TOL - 15th Jan, 2021

Here. We. Go

A healthy process to undertake as you get back to the market from holiday (if you managed one) is to do some attribution on what you’ve missed and what you hold. Half of investing is not the heroic decisions, it's not making mistakes and today we look at some of the mistakes we made (cashing up a bit in December, selling half our energy bet, holding almost any tech stocks other than APT, not holding a lot of banks) and what we got right (selling travel temporarily).

Fund managers do constant (daily) attribution on their performance. Without it, funds management is a random walk with no lessons, learning or development. Here is the attribution on the market in the last two weeks.

What you missed

Here is a look at what themes have been running in the last month which might help you explain your performance and identify the themes running at the moment.

- The market going up – The ASX 200 is up 10% in a month and 14% in three months. Our cash levels, which we raised from almost zero to 24.6% in mid-December were too high for a market going up. We don’t mind that too much, more cash means less risk so in a rising market that comes at a cost (some underperformance). As we found out last year, 90% of the time you should be fully invested and only occasionally, at precipitous moments, cash up. We should have stayed fully invested in hindsight but with the issues of vaccine delays, virus mutations, hot-spotting in Australia, global case numbers (in the UK in particular) out of control, a very strong A$ hurting international stocks, and an over-valuation debate in overseas markets, we're comfortable. We don't see impeachment as a market issue and can see the positives of a new stimulus bill, political stability in the US and the recovery potential in some Australian sectors. We seem to be in a new sideways pattern after the early January jump.

- Recovery stocks have topped out in places, particularly Travel and Tourism as hotspots popped up and border closures killed forward bookings for airlines and accommodation. We timed our sale of travel stocks rather well in December but will look to get back involved should a vaccine get traction.

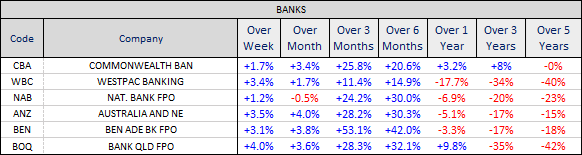

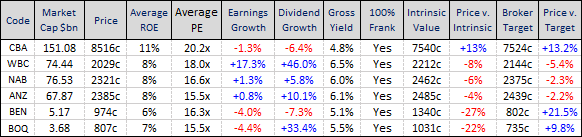

- Banks going up and paying dividends - Bank dividends were paid in December and those dividends were compounded into the Accumulation benchmarks that a lot of fund managers use. It is very hard to perfectly compound dividends the way the index does, which it does at no cost. ANZ paid its dividend on December 16, WBC paid on December 18, NAB paid on December 10. That compounding into the benchmark index creates underperformance for anyone that doesn’t match that process, although they were much-reduced dividends from previous years. We have solid weightings in banks in our income portfolio but not growth. This year should see some dividend normalisation with higher yields – the CBA results on Feb 10 will give us the heads up on the likely timing of dividend normalisation. The problem with the banks is that they are now not cheap, with PE multiples (on reduced earnings numbers) at the top of their historic PE range. They need to see a significant earnings improvement next year to justify current prices but, having over-provided for bad debts last year, they have plenty of firepower (to add back provisions) to improve earnings this year. Happy to hold in the income portfolio but not for growth. The sector is also benefited from rising bond yields recently which allows them to expand margins and creates earnings upgrades. Most brokers see them as fairly valued to overvalued at the moment.

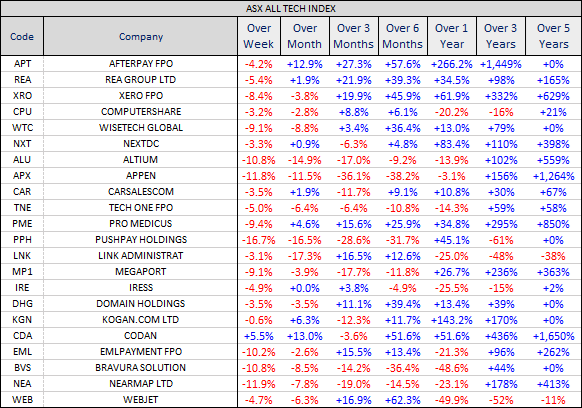

- Tech stocks fell - The most vulnerable sector to the over-valuation concerns. We hold some of them including ALU, SSM, and XRO which has fallen sharply of late. We also hold TNE and NXT which have held up relatively well. Afterpay has also held up. You can see in the performance table below how the tech sector has topped out in the last couple of weeks. With the momentum versus value discussion now well established, success in technology stocks will increasingly come down to stock picking rather than blind FOMO this year. You have to be in the right stocks, not all stocks.

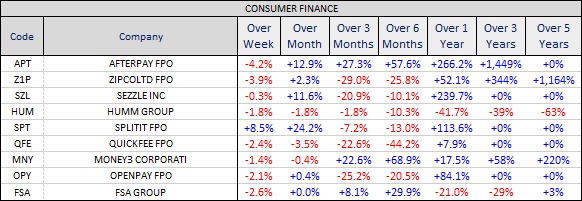

- BNPL – It's all about APT. The rest peaked six months ago. Another sector with over-valuation concerns.

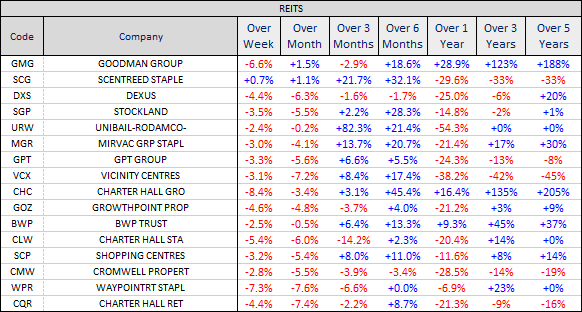

- REITS topping out - Seen as a recovery sector, rolling hotspots and the long-term implications of working at home and shopping online has dented recovery momentum in a number of sectors including commercial/office and retail REITs.

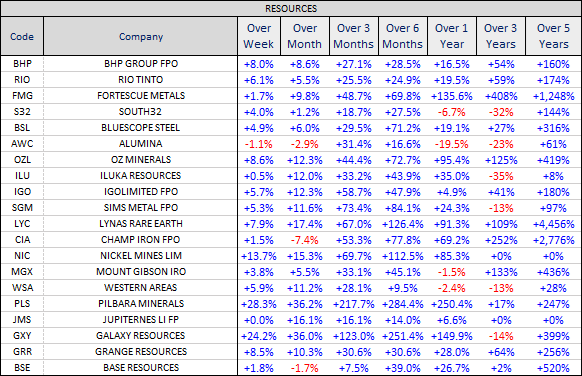

- Resources flying - You had to hold BHP and RIO and other resources over the last month. Sector momentum is strong (too strong?). The iron ore price popped over $170 a tonne as the Chinese closed major road and travel routes to contain another virus outbreak. BHP and RIO up over 25% in the last three months. We hold significant holdings in all portfolios but this is a trading sector and having “faith” in the sector’s performance needs constant reassessment. We will be constantly looking for the top this year. This is a weekly chart:

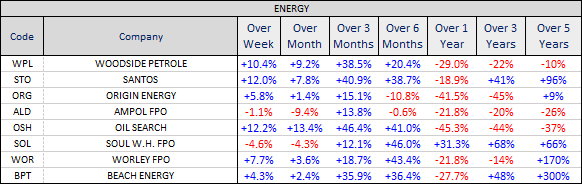

- The energy sector continued to rally over the break – We foolishly halved our big energy bet in late December. Should have left it alone. A unilateral Saudi production cut has kept the oil price and energy sector momentum going. It remains a sector that is well off its highs and still has recovery potential should the vaccine arrive and the pandemic is forgotten. The market seems to be doubting that at the moment. We will look to top up again at the right moment.

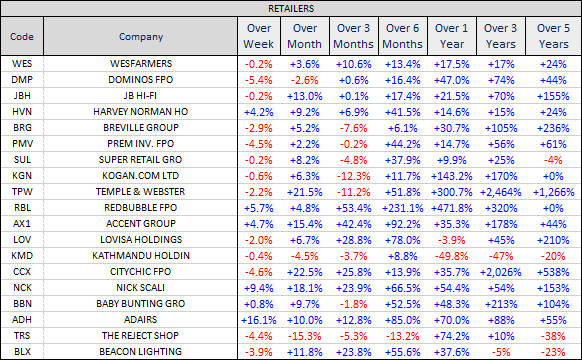

- Retailers holding up – Pandemic or not, they seem to be thriving on stimulus, the move to online, and the spending power directed from travel and holiday spending to retail therapy. They have also had a good month as the hotspots have taken people off the beach and put them back in front of their computers.

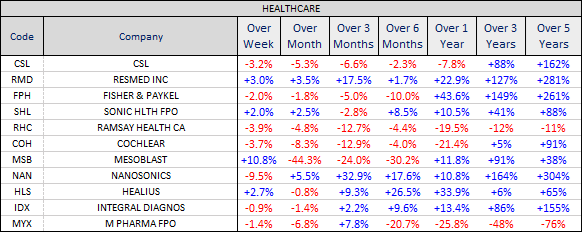

- Healthcare underperforming – CSL down 5.3% in a month and COH down 8.3%. Long-term, quality stocks that have been hurt by the strength in the A$ as a commodity currency in an economic revival.

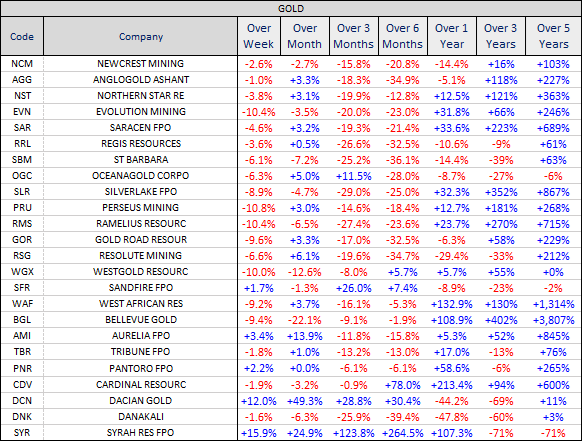

- Gold lost its shine as the vaccine and recovery rally gathered pace. If the market goes to hell it is the obvious sector to buy. There are buy signals around in the short term.

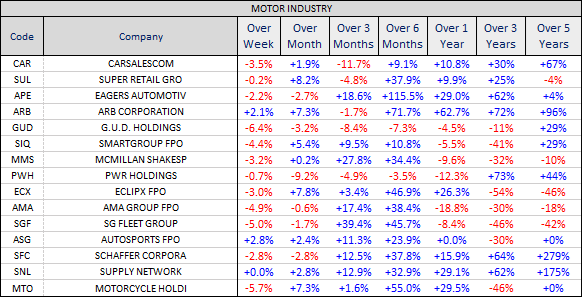

- Car industry stocks lost momentum in the last week but have held up pretty well as pandemic beneficiaries. They too have benefited from a redirection of discretionary travel spending into domestic holidays, driving holidays, idle retail spending of stimulus money, and the expectation that the post-pandemic use of public transport will diminish. Some of those themes should be secular (permanent behaviour change) not cyclical.

Other mild sector themes include:

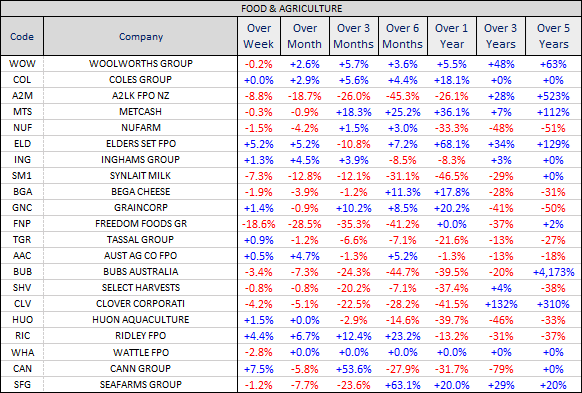

- Food & Agriculture still bent over by the Chinese:

