From 'made in China' to 'created in China'

Amit Lodha

Fidelity International

I spent the last week in China attending Fidelity’s autos and industrial trip for analysts and portfolio managers, as well attending the Credit Suisse China Conference in Shenzhen. It was an interesting week to be in China, the week after the National Congress, and I have come away with an overriding view – China is well on its way to morphing from the ‘Factory of the World’ to ‘Laboratory of the World’.

Let’s start with the big picture…

Macro

The macro seems fine (famous last words…) and the government seems to have so far managed a soft landing. There is tightening in the property sector but, in my view, China is still a manufacturing giant compared to the rest of the world, and when economic growth is fine in Europe and the US, there is little to worry about here.

The consumer sector seems to be chugging along just fine too - look at the growth in Chinese Amazon - Alibaba’s revenues last quarter! Yes, recent auto/truck/elevator and property sales have been a bit weaker than expected and things seem to be slowing down at the margin, but that is to be expected given the pace of past growth and the slowing of money supply. Overall the government and central bank seems to be in control of the bad debt issues (higher resource prices = lower bad debts) though debt de-leveraging and demographic challenges remain on the horizon.

Post Congress there has been a significant change in party posts and leaders across the organisation structure. Unlike in the West, where a new CEO typically means kitchen sinking in year one, typical new leaders of various Chinese provinces want to make sure that things do not deteriorate significantly in the first year of their tenure as it ‘looks bad’ on their resume. So growth in 2018 is likely to be fine, as long as the government wants it to be.

Politics

This is the Xi Jinping era. China has had three eras, namely Mao, Deng and now Xi. Xi (unlike someone like Hu JinTao), wants to leave a legacy. He has also consolidated his position and power. The cabinet allocations are still unclear and need to be watched closely for future policy direction. In addition, there is no succession plan to Xi, which is a departure from the past and a risk for the medium term. The clear goal is restoring China’s place as a ‘Great and responsible world power’ - in a nutshell this also means for the Chinese to take pride in being from China.

So what do we as investors need to consider?

1) Environmental regulation/capacity controls - Two years ago when the government seriously talked about new environmental regulations and capacity controls, no one believed them. Now there seems little doubt that the government is serious, with anecdotes circulating of steel executives being jailed for not closing blast furnaces and 110 million ton of capacity being shut down over the last two years (for context this is about the same as total US steel production). This has significant implications across the materials/petrochemicals complex as lower Chinese capacity growth would suggest better supply/demand equilibrium.

2) There is significant over-capacity in Chinese autos (40mn capacity in 28mn market) - however, the government is strict on regulation. Phasing in Beijing 6 (like EURO 6) on trucks will lead to a demand for 3 million replacement trucks over the next 3 to 4 years (though the exact timing is uncertain). It was also clear that if the government achieves its goals, China will in the next 3-5yrs become the largest electric vehicles market in the world. There is significant innovation and development in the supply chain and there are some exciting opportunities for stock picking here but global companies also need to beware of the amount of capital that is being put behind this innovation.

3) ‘Made in China’ - This concept is well known, but the rapid pace of improvement in local Chinese quality continues to impress. On previous visits, I could easily tell the difference between a locally produced Chinese car and a western one. It is getting increasingly tougher. Most local Chinese brands (not only autos) have recruited western designers. The same is true across the manufacturing chain, though there remain pockets where Western companies still lead the way.

4) Rise of Chinese domestic brands - This extends to Chinese brands. The younger generation is less likely to buy a western brand blindly like his or her parents, and loyalty is only as good as your latest innovation (Apple is still aspirational but the local Chinese mobile brands are the rising 2nd tier leaders). Further localisation and personalisation continue to increase in importance. This trend of the rise of domestic Chinese brands is something we need to focus on in all the consumption segments (staples, discretionary, autos etc.)

5) Technology - This probably was the biggest eye opener for me. What has been achieved in the last few years in China in technology and innovation is simply breath taking. I used Chinese apps during the course of the week including- the easy Didi service app for transport, seamless payments through Alipay, and watched the locals exchange through WeChat QR codes rather than business cards. Technology permeates every corner. I did not use cash once in my travels!

However, making the valuations work for any of these technology companies is difficult and there is significant froth in the tech/fintech IPO market.

