Government bonds are still useful even at the zero lower bound

Chamath De Silva

BetaShares

There’s been a fair bit of commentary recently that because interest rates and yields are so low, government bonds no longer have a role in portfolios. The argument goes that because yields are near zero, they will neither generate returns nor offset equity declines and therefore shouldn’t be used and should be replaced by dividend payers, utilities, REITs, hybrids, etc. This is poor reasoning on a couple of grounds:

- If the safe haven has less ability to offset risk asset drawdowns, the prudent course isn’t to reduce the weight to safe havens and increase the allocation to risk assets. Instead, it’s simply best to face reality and accept a lower expected return for a given level of volatility/drawdown risk.

Many investors don’t want to accept that, but a refusal to acknowledge a global savings (and hence debt) glut and chasing yield/credit no matter the risk premium is how you get the massacre in credit products that we saw in March.

- Long-term government bonds can still provide excellent equity diversification benefits relative to cash, short-term bonds and bond composites in low or even negative yield environments if curves are relatively steep, as is the case now. What matters is not whether they can provide the same absolute equity drawdown offsets as in the past (they can’t), but how they compare to the next best alternatives.

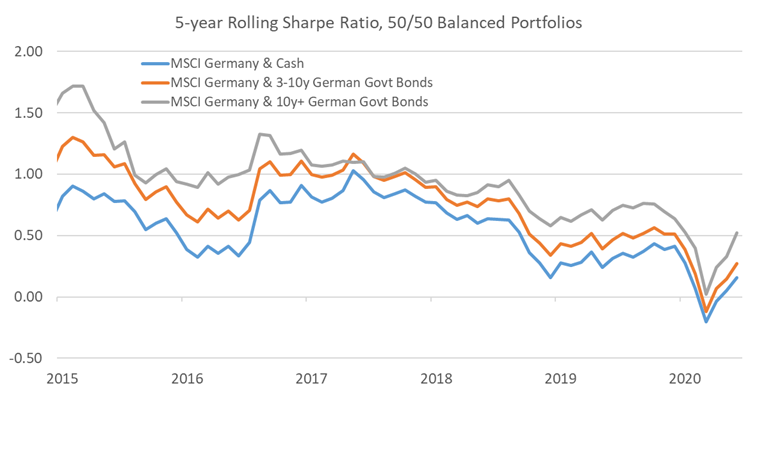

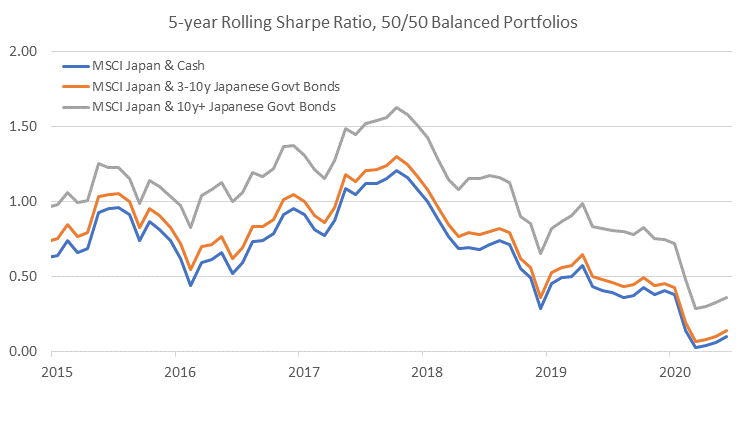

Below are 5-year rolling sharp ratios for German balanced portfolios and Japanese balanced portfolios. What it shows is that long term government bonds have consistently been better diversifiers than cash or shorter-term bonds, even in an extended period of negative interest rates. What ZIRP/NIRP and yield curve control (YCC) did was simply make shorter term bonds behave more like cash, with long-term government bonds becoming the only freely floating risk-off debt instruments. In bond parlance, risk-off = bull flattening in this environment.

In addition, YCC and liquidity support from central banks should continue to incentivise corporates to issue more longer-term fixed rate debt (with US dollar investment grade corporate bond issuance year-to-date already exceeding 2018 and 2019 issuance), increasing the duration contribution of credit instruments in broad composite benchmarks such as the Bloomberg Barclays Global Aggregate (as well as overall index spread duration), further undermining equity diversification of the most commonly used passive vehicles.

Chart 1: German balanced portfolios

Sources: Bloomberg, BetaShares Capital. Past performance is not indicative of future performance.

Chart 2: Japanese balanced portfolios

Sources: Bloomberg, BetaShares Capital. Past performance is not indicative of future performance.

Learn more

Stay up to date with all my latest insights by clicking the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Responsible for the portfolio management function and fixed income product development at Betashares. Previously, Chamath was a fixed income trader at the RBA, working in their international reserves section in Sydney and London.

........

This information has been provided by BetaShares Capital Limited (AFSL 341181; ABN 78 139 566 868). It is general in nature, does not take into account the particular circumstances of any investor, and is not a recommendation or offer to make any investment or to adopt any particular investment strategy. Future results are impossible to predict. Actual events or results may differ materially, positively or negatively, from those reflected or contemplated in any opinions, projections, assumptions or other forward-looking statements. Investing involves risk.

3 topics

Chamath De Silva

Portfolio Manager

BetaShares

Responsible for the portfolio management function and fixed income product development at Betashares. Previously, Chamath was a fixed income trader at the RBA, working in their international reserves section in Sydney and London.

Expertise

Chamath De Silva

Portfolio Manager

BetaShares

Responsible for the portfolio management function and fixed income product development at Betashares. Previously, Chamath was a fixed income trader at the RBA, working in their international reserves section in Sydney and London.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets