How much money should I lose?

Cash is the only asset that rises in value smoothly. Everything else has bumps along the way. Random price moves make it hard to distinguish between signal and noise, especially when markets are volatile. For example, we expect stocks to rise over the long run but with unpredictable losses over shorter horizons. But these swings can also provide buying opportunities when prices change rapidly, while underlying fundamentals do not. All else equal, a lower purchase price corresponds to higher future expected returns and vice versa.

The simplest way to estimate intermediate losses is by looking at past returns. However, the history that occurred is just one outcome. The implicit assumption is that future returns will look like the past. We can also generate and analyse a large number of simulated outcomes using the properties of the asset. The implicit assumption is the asset characteristics are stable and can be modelled accurately.

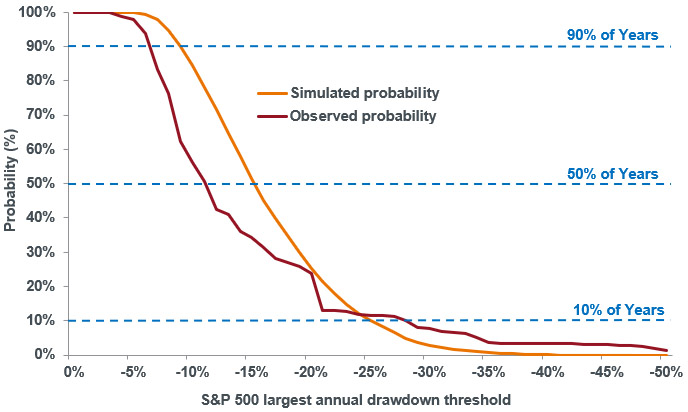

Both these assumptions are wrong – finance is not physics. But they provide a rough approximation of what an investor can reasonably expect. Exhibit 1 shows observed and simulated probabilities of various-sized S&P 500® Index drawdowns (greatest high to low percentage loss) over rolling one-year periods.

The observed and simulated curves are broadly similar. Comparing observed drawdowns to simulated ones, small S&P 500 drawdowns have occurred less frequently, but large S&P 500 drawdowns have occurred more frequently.

In most (90%) of years, we should expect the S&P 500 to have at least one drawdown of 7–10% or more. In 50% of years, the S&P 500 is likely to have a drawdown of 11–15% or more. And in about 10% of years, the S&P 500 is anticipated to lose more than 25%.

Source: Bloomberg, Janus Henderson, Observed from January 1998-January 2020, Simulation uses Monte-Carlo analysis. S&P 500 data excludes transaction costs. Past performance is not a guide to future performance.

We can generalize this result. For an asset with volatility (σ) and log-normally distributed returns, we would expect a drawdown of magnitude (σ/2) to occur about once a year and a drawdown of magnitude (σ) to occur about once every two years. To be clear, there is no assurance that the actual price path of the asset will follow this expectation. But this model fits reasonably well with observed moves.

