Finding security in a time of volatility

The last four months have been especially testing for investors. Many might now be thinking the best destination for a chunk of their portfolio is a biscuit tin buried in the backyard.

We’d take issue with that. Seasoned investors understand that market volatility is nothing new. Asset prices have gone up, down and sideways throughout history and there’s no chance of that changing. But the relative calm of the last few years does make the recent slumps and rebounds striking.

Let’s line up the concerns, all of which have been present for years but have recently taken on a more pressing threat.

First, the impact and scale of a US/China trade war seems to be gathering speed. Second, the risks of a no-deal Brexit appear to be growing. Third, questions remain over the monetary policy pathway adopted by central banks. Does it really make sense to raise rates when major economies appear to be slowing?

Locally, we have our own issues. The fallout from the Hayne Royal Commission continues; the residential property market slowdown shows no sign of reversing; and the long hoped-for increase in wages growth is notably absent.

Together, these threats are dialling up the ambiguity. For investors not prepared to bury their portfolios – and their heads – in the ground, thoughts naturally turn something more sedate – investments that offer the possibility of a good night’s sleep.

It is generally held that Australian Real Estate Investment Trusts (AREITs) come into their own during such times, especially for long-term investors in search of high income certainty and lower relative risk, with a little inflation-protection thrown in.

Now, research conducted by APN suggests they’re right. The share prices of AREITs just don’t jump around as much as ordinary shares. In fact, in periods of volatility they tend to outperform.

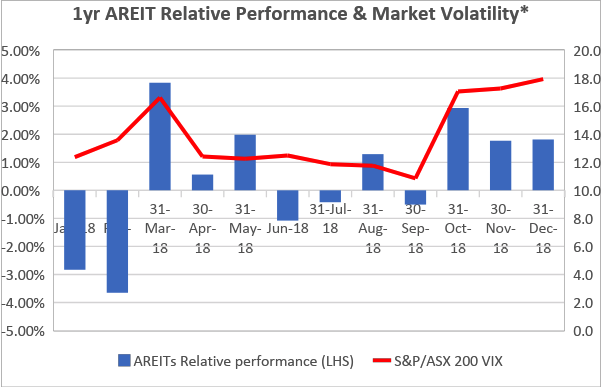

Just look at how the AREIT sector (S&P/ASX 200 AREIT Accumulation Index) has performed relative to the domestic equity market (S&P/ASX 200 Accumulation Index) through periods of elevated share price volatility over the past 12 months.

Source: IRESS, APN FM Jan 2019

*AREITs relative performance is the S&P/ASX 200 AREIT Accumulation Index less the S&P/ASX Accumulation Index. Market volatility is the S&P/ASX 200 VIX Index, used by investors, financial media, researchers and economists for insights into investor sentiment and expected levels of market volatility

The AREIT sector total return appears to exceed that of the broader equities market, as represented by the blue bars, while overlaid with periods where the volatility measure is relatively high, represented by the red line. That, you would imagine, is more conservative investments should perform.

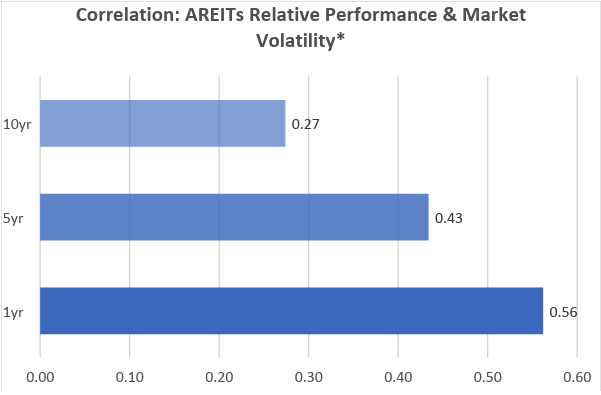

But one can’t learn too much from a solitary year. How did AREITs perform relative to equities through periods of elevated volatility over a 1-year, 5-year and 10-year time horizon? Correlation analysis helps us answer this question:

Source: IRESS, APN FM Jan 2019

*AREITs relative performance is the S&P/ASX 200 AREIT Accumulation Index less the S&P/ASX Accumulation Index. Market volatility is the S&P/ASX 200 VIX Index

What this chart tells us is that AREITs outperform during periods where market expectations of volatility are high. Moreover, the strength of this relationship appears to have increased in recent years. That suggests the defensive characteristics of AREITs have been in demand.

This isn’t really news to us, although evidence supporting our approach is always welcome. As specialist AREIT investors, we’re laser-focused on maximising the level and security of our Fund’s underlying distribution while minimising return volatility.

There are three characteristics in our underlying investment process that have helped to deliver this outcome:

1. Passive income focus – Concentrating our investments in AREITs that derive most of their earnings from contracted rental receipts, as opposed to relatively riskier sources like property development, funds management and transaction performance fees;

2. Asset quality – Directing exposure to the highest quality assets located in the deepest and most active markets. We believe over the long term these assets will be best positioned to deliver rental growth;

3. Appropriate capital structure – We prefer AREITs with a suitably conservative balance sheet and a defendable level of fixed debt coverage with a suitably long maturity profile across diversified sources of finance.

The analysis and attributes above suggest that in times of market turbulence investors might be well served by AREITs, especially those after high income-based returns with lower relative risk in an environment where expectations of continued volatility are higher than usual.

Never miss an update

Stay up to date with the latest news from APN Property Group by hitting the 'follow' button below and you'll be notified every time I post a wire.

Visit the APN Property Group blog to access the latest analysis and insights from a specialist real estate investment manager.

This article has been prepared by APN Funds Management Limited (ACN 080 674 479, AFSL No. 237500) for general information purposes only and without taking your objectives, financial situation or needs into account.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Mark is part of the Investment Team tasked with analysing and investing in global real estate-sector equities. He is an Associate of the Australian Property Institute, a Certified Practicing Valuer and a CFA charterholder.

1 topic

Mark is part of the Investment Team tasked with analysing and investing in global real estate-sector equities. He is an Associate of the Australian Property Institute, a Certified Practicing Valuer and a CFA charterholder.

Expertise

Mark is part of the Investment Team tasked with analysing and investing in global real estate-sector equities. He is an Associate of the Australian Property Institute, a Certified Practicing Valuer and a CFA charterholder.

Expertise

Comments

Comments

Sign In or Join Free to comment