Good quality REITs can add income and relative stability to investors’ portfolios

The Real Estate Investment Trust (REIT) sector – previously called the Listed Property Trust sector – has always been a popular sector with Australian retail investors and currently comprises 7% of the S&P/ASX 300 Index. In this lesson we discuss what we have always believed are the most important aspects to focus on when selecting the appropriate REITs for IML’s portfolios.

While good quality commercial properties have done well over the last few decades there have been periods in the last 20 years when investors in REITs have suffered significant losses.

So how does one go about selecting the right REIT to minimise the chance of large capital losses or disappointments in future?

Firstly, we need to look at the different classes of commercial real estate that are held by most REITs to understand the dynamics of the sector:

Retail

Retail property consists of different types of property but namely:

- ‘flagship’ shopping centres such as those owned by Scentre Group which owns properties like Westfield Bondi Junction and Pitt Street Mall.

- regional shopping centres owned by the likes of Stockland and Vicinity which owns assets such as Bankstown Central in Sydney and tend to house the big chains such as discount retailers like Target and Big W.

- neighbourhood shopping centres – which house a local Woolworths or Coles supermarket with a few specialty stores – these are run by companies such as Shopping Centres Australia (SCP) and Charter Hall Retail (CQR).

Historically retail property has been a rewarding place to invest in, however the increase in the popularity of online retailing means that investors have to be very selective when investing in this segment.

Office

Compared to retail, office space is a more commoditised type of property as tenants tend to have less loyalty to a specific city location. When rents are very high, the supply side tends to surge - although there is generally a time lag before new supply impacts the market.

The office market overall tends to go through cycles of oversupply and undersupply, depending on economic conditions and the construction cycle – as discussed later in this article.

Industrial

Industrial properties are primarily logistics warehouses. Historically these assets have been viewed as the lowest quality property class because the ‘sheds’ can often be easily replaced, and they often have single tenant risk – meaning the income can go to zero if a tenant moves out and they cannot be replaced.

So what are the most important attributes and risks that IML considers to decide which REITs are worth investing in?

Good quality, recurring earnings

It is important to understand that while most REITs earn their income from the underlying rents received from the properties that they own, this is not the case for all REITs.

Some REITs make part of their income from development divisions that they operate – for example Mirvac (MGR), Stockland (SGP) and Goodman Group (GMG) all operate development divisions where they buy sites, construct buildings and then sell the final product to an end user. These development profits currently now represent 47%, 39% and 40% respectively of MGR’s, SGP’s and GMG’s profits.

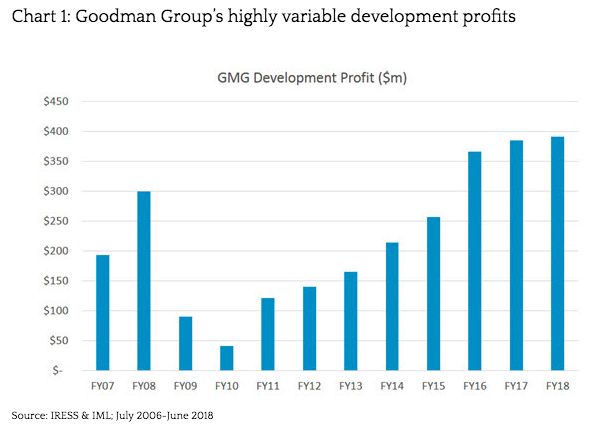

Chart 1: Goodman Group’s highly variable development profits

As can be seen from chart 1 Goodman’s Group’s development profits in the last few years have risen from around $120m in 2011 to nearly $400m in the latest results – a substantial 40% of Goodman’s net operating income for FY18.

Of course if market values rise between the time of site acquisition and the final sale, then a good profit will be made. However, if the market value of property declines between acquisition, construction and the sale, then the profits will be much lower - and this part of the business can actually swing into a loss. In fact in the aftermath of the GFC, Goodman Group, Mirvac and Stockland all recorded large losses from their development arms and all had to cut their distributions substantially.

Given the elevated state of property, we are currently very cautious on any REITs which make large profits from their development arms, and instead focus on those which earn stable income from rental payments from good quality, long-term tenants.

Long WALE

The WALE is the ‘weighted average lease expiry’ which measures the average length of the leases in any property and is measured in years. Clearly a longer WALE is generally more attractive because it gives the property owner certainty over the rental income for a longer period.

At IML we have always generally liked REITs which have longer WALE’s particularly when the lease is with an A rated tenant like Woolworths or Coles.

A good example is Shopping Centres Australasia (SCP) which has been a core holding of IML since it was demerged and spun off from Woolworths in 2013. SCP operates over 70 neighbourhood shopping centres all of which have long leases with Woolworths supermarkets, which is an anchor tenant in these centres.

Chart 2: Shopping Centres Australasia – steady, growing distributions per unit

Under the terms of the leases signed with Woolworths, rent is linked to the sales growth of the supermarket, and the WALE on these centres is almost 10 years – and thus we expect SCP to produce a very secure, growing income stream for shareholders for many years to come as can be seen from chart 2.

Low debt/gearing levels

Many REITs borrow money to fund part of their property portfolio as they seek to add value for shareholders by borrowing at a low fixed rate and using the money to own properties that have a growing income stream or by investing in properties where they can enhance the capital value.

While borrowing money to buy property may add value to a REIT, this can also substantially increase the financial risk of the REIT.

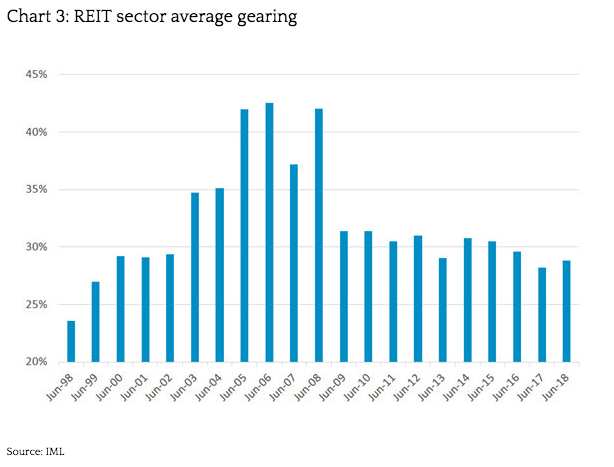

As can be seen from chart 3, In the period leading up to the GFC, average gearing levels in the REIT sector rose from levels under 30% to well over the 40% level as many REITs took advantage of the readily availability of credit pre-GFC to borrow heavily and acquire properties. As credit froze and property values declined during the GFC, many REITs were caught out holding too much debt forcing many to cut their distributions or undertake emergency capital raisings. Some REITs like Centro and Valad also filed for administration in this period.

Chart 3: REIT sector average gearing

IML has always preferred REITs with lower gearing levels and currently owns REITs such as Abacus and Bunnings Warehouse Property Trust whose gearing levels at 19.3% and 23.3% respectively are well below the average gearing level of the sector.

Favourable supply/demand dynamics

REIT investors also have to be wary of the supply /demand dynamics that may influence each particular property segments.

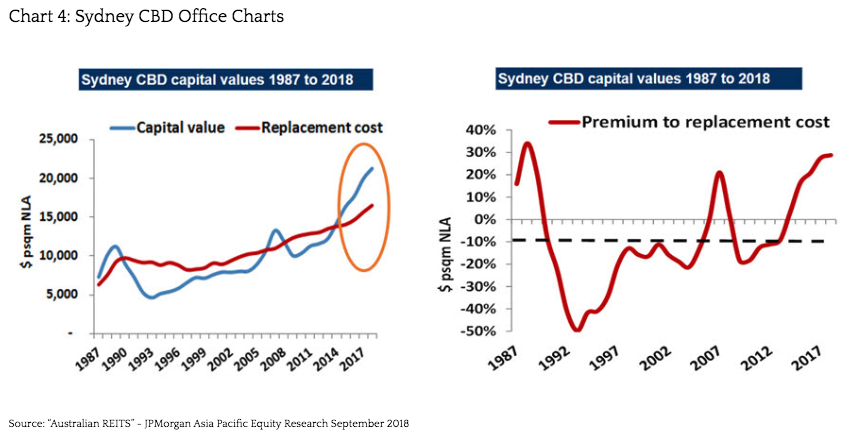

In recent years the key office markets in Sydney and Melbourne have performed strongly with office prices and rents rising substantially. However, as the charts below show for Sydney, the significant increase in the value of office properties over the last few years has pushed prices to well above the replacement cost of these buildings so that it is now cheaper to build a new office property than to buy an existing one. The Melbourne CBD market is also in the same situation.

Chart 4: Sydney CBD Office Charts

As the market value has soared above the replacement cost of CBD property, it is incentivising the construction of new office supply in both Sydney and Melbourne – in time, this will in our opinion, lead to office rents falling in both cities as new supply comes on the market in both cities.

