Are bonds as defensive as they used to be?

Many investors focus on the materially lower volatility in returns exhibited by fixed income securities when considering the potential diversification benefits when combining them with equities. Unfortunately, the equally important diversification benefits associated with the negative correlation of returns between the two asset classes can often be overlooked.

When focusing on this negative correlation of returns, it raises the question of whether, (in the last decade of financial deleveraging and low interest rates), bonds have maintained their diversifying characteristics during the periods when most needed. More explicitly the question of most relevance to many investors is whether bonds have continued to provide protection for equity portfolios during periods of heighted market risk?

To quantify the impacts, I used the CBOE Volatility Index (“VIX”) as a measure of market risk and the S&P/ASX 200 as the equity market measure. These were than compared with bond returns for both the Bloomberg Ausbond Composite Index return (“BACM0+”) and BACM0+ Duration-Matched Government Bond (“Dur-Matched Indexed”). The difference between the two bond indices is that BACM0+ includes credit exposures whereas the Dur-Matched Indexed is a Commonwealth Govt only return measure (same duration as BACM0+ but excludes credit exposures).

Prior to delving into the results regarding the behaviour of the correlations, it is important to address whether, in using the VIX, it is the equity market driving the movement in both bonds and the VIX or the VIX driving both equity and bond returns? To answer the question regarding the nature of any interlinkage between the VIX and bond returns it is necessary to take a closer look at the relationship after controlling for any interlinkage between equity markets and the VIX. Controlling for this interlinkage can be done via a two-stage regression analysis which effectively considers the VIX as an explanatory factor driving bond returns after stripping out its interaction with equities. The regression results from such an analysis do confirm that there is a significant and direct impact from the VIX on bond returns. Just as importantly, the coefficient from the analysis, as would be expected, is positive which highlights that the VIX and bond returns are positively related; i.e. increases in market risk are linked to higher returns from bonds.

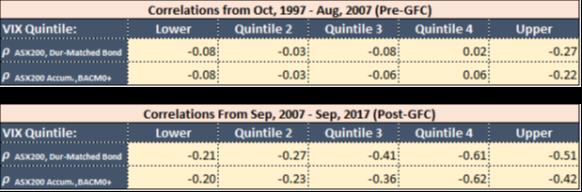

Having identified that the VIX, as a measure of market risk, does have a direct and positive impact on bond returns, the more important question to address is whether this relationship has changed over time. The methodology adopted to consider the strength of the relationship over different time periods is to divide the observations for the VIX into quintiles i.e. higher quintiles indicate higher levels of market risk. The relationship between equity and bond returns is then considered for each quintile of the VIX for the decade before and after the collapse of Bear Sterns in September 2007 (an event often considered to have signalled the start of the financial deleveraging cycle). The results of such an analysis are shown in the two tables of correlations below.

A consistent message from the analysis is that irrespective of the time-period there is an increasingly negative correlation between the returns on Australian equities and bonds as the level of market risk moves higher. The takeaway is that the diversification benefits from combining a bond portfolio with an equity portfolio increases as market risk increases. More importantly the magnitude of the negative correlations is greater in the decade post the collapse of Bear Sterns, an environment of materially lower interest rates, than in the decade prior to this. This supports the proposition that the lower level of interest rates witnessed post August 2007 did not weaken the negative relationship between bonds and equities. Indeed, the period of lower interest rates associated with central banks undertaking more accommodative monetary policy seems to have materially increased the level of diversification, or risk reduction, provided by bonds during episodes of heightened market risk.

Why bonds and equities retain their yin and yang

Despite what appears, on the ’face of it’, to be a less favourable market environment, bonds continued to deliver diversification benefits to equities. But how? One potential driver may be the actions of central banks. During periods of financial deleveraging, by dramatically reducing cash rates, central banks have aimed to encourage investors to continue holding riskier assets. By doing so, the central banks sought to provide a stimulatory tailwind to assist the recovery in the economy and financial systems. The ongoing success of such a strategy however risks being undermined by bouts of heighted market risk. Accordingly, central banks in the last decade have increasingly used interest rates as a tool to specifically offset episodes of heightened market risk. In such an environment, bonds may have maintained the potential to act as effective diversifiers, and indeed may have become more effective diversifiers, when most needed. With central banks continuing to adopt a cautious approach to the normalisation of interest rates, as they seek to sustain the global growth cycle, the diversifying benefits of bonds are likely to be maintained going forward.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

1 topic

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment