Fiscal is the new black (…until the bond vigilantes return)

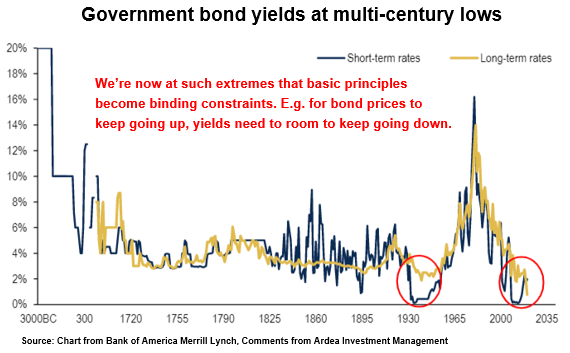

Unprecedented global fiscal stimulus. Extreme monetary policy experiments. Yields at multi-century lows. Government bond markets are now at the precipice of a paradigm shift.

In combination, these factors fundamentally change the risk vs. reward proposition of government bonds. So much so, they challenge conventional assumptions about how bonds should behave and the defensive role they are supposed to play in multi-asset investment portfolios.

Meanwhile, policymakers have the unenviable task of striking a very fine balance. Too little stimulus means a painfully severe recession. Too much risks loss of credibility on inflation control and government debt sustainability.

Faced with all this, it would be imprudent not to at least question whether government bonds are still the ‘safe haven’ they are assumed to be. To question whether interest rate duration is still a reliable hedge for equity risk.

At the risk of stretching metaphors too far, fiscal stimulus is now back in fashion and will remain so until the bond vigilantes (i.e. the fashion police) say, enough!

The term ‘bond vigilante’ was coined by former Yale economist Ed Yardeni in the 1980’s to describe bond investors who push back on excessive government spending by demanding higher risk premia (i.e. higher yields) on government bonds. They may be poised to make a comeback.

The fiscal stimulus unleashed globally over the past few weeks is astounding, both in terms of its speed and its scale. This amount of government spending is rarely seen outside wartime, and it is coming on top of a decade worth of accumulated monetary easing.

While the last decade was dominated by monetary policy, 2020 will be remembered as the year fiscal stimulus became fashionable again.

Right now, investors are entirely focused on the near-term economic damage from virus disruptions, which means markets are applauding every new stimulus program being announced. However, we will eventually reach a tipping point where the consequences of all this policy stimulus will have to be weighed.

- What does it mean for government finances, will bond investors start demanding more risk premium, will the bond vigilantes make a comeback?

- Can bond markets handle so much new government bond issuance, will longer dated bond yields shoot higher or will central bank buying be enough to maintain the supply vs. demand balance?

- At a time when monetary policy is already pushing new extremes, will so much fiscal stimulus cause longer term inflation expectations to shoot higher and what would that mean for the stability of currencies?

No one can answer these questions with certainty, but it is a safe bet that bonds will behave very differently going forward than they have in the past, which in turn has important implications for portfolio construction and the traditional assumption that government bonds are a ‘safe haven’ asset.

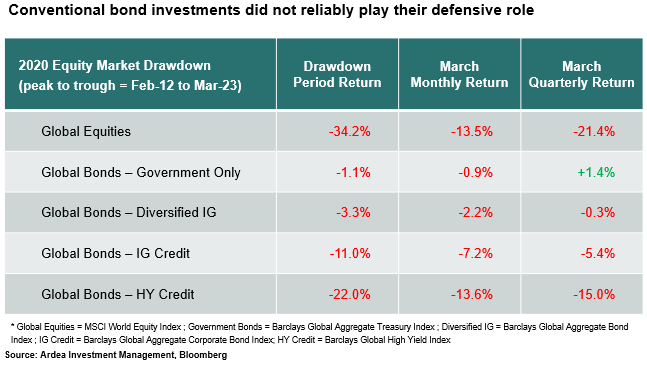

We’re already seeing these dynamics playing out as conventional bond holdings failed to hedge equity risk as reliably during the February / March global equity drawdown - one of the most violent on record – as they have in the past.

This changing behaviour of bonds could undermine the central assumption underpinning most multi-asset portfolio construction models i.e. that the interest rate duration inherent in government bonds will protect against equity losses.

As Goldman Sachs points out, in relation to typical government bond / equity balanced portfolios:

“A 60/40 portfolio had one of the largest drawdowns since the 1960s this month. This was due to the sharp equity drawdown but also as there was less of a buffer and diversification from bonds.

… In addition to the sharper-than-normal equity correction, diversification in 60/40 portfolios has been less good. First, with bond yields at all-time lows now and close to the effective lower bound, there is little space for most DM bonds to buffer equity drawdowns. In other words, the beta of bonds to equities has declined, especially in Europe and Japan. But also equity-bond correlations turned positive in most markets”

- Goldman Sachs, ‘The 60/40 Drawdown and Multi-Asset Portfolio Risk’, Mar 2020

We have covered these themes before here and here.

Given monetary policy has already gone ‘all in’ and given the avalanche of new government bond supply coming to fund all the promised fiscal stimulus, government bond markets now face the base case scenario of outsized price volatility relative to their meagre returns and the tail risk scenario of future inflation spikes imposing crushing losses on long duration bond exposures.

That is unless central banks everywhere can impose Japan-like control, but with the starting point of government bond yields now at multi-century lows, you’re really not getting paid much to take that bet.

The takeaways here are not binary. It’s not about which way bond yields will move from here or whether future inflation will be higher or lower. Nobody can reliably predict these things.

For multi-asset portfolios, it’s about a nuanced re-assessment of how government bonds are expected to behave, an objective scrutiny of how reliably they can continue to play their defensive role and balanced consideration of the tail-risk scenarios that might play out from the unprecedented policy actions being implemented.

What does all the fiscal stimulus mean for government bonds?

Governments everywhere have launched a blitz of stimulus measures, the speed and scale of which is astounding. Of course all this fiscal stimulus, which in aggregate is of a magnitude that is unprecedented outside wartime, means governments need to borrow more money by issuing lots and lots of new bonds.

Investors have become used to reflexively reaching for the interest rate duration inherent in government bonds as THE hedge of choice for equity risk, implicitly assuming that highly rated government bonds are by definition a ‘safe haven’.

It’s now prudent to reconsider those assumptions in light of the following factors, which in combination are driving a stark paradigm shift for government bond markets:

Demand / supply imbalance

The obvious question is how well bond markets can absorb the vast amounts of new government bond supply that is coming. Recall that when Japan was ramping up its government spending, on its way to becoming the most indebted developed economy in the world, it had a giant domestic pension savings pool to absorb it.

We are now about to see rapidly rising government debt levels at a time when ageing populations in the western world are transitioning into retirement and drawing down their retirement savings. This may mean less demand from pension savings pools to absorb all those new bonds.

Lots of new government bond supply, at record high prices, isn’t an ideal combination when demand may be waning.

Government debt concerns

Rapidly rising government debt levels will eventually focus attention on the state of government balance sheets and sovereign credit risk. This will be more of an issue in some countries than others and is highly contingent on the severity/duration of the economic disruptions to come.

Lower bound for rates

With cash rates in most developed economies now effectively at the lower bound (i.e. near or even below zero) and a growing acceptance of the unsavoury side effects of negative rates, (details here) the single biggest tail wind for government bond markets – central bank rate cuts – is now pretty much done.

We’re at such extremes now that basic principles become binding constraints … for bond prices to keep going up, yields need room to keep going down. Bond yields could go negative everywhere, as they already are in Germany and Japan, but that’s harder with negative rates falling out of favour.

Inflation tail risk

The current consensus view is that inflation is dead forever. This view may be tested by the unprecedented combination of massive fiscal stimulus + ultra-loose monetary policy + risk of supply side production disruptions, that we now have.

Given the ultra-low starting point of bond yields, an unexpectedly rapid rise in future inflation would be very damaging for bond markets.

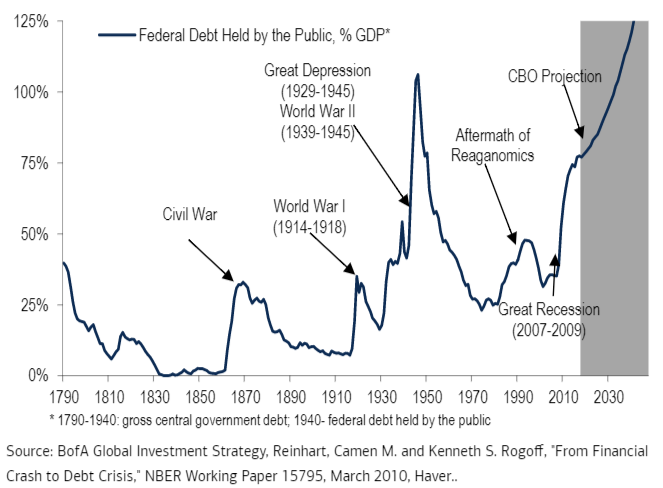

To put things in perspective, the chart below shows how large the government debt burden will become for the US alone. The same dynamics are set to play out in globally, to varying degrees.

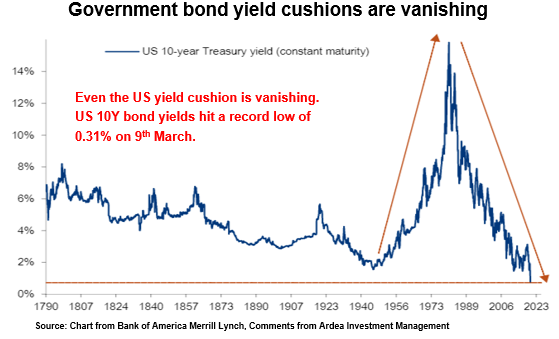

And this all happening at a time when the yield cushion that protects against the duration risk inherent in government bonds is extraordinarily low. Even in the US, where the FED managed to rebuild a modest yield cushion by raising rates in 2018, yields have dropped all the way back toward zero. (refer here for an explanation of yield cushions).

Combining all these factors, price sensitive bond investors will eventually demand more of a risk premium (i.e. higher bond yields) in return for taking the duration risk inherent in government bonds. Remember, even with central bank cash rates anchored at zero, longer dated bond yields can still rise and we already saw early signs of this in March:

“Global bonds plunge on fear of debt deluge from pandemic defence. European sovereign bonds led a global rout as markets braced for the kind of supply surge not seen for years, after nations from the U.K. to France and Italy unveiled plans to spend their way out of the coronavirus crisis.

Investors are pricing in the risk of a surge in government borrowing to fund stimulus aimed at offsetting the economic shock from the pandemic.”

- Bloomberg News, 18th March 2020

Fighting against all this is and the potential saviour of government bonds is one group of enormous price insensitive buyers … central banks.

Thus, we’re set up for a 3-way showdown between the governments, who will be dumping more and more debt onto government bond markets, the private investors, who will demand higher risk premia to keep buying all those bonds and the central banks, who will need to be the buyer of last resort to prevent a violent re-pricing of bond markets (i.e. higher yields / lower prices).

What’s the end game?

Japan provides a blue-print for the benign (at least so far) end game scenario.

Despite enormous government debt, the Bank of Japan (BOJ) has successfully kept bond yields under control via aggressive market intervention. While there is much criticism about the longer-term merits of their approach, the fact remains the BOJ has been able to keep bond yields pinned at extraordinarily low levels, while facilitating very large amounts of government bond issuance.

The question then becomes, can the Japan experience be repeated everywhere else, all at once?

Whether it’s the right approach or not in the long term, central banks will certainly try very hard to keep government bond yields pinned down. Otherwise, if bond yields were to rise a lot, at a time when inflation expectations remain subdued, the resulting increase in real yields would effectively represent a monetary policy tightening. That’s the last thing they want when governments are frantically deploying fiscal stimulus to prevent a prolonged recession.

A longer-term consideration is that when central banks aggressively intervene in bond markets, bond prices lose their information value, as we have already seen in Japan.

