For China, this Time is Different

Last month I wrote about how we are ten years on from the beginning of the credit crisis, but are seeing many of the same signs of hubris that were present then. There’s no reason to believe that this time is different, highly priced assets and easy credit are likely to correct in the medium term. However, one thing that is definitely different is the shadow that China now casts over the global economy. In 2008 China announced a massive stimulus package that helped its economy and the global economy weather the storm. But nearly ten years on, the situation is very different and China could shift from being a big contributor to global growth to an anchor slowing down the global economy.

The 2015 McKinsey report “debt and (not much) deleveraging” laid out how global debt levels have risen since the crisis. It highlighted three areas of particular concern; sovereign debt, consumer debt and China. However, as shown in the graphs below the growth in Chinese debt levels is drowning out progress made in other countries which have as a group reduced their debt levels. When China is excluded there has been meaningful deleveraging in global bank, corporate and consumer debt since 2009.

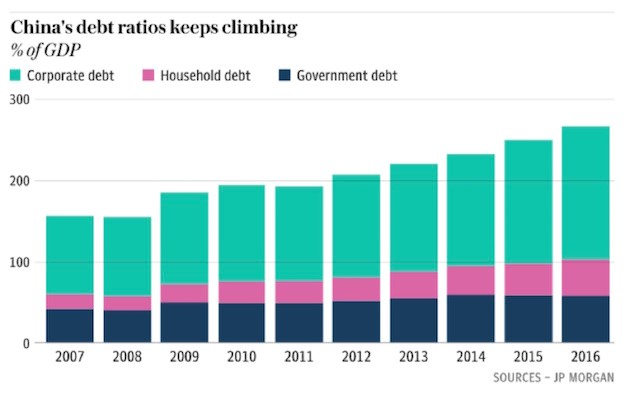

The next graph shows just fast China’s debt levels have grown in the last decade. In 2007, China had an above average level of debt for an emerging market. Roll forward to today and nobody talks about China’s debt levels in comparison to emerging markets anymore as it is so much bigger than its peers. Today people talk about China’s debt to GDP level as on par with developed economies, dismissing China’s substantially underdeveloped economic structures and financial markets. For an emerging market, China is carrying record levels of debt.

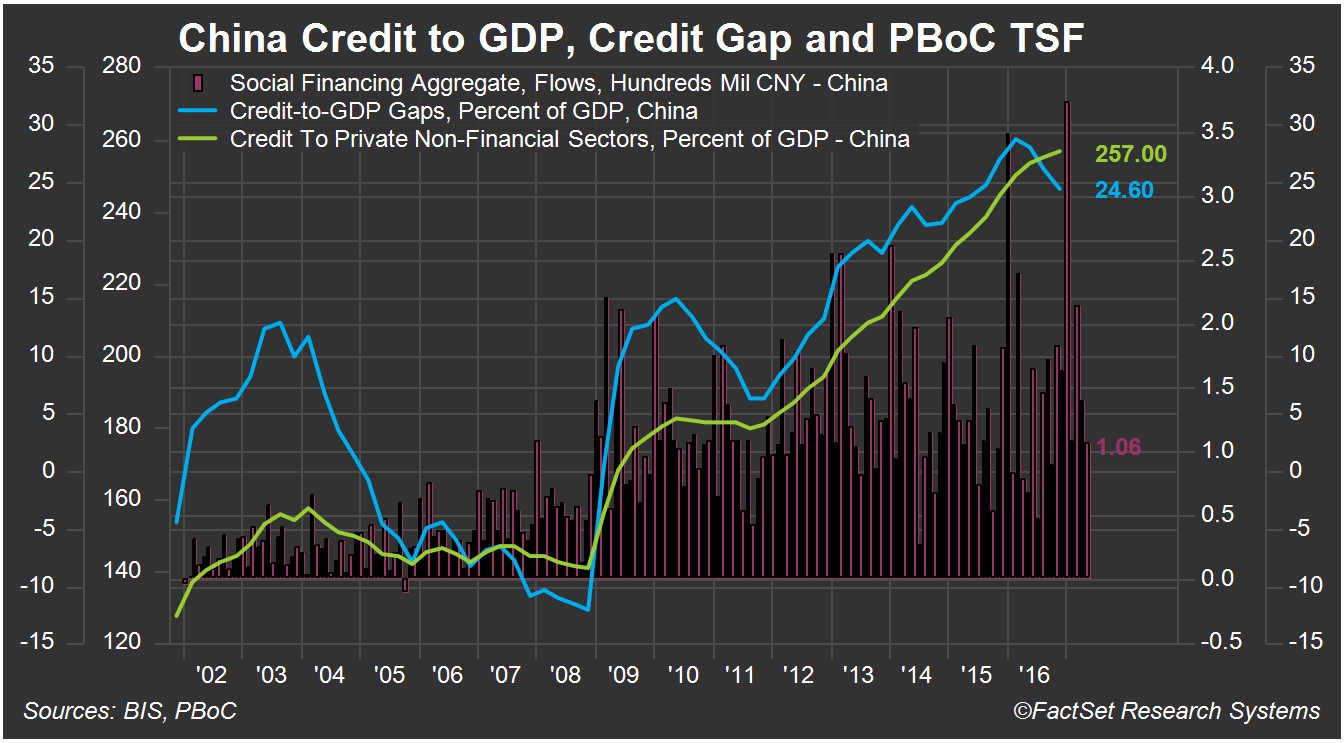

Another factor that makes China’s debt growth extraordinary is the pace and length of the expansion. Arguably the best indicator of future debt issues for anyone (corporate, individual or government) is when the debt is growing much faster than the income used to make repayments. When talking about an economy as a whole, the IMF measures this using the credit to GDP gap. The chart below is particularly busy, but concentrate on the blue line. It shows that China’s debt has been growing way above sustainable levels since mid-2013. To maintain its high levels of GDP growth, China has had to use an enormous amount of debt stimulus.

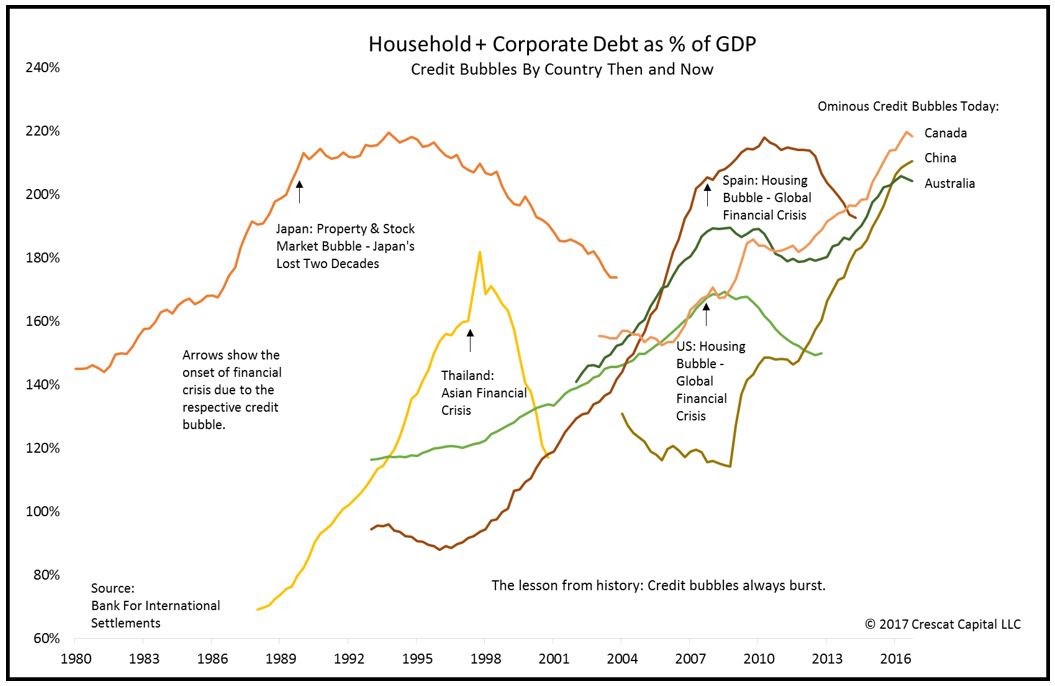

Further demonstrating how record setting China’s credit growth has been is the following graph. This chart excludes government debt, focussing just on private sector debt. Note the near vertical rise in China’s debt levels that mirror the experience of Thailand and Spain in the lead up to their credit induced bubbles. Note also the comparison with Canada and Australia, which are both frequently cited as having excessive household debt and house prices.

This time is very much different for China. No other emerging market has reached such extraordinary levels of debt. Chinese institutions and investors are mostly amateurs with a track record of investing in unproductive assets. Default rates are kept artificially low as extend and pretend lending is commonplace. A generation of investors have seen nothing but good times and only fear missing out on more. The potential for losses is given little consideration other than the expectation that the government will bail out everyone if losses occur.

It is now a question of when, not if for China. China’s government believes it can reduce leverage whilst maintaining high levels of growth but there’s no precedent for this. China’s companies have dominated their domestic markets due to trade barriers but have struggled overseas. China now appears to be hitting a limit on growth from exports as other Asian nations undercut it on price and developed nations fight back against its hypocritical stance on “free trade”. If credit growth stops China’s growth will stop, with recession a foreseeable prospect. Given the size of China’s economy and its outsized contribution to global GDP growth a reversal in China could see it export a recession to other countries. This time is different for China, but in a very bad way.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

4 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment