For want of a coffee can, we left $7 million on the table

Every so often, you find a story in a newspaper about a frugal living individual who had a modest paying job throughout their life, who everyone in their community thought was penniless, but who left a fortune to the local “dogs home”.

The most well-known example: Robert Read. Mr. Read, who died in June 2014 in Dummerston, Vermont aged 92, worked for many years at a service station, didn’t enjoy retirement, and so worked as a janitor at J C Penney. He combined frugal living with numerous visits to his local library – and buying stocks, which were kept in certificate form in a safe deposit box at his local bank.

In a sense, the safe deposit box is like a deterrent – it’s actually a pain to sell any of the securities as you have to go to the bank, take out the scrip and then physically deliver it to the broker. No blockchain CHESS settlements here.

Mr. Read’s portfolio was worth $8million on his death, with the main beneficiaries being his local library and local hospital. The portfolio contained 95 stocks, acquired over time, with the dividends largely reinvested.

It’s a great story, but you don’t see the timeline – he bought this stock at this time and it appreciated from X to Y. But we know the core tenets of what was at work: long term investing to gain the benefit of compounding, reasonably well chosen initial investments and a form of “dollar cost averaging” by reinvesting the dividend payments.

Investment advisers will often show you some fabulous theoretical examples, which of course are handpicked: buy CSL on the float, or Cochlear on the spin out from Pacific Dunlop. By and large, they are unrealistic because they suffer at the very least from survivorship bias, as well as “sales bias”.

What if I could show you a real life ten year plus example of what might have been from a publicly available portfolio of 13 securities? Where one went broke, one lost 98.5% of the investment and another over 83% - no survivorship bias.

Coffee can investing

Before we get to our real life story, a few pointers to this type of investing. This style of “buy and hold” is often referred to as “coffee can investing” – where you effectively put your carefully chosen scrip in a coffee can and leave it alone to compound over time. No trading.

Robert Kirby of Capital Guardian Trust seems to have been the first investor to write about this phenomenon in a partly academic manner in the Journal of Portfolio Management (Fall 1984 issue), easily found on-line. The four major points Kirby stresses are:

· the lack of transaction costs, which were far higher in the mid 1980’s than the present day - anybody remember the old 2.5% sliding scale;

· his coining of the phrase “active passive” – in other words, you do actually pick stocks (active), but you leave them to gestate for years (passive);

· the difficulty of selling such a product to anyone – it takes ten years or so to evaluate, and thereby makes evaluating an upfront fee to an adviser quite difficult; you can, of course, just do it yourself; and

· the big one: the presence of a “multi-bagger” – a security that appreciates many-fold in price amongst the portfolio, because you leave it to do so.

Kirby’s piece notes, when analyzing the portfolio of a recently deceased husband to add to that of his client – the surviving wife - that he had been piggybacking the buy recommendations, but paid no attention whatsoever to the sell recommendation. He simply bought $5,000 of each stock, tossed the certificate in a safe deposit box and forgot about it.

Let’s let Kirby take up the story:

“Needless to say, he had an odd-looking portfolio. He owned a number of small holdings with values of less than $2,000. He had several large holdings with values in excess of $100,000. There was one jumbo holding worth over $800,000 that exceeded the value of the wife’s portfolio and came from a small commitment in a company called Haloid; this later turned out to be a zillion shares of Xerox”.

There are two or three books about trying to find “jumbo sized return companies”; the best, in my opinion, is Chris Mayer’s “100-Baggers”. Chris is a portfolio manager for Woodlock House Family Capital and authored the book as an update to the 1972 Thomas Phelps manuscript “100 to 1 in the Stockmarket”.

More recently, in February 2020, Kevin Duffy of Bearing Asset Management has started an diary based around the concept. You can interact easily with both Chris and Kevin on twitter

Coffee can investing has an obvious application in the current environment. There is great logic in acquiring certain types of companies which have long term income streams, but where their main asset is currently closed, and which has resulted in a significant decline in the share price to levels well below the absurdities of late 2019 or early 2020. Clearly the company needs the requisite degree of liquidity or low debt to make it “through to the other side” and not be structurally challenged. Thoughts over the next few months are likely to move towards assessing a permanently changed environment arising from the COVID-19 lockdown measures. My most obvious coffee can holding facing this environment is Madison Square Garden Companies (NYSE: MSG), owner of one of the most famous venues in the world, the sports teams who play there (Knicks, Rangers) along with a multitude of other currently closed venues and attractions. You may have others – airports, toll road, casinos, impenetrable brands and the like.

Leaving $7million on the table: a real-life example

At my own expense, I want to illustrate the potential benefits of this style of investment on an actual portfolio from June 2009. I accept the starting date has the benefit of propitious timing – the All Ordinaries Accumulation index returned 168.6% over the period - but that should be seen against the fact that over half the portfolio was invested in a gold and copper exploration company.

This is learning a different way: what would have happened if we had done better, rather than a conceited brag of what we did and how we spent the money. I reckon it’s stronger and ,more meaningful.

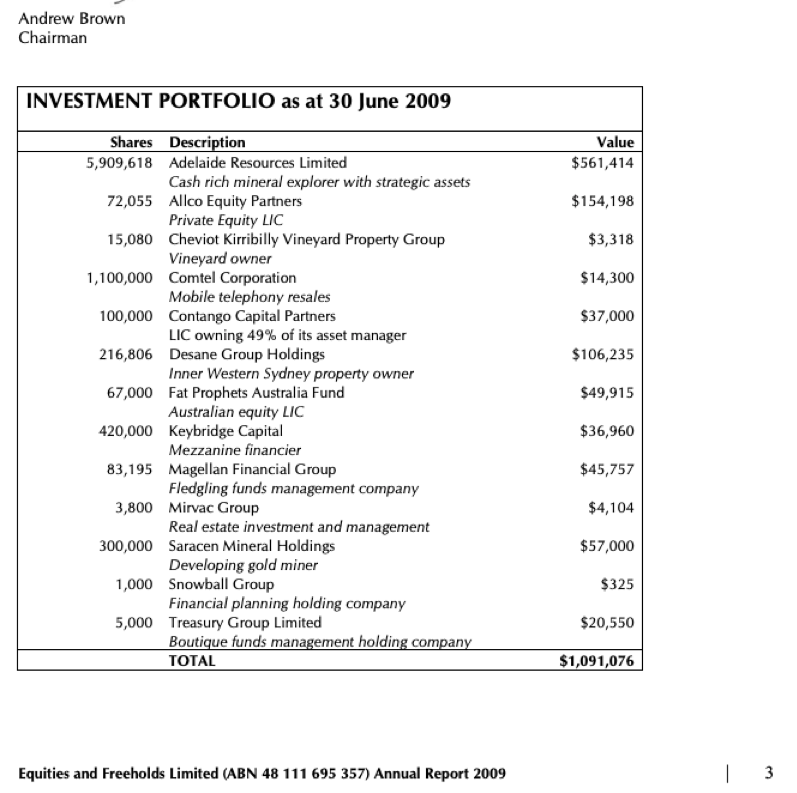

It would be quite amazing if many (indeed, any) of you had ever heard of Equities and Freeholds Limited (ASX code: EQF). I acquired control of the company, which was previously Goldlink GrowthPlus Limited in 2008. We encountered a few issues with the declines in equity prices arising from the GFC, returned capital to shareholders, found an interesting opportunity to acquire a significant stake in a mineral explorer (Adelaide Resources Limited, now Andromeda Metals) at below cash backing and started to invest in “discount to asset” situations.

By 30 June 2009, we had a portfolio worth just under $1.1million; with other assets and liabilities broadly offsetting each other, the $1.1million was broadly the NTA.

From there, we distributed the shareholding in Adelaide Resources as a capital return, introduced a new set of shareholders via an 8-1 rights issue, liquidated the portfolio, and I retired to the sidelines. The company eventually morphed into the currently listed financial advisory group Easton Investments Limited (ASX: EAS).

Most people would think it was impractical to run a $1.1million portfolio of 13 stocks in an ASX-listed company. But what if we had stayed the course, put the holding statements in a coffee can and left them alone to gestate, rather than doing a back-door listing transaction?

Here’s the snapshot of page 3 of the EQF annual report for 2009 containing the portfolio:

Of the 13 securities in the portfolio, one went broke (Cheviot Kirribilly) and four were (effectively) taken over (Allco, Comtel, Contango and Snowball). A few were very disappointing. But the whole essence of this style of investing is that if you choose carefully, there is a real chance of leaving a multi-bagger alone to gestate, like Kirby’s client’s Haloid holding.

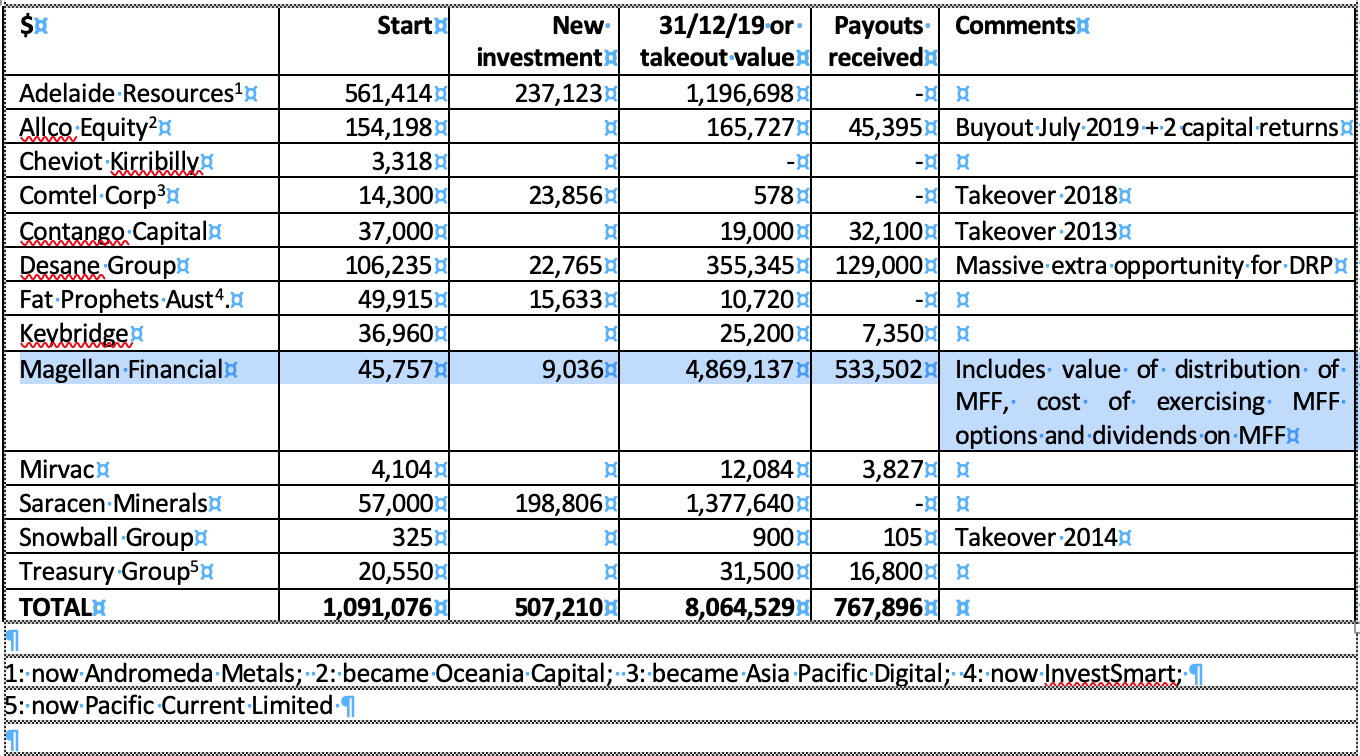

The analysis which follows simply assumes that we took up entitlement issues for each company (good or bad) but did not reinvest dividends where available. That actually disadvantages the analysis quite severely. There is no adjustment for the time value of money, nor for expenses which would be incurred in running a small ASX company.

Between 30 June 2009 and 31 December 2019, we would have been required to invest a further $507,219 into the portfolio; however, the capital value of the portfolio would have grown from an effective $1.6million ($1.1m base + ~$500k new investment) to $8,064,529. We would have also received dividends and cash capital returns of $767,896.

What drove this performance from a motley-looking selection of investments? The table below shows four differentiated but very successful investments made possible by patience – not touching:

Magellan is obviously the star performer, with an investment of less than $55,000 yielding $5.4million in capital values and dividends including the Magellan Capital Investments (MFF) shares and options spin-off in 2013. However, even excluding this stellar performer, simply having Desane, Saracen and the more speculative Adelaide Resources provided a significant outcome, with a two and a half fold increase in capital value, and significant dividends.

Adelaide Resources is interesting in terms of the lifecycle of an exploration company. From a share price of 9.5c in June 2009, the company traversed the highs and lows of 17c and 0.4c at various stages. Having belief – which is, of course, suspended in the coffee can environment – and taking up rights issues at 0.8c and 0.5c per share with attaching options, was clearly the key.

Note the differences: Saracen the (project) acquisition driven gold miner never paying a dividend, versus Desane, the street smart property developer paying significant dividends, many of which could be reinvested, which would have massively additionally boosted the return.

Excluding expenses and interest costs, each of EQF’s 2,910,506 thinly traded shares would have seen their NTA move from $0.37 to $2.86. That’s over $7million of value not realised – for want of a coffee can.

However, EQF is like the 2005 movie “Batman Begins”. There’s a sequel which is much better…

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 40 years experience as on the buy-side, sell-side and corporate investing. Andrew currently runs East 72 Dynasty Trust, a unique long only wholesale trust investing in companies which are controlled by single shareholders or a close-knit group, usually families.

1 topic

4 stocks mentioned

Andrew has over 40 years experience as on the buy-side, sell-side and corporate investing. Andrew currently runs East 72 Dynasty Trust, a unique long only wholesale trust investing in companies which are controlled by single shareholders or a...

Expertise

Andrew has over 40 years experience as on the buy-side, sell-side and corporate investing. Andrew currently runs East 72 Dynasty Trust, a unique long only wholesale trust investing in companies which are controlled by single shareholders or a...

Expertise

Comments

Comments

Sign In or Join Free to comment