Spending a couple of days in Shenzhen was interesting. Shenzhen used to be where you could go to buy cheap Rolex rip-offs. Now it is the test bed of innovation. Most electronic prototype testing now happens here and, just like Silicon Valley, there is a significant ecosystem effect at work. As an example, we met with the co-founder of a car start-up NIO (backed by Tencent/Sequioia which has gone from start-up concept to a model in production (by March 2018) under the space of 3yrs (see the impressive videos here (VIEW LINK) & below. Their motto is ‘blue sky here’ and actually through most of my trip, China had blue skies.

Looking at the bigger picture, this means that all western companies either need to have development centres in China or ears to the ground to decipher what could out-innovate them.

Lastly, the problems of proposed regulation that we see with western tech companies, such as Facebook and Google, are not an issue as Alibaba, Baidu and Tencent closely partner with the government. However this is an area where, as they become bigger, regulation may make an impact.

What does this mean for investing in China?

Overcapacity, poor capital allocation and questionable corporate governance have made it difficult for many of us quality-biased investors to invest (v/s rent) in Chinese stocks beyond the internet names such as Tencent, Baidu and Alibaba. We have therefore tried to play Chinese growth through western companies. At the margin, I think this is changing.

Environmental control and the debt issues have reduced capacity additions across a range of sectors. They have also led to consolidation in industries the pace of which is only accelerating. State owned enterprise reforms have led to a number of companies putting in place stock option plans leading to some semblance of corporate governance coming through. Destruction of wealth through expensive international acquisitions (due to anti-trust concerns) are also less likely.

So you have consolidating industry structures, reduced capacity additions with improving corporate governance and a level of innovation from and within China that is astounding. Happily for me, there are some strong management teams operating here too.

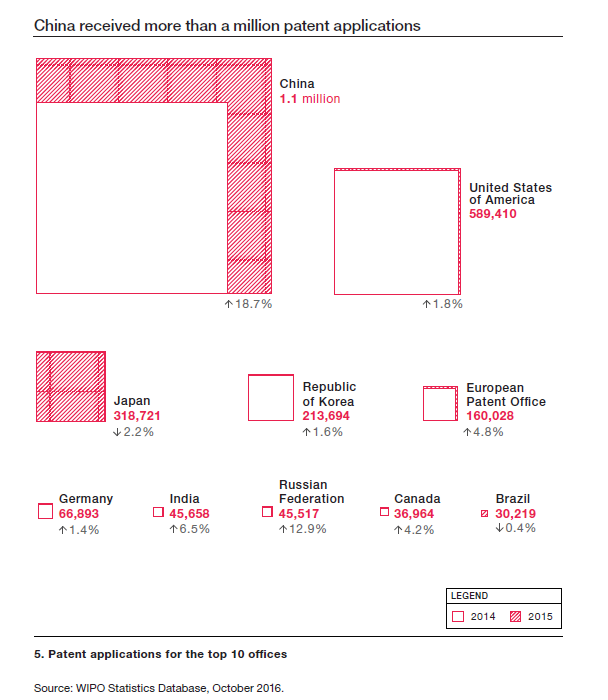

It does seem that the World’s Factory is morphing into the World’s laboratory (see the chart on patent applications below). This points to some interesting stock picking ideas – and that certainly piques my interest!

For further insights from Fidelity International, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Amit Lodha has been Portfolio Manager of the Fidelity Global Equities Fund since 2010 and has over 16 years of investment experience. He is a qualified accountant from the Institute of Chartered Accountants (India) and a CFA charterholder.

1 contributor mentioned

Amit Lodha

Portfolio Manager, Global Equities

Fidelity International

Amit Lodha has been Portfolio Manager of the Fidelity Global Equities Fund since 2010 and has over 16 years of investment experience. He is a qualified accountant from the Institute of Chartered Accountants (India) and a CFA charterholder.

Expertise

Amit Lodha

Portfolio Manager, Global Equities

Fidelity International

Amit Lodha has been Portfolio Manager of the Fidelity Global Equities Fund since 2010 and has over 16 years of investment experience. He is a qualified accountant from the Institute of Chartered Accountants (India) and a CFA charterholder.

Expertise

Comments

Comments

Sign In or Join Free to comment