High Yield Bonds - Flashing Amber

Chris Manuell, CMT

Jamieson Coote Bonds

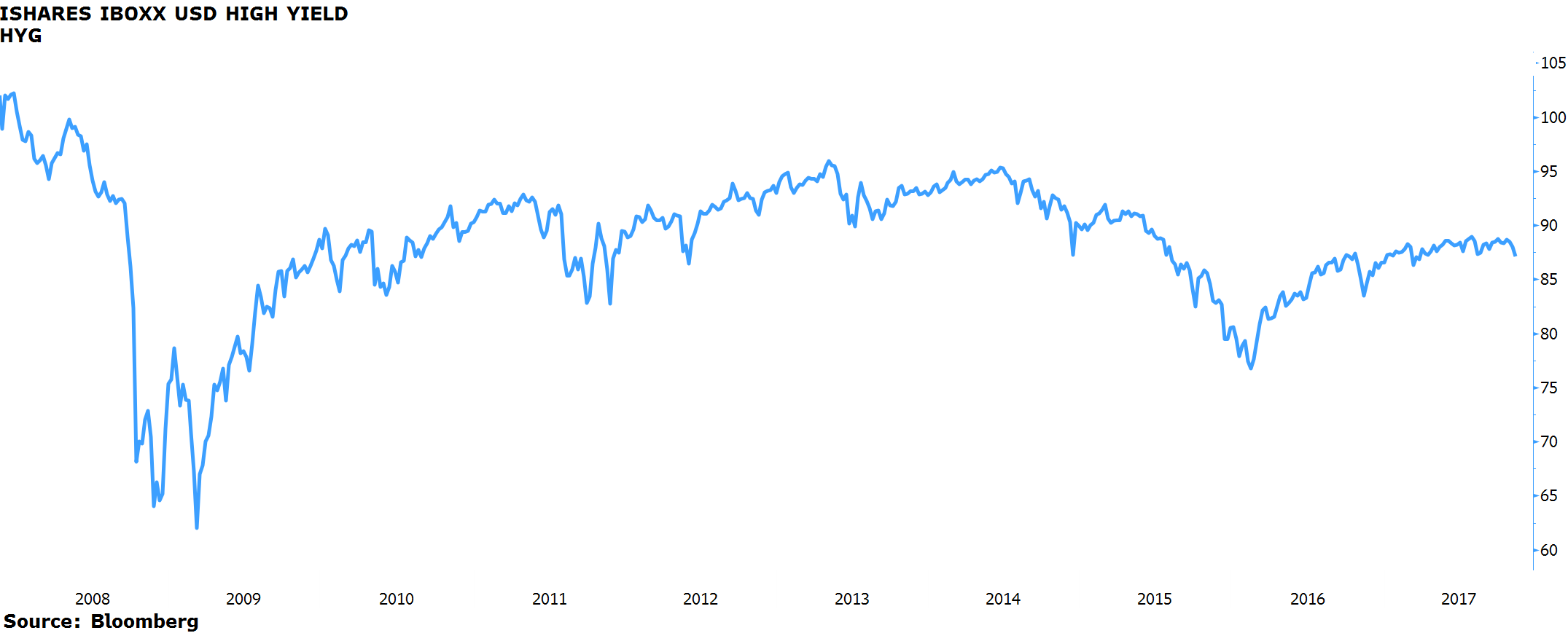

Global financial markets have remained devoid of any meaningful volatility this year which partly explains the excitement last week following the sharp retracement in high yield bonds. Credit is historically the canary in the coal mine for impending weakness in other asset classes which is why it tends to attract so much attention when it starts to wobble. Market participants are particularly sensitive at the moment given that we are late in the innings for this business cycle. Looking through the hourglass of the global economic cycle clock, Jamieson Coote Bonds (JCB) feels it’s not quite time to ring the bell on credit, although the window is narrowing.

The US equity market is in the midst of its second-longest bull run in history, alongside its economy which is enjoying its third longest period of growth since the 19th century. Global high yield spreads are not immune to the “everything bubble” although unlike bitcoin or Paul Newman’s Rolex Daytona their importance to the global economic machine cannot be dismissed. Deducing when the business cycle is going terminate is crucial for investors, bearing in mind the simplistic notion that in the final stages of an expansion, corporate profits will diminish as wages climb whilst rising interest costs hinder returns on capital.

JCB monitors credit and the business cycle ardently given its importance in our investment process and portfolio management. We don’t feel this turmoil in junk bonds will persist in the near term and morph into other asset classes this year and as a result we envisage a mean reversion of the recent retracement. Although last week saw the biggest outflow in eight weeks for high yield bonds according to EPFR Global data, we feel this is just the warm up for the greater move in 2018 when credit will start to feel the impact of the Fed tightening bias, the inevitable rise in asset market volatility and the increasing pressure on the balance sheets.

This recent weakness or noise can be attributed to few specific factors

- 3 of the largest Wall Street investment banks as well as the highly feted US bond manager Jeffrey Gundlach recommending to reduce high-yield corporate debt exposure, which in itself is a contrarian “buy the dip” signal for the cynical investor

- Telecommunications account for 20% of dollar junk bonds as such are the biggest sector in the index and they just reported some disappointing 3Q results

- Deluge of supply and issuance weighed down the market, particularly in the Telco sector, as it was the third highest weekly investment grade credit total this year as issuers storm the market before Thanksgiving and the impending December US Fed rate hike

- Seasonally November is a poor month for high yield as the market enters year end with 8 of the last 10 Novembers closing in the red

JCB remains concerned with the bigger picture of the credit markets and the business cycle given the impending US Fed rate hikes, the record low volatility across asset classes and the weaker credit standards as demonstrated in the erosion of covenants for bond-holders. However as monetary policies still remain accommodative around the globe with the European Central Bank and Bank of Japan as the anchors it will be hard to prevent the stretch for yield in the near term. Heading into 2018 the ECB and BoJ will still be targeting more than $90 billion of asset purchases every month as the liquidity fountain remains open. High yield bonds should also benefit from the energy complex which is rounding out the year in positive fashion and is viewed constructively by JCB .Given its heavy weighting in the high yield index, this will somewhat negate the recent Telecommunications lead weakness.

Investors are wise to be concerned with the tightness of the high yield credit spreads given that excess returns are historically negative in the three to five years after spreads approach or fall below 300 bp. Credit has also presaged the last two spectacular asset class meltdowns in 2000 and 2007 which is why JCB will be following it closely in 2018 as we anticipate the countdown of the global economic cycle.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris oversees a range of investment strategies for institutional and retail clients. He is a bond investment specialist with over 20 years of experience gained at Merrill Lynch, Société Générale and The Royal Bank of Canada, here and abroad.

Chris Manuell, CMT

Senior Portfolio Manager

Jamieson Coote Bonds

Chris oversees a range of investment strategies for institutional and retail clients. He is a bond investment specialist with over 20 years of experience gained at Merrill Lynch, Société Générale and The Royal Bank of Canada, here and abroad.

Expertise

Chris Manuell, CMT

Senior Portfolio Manager

Jamieson Coote Bonds

Chris oversees a range of investment strategies for institutional and retail clients. He is a bond investment specialist with over 20 years of experience gained at Merrill Lynch, Société Générale and The Royal Bank of Canada, here and abroad.

Expertise

Comments

Comments

Sign In or Join Free to comment