Fed hikes rates... and long-dated bonds rally

The US Federal Reserve raised rates 25 bps last night in the first of 3 expected rate hikes in 2017. Yet US government bonds have started to rally as US rates are rising. Isn't that counter-intuitive?

As JCB predicted in our recent note, long-dated bonds have started to rally as US rates are rising- something that many managers failed to predict. Do not under-estimate the potential of performance from long-dated bonds at this point in the cycle.

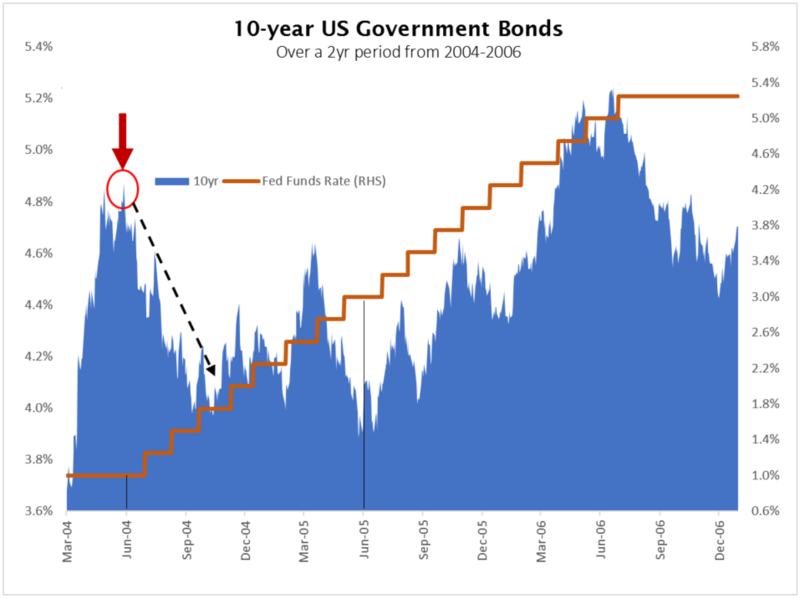

This is a critical ''Y'' in the road of the monetary policy cycle for investors to reconsider their asset allocations. The JCB investment team were all working in US fixed income markets during the last Fed rate-hiking cycle of 2004-2006 and are uniquely experienced to consider these issues and implications for asset class performance.

Long-dated bonds are primarily driven by inflation expectations and tend to perform very well after central banks start hiking interest rates. As inflation pressures build in the economy, long-dated bonds pullback to compensate investors for potential higher future inflation (as seen in Q4, 2016) Today's rate hikes heralds the arrival of the inflation fire fighter in the Fed, who by hiking rates today and committing to further rate hikes in 2017 have dampened future inflation expectation. Rate hikes slow the economy down and quell financial excess.

Longer dated bonds have started a relief rally in acknowledgement of:

a) future inflation pressures are being actively dealt with by the Fed; and

b) rate hikes will reduce the level of accommodation in the economy, slowing future financial activity

Do not under estimate the potential of performance from long dated bonds at this point in the cycle.

In 2004, despite the Fed raising funding rates 4 times by 100 bps, 10 year US Government bonds rallied (bond yields declined leading to higher prices) 99 bps for capital gains of more than 8.00% plus income for a total return of more than 10.50%. So funding rates up 100bps, and yet bond yields down 99 bps.

Over that entire hiking cycle of 2004-2006, the Fed raised funding rates by 425 bps. Despite this large move higher in funding rates that ultimately led to the GFC, 10 years US government bonds returned 6.50% over that period and went on to produce consistent returns for much of the past 10 years.

The start of a rate hiking cycle is a critical time for investors to reconsider their asset allocations. As the cycle continues other asset classes will become affected as the economy slows. Bonds had a tough run late in 2016 in acknowledgement of higher inflation pressures, but looking forward continued rate hikes will slow down the economy and tame inflation, and at some point this will have a negative effect on higher growth assets, many of which are still at record highs.

Have we started down the road to ruin leading to GFC mark II? We think this is unlikely as policy makers have learned a great deal from the lessons of the 2004-2006 cycle.

However, as the Fed continues to raise funding rates this will have significant effects on different asset classes including equities and other growth assets.

Sources: JCB Analysis

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Angus established Jamieson Coote Bonds with Charlie Jamieson in 2014. He started his career with JPMorgan in London, before working at ANZ and Westpac, where he transacted the first ever Australian Bond trades for several large Asian Central Banks.

Angus established Jamieson Coote Bonds with Charlie Jamieson in 2014. He started his career with JPMorgan in London, before working at ANZ and Westpac, where he transacted the first ever Australian Bond trades for several large Asian Central Banks.

Expertise

Angus established Jamieson Coote Bonds with Charlie Jamieson in 2014. He started his career with JPMorgan in London, before working at ANZ and Westpac, where he transacted the first ever Australian Bond trades for several large Asian Central Banks.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

This recently triggered market signal has never failed to predict gains

Ophir Asset Management