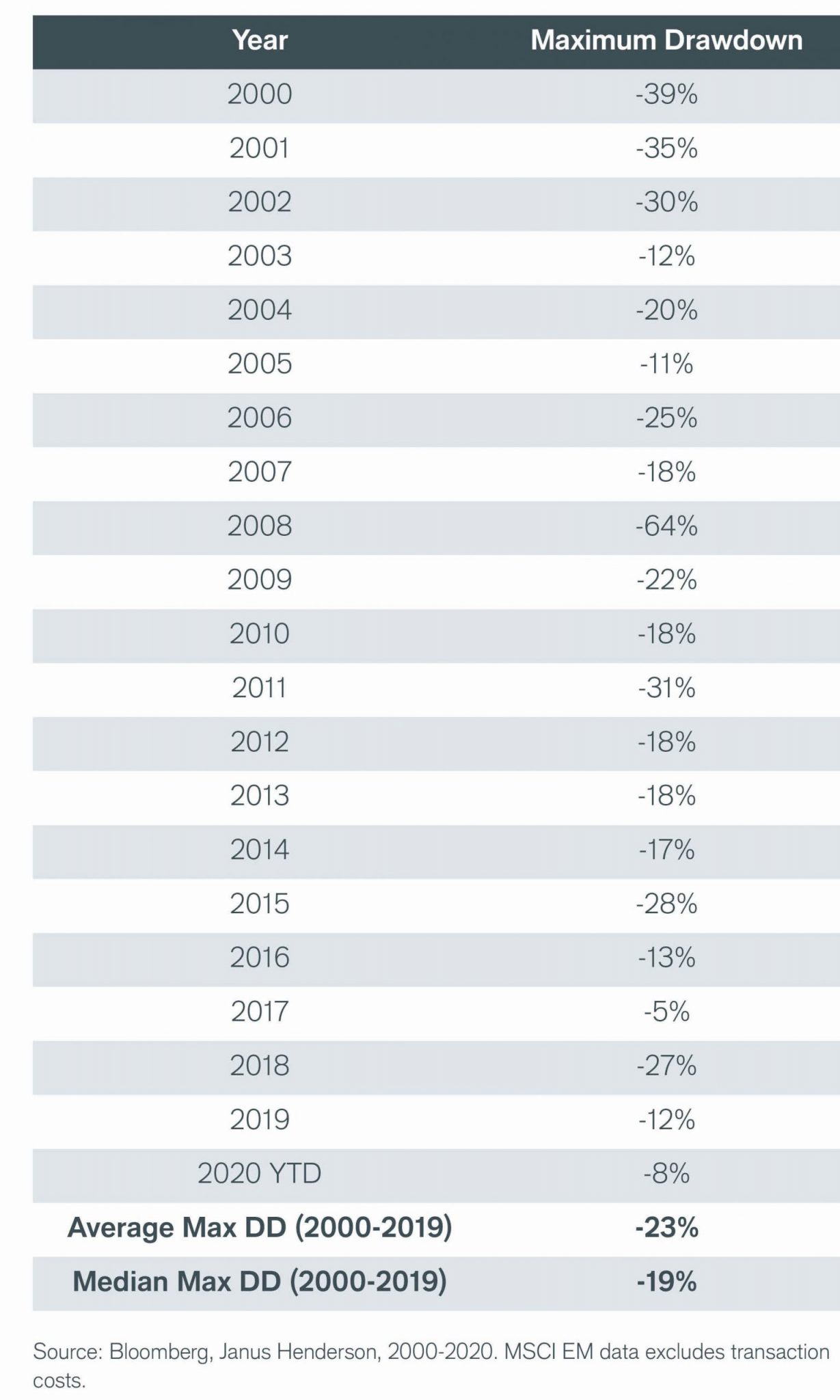

For example, the MSCI Emerging Market (EM) Index has had an average annualized volatility of about 20%. Since 2000, the index has had a 10% (σ/2) or greater drawdown in 19 out of 20 years. A 20% (σ) or greater drawdown has occurred in about 50% of years. Exhibit 2 shows the maximum drawdowns by year for the MSCI EM Index.

Past performance is not a guide to future performance.

Already in 2020, the MSCI EM Index has dropped 8% following the COVID-19 outbreak. Although the cause of the recent fall was unforecastable, the size of the drawdown is in line with expected EM drops that occur periodically. If you are positively biased towards owning more EM equities, buying a ~10% decline captures a reasonably sized dip that has happened in most years.

However, if you are instead waiting for EM stocks to fall 30% before investing, that can and has happened, but is probabilistically unlikely. A drop that large (-30% or more) has only occurred in about 25% of years. To wait for that before buying, you need to have very strong conviction that the current year will be remarkably bad for EM equities.

We don’t know how asset prices will move. But we can ballpark using historical and simulated data about what swings to expect due to “randomness”. More volatile assets have larger moves. For example, Amazon.com has had a greater than 50% drawdown on four different occasions in its history, yet its share price is near all-time highs. Conversely, if a corporate bond drops 50%, it is highly likely to default. Looking at drawdown probabilities provides a simple way to calibrate our expectations based on the type of asset.

The information in this article is not an investment recommendation. References to stocks, indices or asset classes do not constitute or form part of any offer or solicitation to buy or sell. These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

David Elms is Head of Diversified Alternatives for Janus Henderson Investors responsible for enhanced index, risk premia, and hedge fund portfolios. Prior to joining Henderson in 2002, he spent eight years as a founding partner at Portfolio Partners. He was initially based in Melbourne, where he managed derivatives and enhanced index portfolios, and was later seconded to Aviva in London in a corporate strategy role following Aviva’s acquisition of Portfolio Partners.

David received a BCom degree (Hons) from the University of Melbourne and has 28 years of financial industry experience

David Elms is Head of Diversified Alternatives for Janus Henderson Investors responsible for enhanced index, risk premia, and hedge fund portfolios. Prior to joining Henderson in 2002, he spent eight years as a founding partner at Portfolio...

David Elms is Head of Diversified Alternatives for Janus Henderson Investors responsible for enhanced index, risk premia, and hedge fund portfolios. Prior to joining Henderson in 2002, he spent eight years as a founding partner at Portfolio...

Comments

Comments

Sign In or Join Free to comment

most popular

Education

How Warren Buffett has trounced “the world’s greatest hedge fund manager”

Leithner & Company Ltd