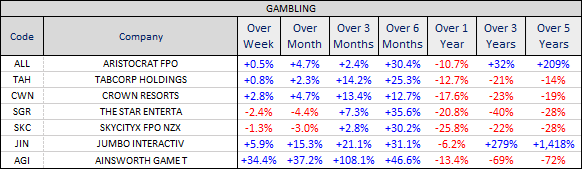

- Gambling stocks on the road to recovery:

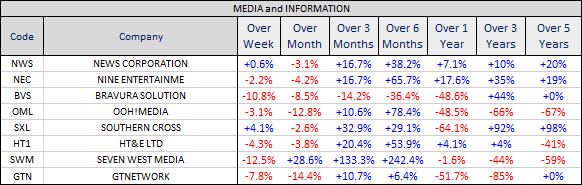

- Media recovery paused:

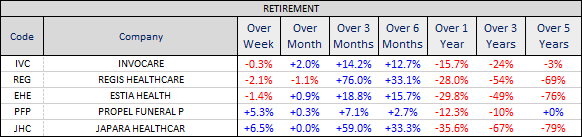

- A recovery in Aged Care/Retirement homes stocks continue:

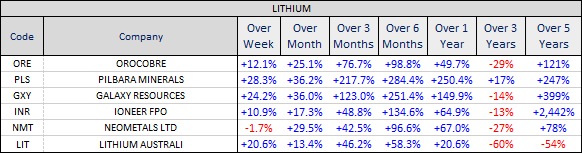

- Lithium storming along:

Themes for 2021

What are the predictions for the New Year?

The highest probability prediction is that the themes that are trending at the moment will continue to trend. There is no point us heading off down some lonely contrarian road just because it's 2021. Believe what is happening now, invest in that and the odds are that you will be more right than wrong. So here are the current themes that are likely to persist and deserve more faith than some wild clickbait fantasy:

- Expect the bull market to continue until it doesn’t. Don’t constantly worry about a market collapse. Just be alert to it. React don’t predict. We intend to remain fairly fully invested until we wake up and decide not to be.

- Look for the recovery sectors to recover again assuming the vaccine roll-out gains momentum. The recent Australian hot-spotting has dented REITs, travel and tourism and energy remains well off its highs – an opportunity.

- Stock pick technology stocks. Many are still in La-La land when it comes to valuation. The days of surviving on popularity, momentum and FOMO are limited – be prepared to trade them not invest in them.

- The Resources sector trend depends on unreliable commodity prices. OK for now but don’t take them for granted.

- The Energy sector is still well below its long-term highs – it remains a recovery sector. Stick with it unless there is a vaccine hiccup or an oil price top.

- Banks are for income, not growth but the odds for the year ahead include a few positives – dividend normalisation, earnings improvement (as they add back over-provisioning), less regulatory interference, higher interest rates (wider margins) and earnings upgrades.

- Aussie dollar strength – The A$ has rallied hard as economic recovery hopes pump commodity prices and commodity currencies. The odds are on it continuing which will limit the performance of the big international stocks...healthcare mostly.

The biggest risks

The market “Climbs the wall of worry”. There is always something to worry about but we really don’t need to worry about things that could happen until they happen.

But what could put a spanner in the works? Your guess is as good as mine but the most obvious market killer is a virus mutation that renders existing vaccines ineffective and puts us back to square one on a medical solution. Pandemic beneficiaries would soar, recovery sectors dump, gold will fly, and the market will briefly collapse. Mild forms of that will come with anything that dents the market’s global economic assumption or delays it.

Another obvious development would be the appearance of inflation and a change in central bank rhetoric from maximum stimulus to hawkish policy tapering. The central banks are unlikely to allow a repeat of the “taper tantrum” that caused the market to fall over in October 2018, so we can probably relax for this year at least.

Access to our exclusive newsletters

We write daily for Marcus Today members, keeping them up to date on our current strategy and stock ideas. To get our next update, sign up for a 14-day free trial to Marcus Today – CLICK HERE to get started.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and informing private investors with insightful, honest, straight-up independent stock market research and ideas. Marcus likes to call it as it is without agenda, puts subscribers first, and this has paid off for real people with real money.

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Comments

Comments

Sign In or Join Free to comment