Going overseas for income

The underperformance of Australian equities in the last year has highlighted the importance of diversifying globally for all Australian investors, not only to seize opportunities but to avoid being overexposed to local risks. However, we believe most Australian SMSF investors have very low allocations to international equities, particularly relative to the average large superannuation fund.

Why is that?

Home bias

In spite of the diversification benefits of investing in foreign shares, it seems investors have a tendency to over-invest in domestic market. This home bias is likely due to two reasons; firstly that people tend to invest in what they know, and secondly, because of the perceived difficultly and associated costs with accessing the global market.

Tax

Investments in Australian shares can carry valuable franking credits. The franking credits on the Australian S&P200 index for FY2016/17 were worth 1.4% in returns for a pension phase superannuation fund which receives a full refund of those franking credits. For a pension fund, this meant Australian shares returned 5.7% for FY2016/17. On the other hand, investments in overseas shares can often be subject to foreign government withholding taxes which can reduce the dividends and thus total returns that investors receive.

Income

Australian shares have delivered higher dividend yields relative to global shares in the past. For example, Australian shares yielded 5.7% inclusive of 1.4% franking in FY2016/17 whilst global shares yielded just over 1.9% after withholding taxes. From an income perspective, Australian shares appear to be more attractive than global shares. However, we believe it is possible to generate similar levels of income from global equities if a fund is actively managed for income

Australian equities: Consider the risks

Focussing on domestic shares makes sense at a number of levels, but it could result in missed opportunities, as well as increased exposure to significant risks.

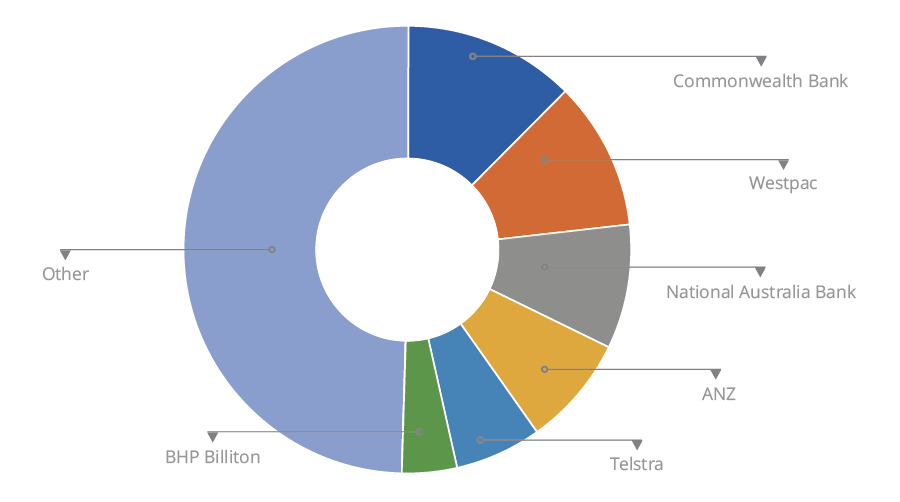

Chart 1 - Top dividend payers in the S&P/ASX200 in FY2016/17

Source: Plato, Iress

The chart above highlights the concentrated nature of the Australian equity market. Of the 200 stocks in the S&P/ ASX200 index,

the top six stocks represented over half the total gross dividend income in FY2016/17.

With the four big banks currently representing approximately one third of that dividend income, if a banking industry incident were to occur, this could seriously impact the total dividends paid on the Australian share market, and in turn the income received by the average SMSF.

Therefore, income-focused SMSF investors should consider high-yield global share offerings to not only generate income streams, but to also diversify away from the $A, particularly those in pension phase.

The benefits of high-yield global share offerings

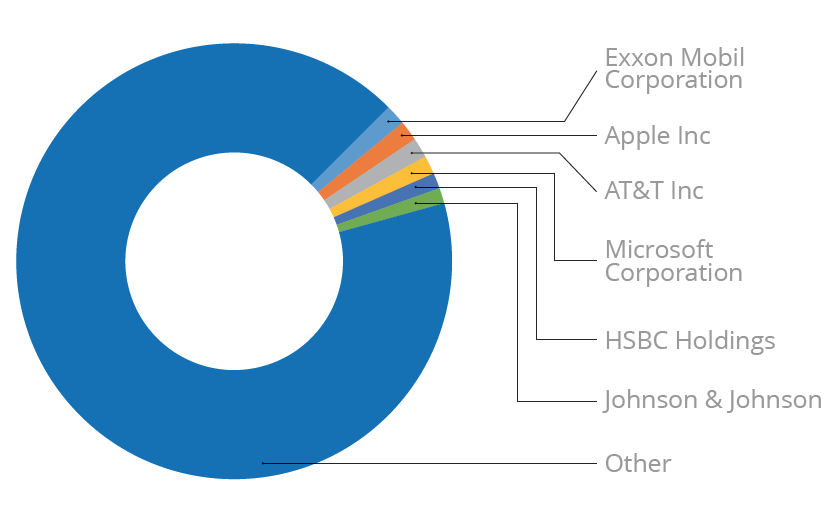

To provide a contrasting measure of how concentrated the Australian equity market is, we calculated the dividend composition for a global equity index, depicting the top six dividend paying stocks in the MSCI World ex Australia in FY2016/17.

Chart 2 - Top dividend payers in the MSCI World ex Australia in FY2016/17

As shown in Chart 2,

the top six stocks represent less than 10% of the total dividends of the global index in FY2016/17,

and the make-up of those top six stocks is far different to Australia’s top six stocks. The top six reflect globally recognisable brand names in industries such as energy, electronics, software and telecommunications.

It is evident that the income derived from the global index is likely to be more diversified, and therefore not dominated by a single industry in a single geographic location, like the Australian banking is to the Australian index.

For further insights from Plato Investment Management, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006.

Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street Global Advisors, responsible for over $10B in active and enhanced equity investments. Earlier he held various positions at Westpac Investment Management, including Chief Investment Officer, Head of Equities. During his time at Westpac he was also instrumentally involved in the mergers of BT and Rothschild.

Don has a strong interest in responsible investment and governance. He has a PhD in Finance and a Bachelor of Commerce with First Class Honours from UQ, and a University Medal.

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006. Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street...

Expertise

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006. Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street...

Expertise

Comments

Comments

Sign In or Join Free to comment