Thus, at the moment IML is very wary of all property office trusts such as Dexus and Investa Office Fund and is not a holder of these REITs.

Sustainable dividend payout ratio

Due to a quirk in current accounting standards, REITs are not required to depreciate their property assets in the same way that industrial companies do. This means that if a REIT pays out all of its profits to investors, the REIT may find that it has insufficient cash left to maintain their assets.

At IML we pay particular attention to the cashflow statements of each REIT to ensure that all maintenance capex is covered by retained earnings of the REIT. We like to invest in REITs that manage their cashflows in a prudent way and where the distributions to shareholders are sustainable.

However, in the lead up to the GFC, where financial engineering was being encouraged and well rewarded by the sharemarket and with credit readily available and debt cheap, most REITs resorted to paying distributions out of unrealised gain. This is why during this time IML funds held almost zero REITs despite the sector being 10% of the ASX 300.

Thus in 2007, GPT, one of Australia’s leading REITs, was caught up in the excitement pre-GFC and resorted to financial engineering alchemy by paying distributions of $587m from only $487m of operating cashflow - representing a 120% payout ratio. GPT was not alone e.g. Macquarie Country Wide paid out 127% of their cashflow in distributions in 2007. It is no wonder that these REITs distributions were proven to be unsustainable and were cut severely during the GFC.

Price /NTA

Apart from all the many qualitative factors above to consider when selecting REITs for one’s portfolio, there is also then the question of what is a reasonable price to pay for any particular REIT?

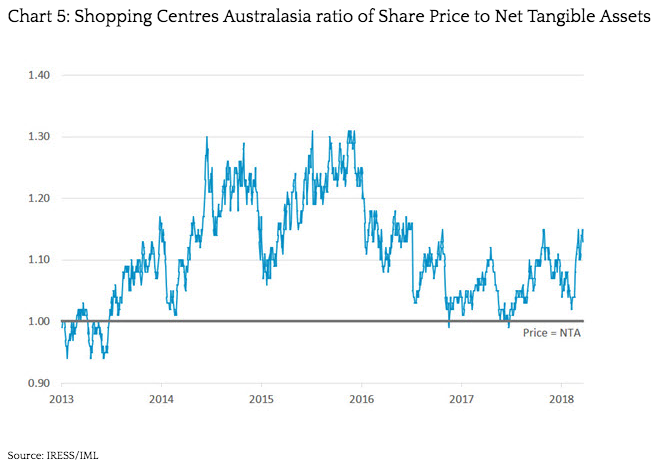

As mentioned in Lesson 12, the most commonly used way to value REITs is to look at the Price to NTA ratio – which compares the share price of the REIT to its net tangible asset backing.

Provided one is satisfied with the valuation and quality of the underlying assets, as well as the other qualitative factors discussed earlier, then using the share price to NTA ratio can be a good guide to when to buy a particular REIT.

The chart below plots the share price vs the underlying NTA of Shopping Centres Australasia (SCP), which we mentioned earlier. Following our in-depth research of the company, we are satisfied with the level of gearing, the long WALE and the low maintenance capex required to maintain the assets held. We are also satisfied with the recurring nature and quality of the cashflows generated from the properties held as well as with the conservative and experienced management team of SCP.

As such, since SCP was listed in 2013, IML has always been happy to top up our holding in this REIT whenever the trust has traded below or very near to its stated NTA - which happens from time to time – as shown in the chart.

Chart 5: Shopping Centres Australasia ratio of Share Price to Net Tangible Assets

Conclusion:

High quality tenanted real estate held in conservatively managed and well-structured REITs should produce fairly reliable distributions for shareholders over time. If carefully selected, REITs can enhance the income and stability of investors’ portfolios over time as well as produce reasonable long-term capital growth.

Did you enjoy that?

You can read more of Anton’s 20 lessons from 20 years of years of quality and value investing here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality and value'.

Anton arrived in Australia in the 1980’s and was soon drawn to the sharemarket at a time when high-flying entrepreneurs dominated the headlines. His passion for investing in the sharemarket has not waned and he continues to put his considerable experience and the important lessons learnt over the last three decades to mentor the IML investment team and to deliver to clients' expectations.

1 topic

2 stocks mentioned

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality...

Expertise

Anton Tagliaferro is one of Australia’s most highly respected value-style fund managers. Anton founded IML in 1998 with the purpose of creating a research-driven fund manager focused on building portfolios of companies that represent both 'quality...

Expertise

Comments

Comments

Sign In or Join Free to comment