He is CIO and co-PM of Resonant’s multi-asset SMA’s with direct stocks.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

2 stocks to drive future performance following a 35% return in six months

Katana Asset Management