Bond market pricing normally acts as a disciplinary check on the actions of central banks and governments. For example, if monetary policy is too loose and inflation risk is rising, or if government borrowing is becoming unsustainably high, bond markets will reflect this via the risk premia incorporated in pricing.

Aggressive central bank intervention dampens these pricing signals, which means inflationary pressures, unsustainable debt levels etc. can continue building up without any market based disciplinary check. It’s therefore then left entirely up to central bankers and governments to control themselves.

How confident can we be that a small group of powerful policymakers with little real-world accountability, can walk the delicate balance between too much or too little policy stimulus?

Of course the policymakers would like us to believe very confidently in their abilities.

Back in 2015, BOJ governor Kuroda began a policy speech explaining the BOJ’s extreme monetary policy stance by invoking Peter Pan:

“I trust that many of you are familiar with the story of Peter Pan, in which it says, ‘the moment you doubt whether you can fly, you cease forever to be able to do it,'”

As monetary policy increasingly reaches its limits, and as some argue, with little results to show other than rampant asset price inflation, the power of central banks becomes increasingly reliant on markets continuing to believe in their narratives, rather than the concrete positive impacts of their actions.

‘I believe I can fly’ might be confidence inspiring to some but sounds delusional to others. In that same vein, many of the consensus narratives around central bank omniscience and omnipotence will now be severely tested.

The ultimate test of belief in central bank credibility may well be the end game we are heading for – debt monetisation.

This seemingly innocuous technical term is in fact loaded with all kinds of scary connotations as it refers to the controversial idea of central banks explicitly financing government spending by printing money to absorb extreme levels of government bond issuance that markets wouldn’t be able to digest (at least not without yields rocketing higher).

This is controversial because of the fear that it could eventually lead to economic carnage via hyperinflation, sky high interest rates and loss of confidence in currencies a la Venezuela, Zimbabwe etc.

A recent paper co-authored by former FED vice chair Stanley Fischer argues that ‘unprecedented policy co-ordination’ will be needed to fight the next economic downturn. Recognising the risks of outright debt monetisation, the authors advocate a middle path of fiscal and monetary policy co-ordination that mitigates these risks. While that sounds fine in theory, in practice it requires policymakers to manage an extremely delicate balance in engaging extraordinary stimulus measures, while still maintaining a credible narrative around inflation and budget deficit control.

Such narratives only hold as long as the majority thinks that the majority still believes in them. Once that belief is questioned a dramatic paradigm shift can occur. The early warning signal will be a modest but sustained increase in longer dated bond yields. Initially it will be subtle enough that most won’t notice (aside from the bond vigilantes), but then it quickly gains momentum as confidence in the prevailing narratives crumbles.

Stay on top of fixed income markets

We believe that accurate and transparent risk measurement is fundamental to making intelligent investment decisions and producing the anticipated return outcomes. Never miss a Livewire insight by hitting the 'follow' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gopi Karunakaran is Ardea’s Co-Chief Investment Officer (Co-CIO), together with Ben Alexander. In this capacity they both share responsibility for overseeing the investment process and investment team, with ultimate accountability for ensuring the performance of all portfolios is consistent with client objectives.

Gopi has +20 years’ experience across global fixed income markets, including the full spectrum of global interest rate and credit markets, as well as broader macro relative value investing across equities, FX and structured products.

Featuring

Gopi Karunakaran,

Ardea Investment Management

Gopi Karunakaran is Ardea’s Co-Chief Investment Officer (Co-CIO), together with Ben Alexander. In this capacity they both share responsibility for overseeing the investment process and investment team, with ultimate accountability for ensuring the performance of all portfolios is consistent with client objectives.

Gopi has +20 years’ experience across global fixed income markets, including the full spectrum of global interest rate and credit markets, as well as broader macro relative value investing across equities, FX and structured products.

Gopi Karunakaran is Ardea’s Co-Chief Investment Officer (Co-CIO), together with Ben Alexander. In this capacity they both share responsibility for overseeing the investment process and investment team, with ultimate accountability for ensuring the...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

How to invest $100k for growth

Livewire Markets

Equities

Morgans’ top large-cap picks for October 2025

Morgans Financial